If you’re part of a religious organization in Canada or simply interested in how these organizations operate, you might wonder: how does the Canada Revenue Agency (CRA) decide if a religious group can be considered a charity? This question touches on important aspects of common law and the specific requirements of the Income Tax Act. Let’s break down the key points to understand this process better.

The Role of Common Law and the CRA In Canada, common law plays a significant role in determining what counts as a charitable purpose. One of these purposes is advancing religion. However, it’s important to know that the CRA doesn’t judge the value or worth of different belief systems. Instead, it assesses if an organization meets the legal requirements to be registered as a charity.

Historical Context and Diversity Most of the common law concerning religion was developed in predominantly Christian countries. As a result, the language used in these legal decisions might not fully reflect Canada’s diverse religious landscape today. Despite this, the principles from these cases apply to all religious organizations aiming to achieve charitable status.

Defining Religion According to Charity Law For an organization to be eligible for charitable status on the basis of advancing religion, it must prove that its belief system qualifies as a religion under charity law. Here are the three essential elements required:

Belief in a Supreme Being: The organization must have a doctrine that includes belief in a God or Supreme Being.

Worship or Reverence: There must be a doctrine that requires adherents to worship or revere this Supreme Being.

Comprehensive System of Faith and Worship: The belief system must include a detailed and comprehensive set of faith practices and worship methods.

Advancing Religion: What Does It Mean? Once a belief system is established as a religion, the CRA evaluates whether the organization is advancing this religion according to charity law. To advance religion means to manifest, promote, sustain, or increase belief in the religion. This is assessed by looking at the organization’s purposes and activities.

Purposes That Advance Religion A purpose that advances religion must clearly state:

a. The specific religion being promoted.

b. The methods used to advance the religion.

c. Who will benefit from these religious activities.

For detailed guidance on how to draft these purposes, the CRA provides a document called Guidance CG-019.

Activities That Advance Religion Not every activity done in the name of religion qualifies as advancing religion in a charitable sense. Activities that do meet this requirement must:

1. Be clearly and materially connected to the religion’s teachings, doctrines, or observances.

2. Aim to manifest, promote, sustain, or increase belief in the religion among adherents or the general public.

Activities That Serve Multiple Charitable Purposes Sometimes, religious activities can also further other charitable purposes like relieving poverty, advancing education, or benefiting the community. For these activities to count as advancing religion, they must:

Directly Further Another Charitable Purpose: The activity should meet all criteria for directly furthering a different type of charitable purpose.

Connect to Religious Teachings: There must be a clear and material link to the religion’s teachings, doctrine, or observances.

Public Perception: The public should be able to recognize the activity as linked to the religion being advanced.

Understanding how the CRA evaluates religious organizations for charitable status involves knowing the intersection of common law and the Income Tax Act. By ensuring that an organization’s belief system, purposes, and activities meet specific legal criteria, religious groups can achieve recognition as charities. This process ensures that charitable status is granted fairly and reflects the diversity of religious practices in Canada. Whether you’re part of a religious organization or simply curious about the law, these guidelines provide a clear framework for understanding what it means to advance religion in a charitable context.

At Northfield & Associates our expert teams guidance on compliance requirements. Our team understands Canadian charity law and can help ensure your organisation follows proper procedures.

In this evolving economic landscape, collaboration with our firm offers clients a strategic advantage. With Cambodia’s reform-driven investment environment and Canada’s expanding footprint in Southeast Asia, our team of experienced consultants and legal advisors provides tailored guidance to help businesses navigate cross-border opportunities. We focus in developing comprehensive legal strategies, structuring international partnerships, and ensuring compliance in emerging markets.

By leveraging our regional insight and international expertise, you benefit from a trusted partner dedicated to helping you capitalize on growth potential in Cambodia and beyond.

Book a Consultation with Northfield & Associates

Your Trusted Partner in International Bilateral Relations

At Northfield & Associates are focus in Foreign Direct Investment (FDI), international trade missions, and cross-border legal strategy. Our team of experienced consultants and legal advisors offers tailored guidance and strategic insight to help you navigate the complexities of international partnerships and development opportunities.

Whether you choose to meet in person at one of our offices or connect virtually, we provide flexible and accessible consultation options. During your session, we’ll assess your goals, review key documentation, and guide you through every stage of your FDI or trade mission engagement.

Let us help you take the next step with confidence supported by trusted legal and strategic counsel every step of the way.

Take the First Step Today

If you believe you may be eligible for legal relief or simply need sound legal advice, we’re here to help. Contact us today to book your consultation. Let us provide the clarity, strategy, and peace of mind you need to move forward.

We serve our clients in English, Cambodian, Vietnamese, Mandarin and Cantonese, especially in Asian clients.

If you or anybody that you know, think that you meet the requirements and wish to receive further information.

We can help you start the application process and confirm eligibility requirements to participate.

We Offer Consultations & Meetings by Phone & Virtually. Affordable Fees.

Disclaimer:

The information contained in this article is provided for general information purposes only and does not constitute legal or other professional advice. Readers should seek tailored legal advice in relation to their personal circumstances.

Northfield & Associates International Corporation is a global consulting firm serving private enterprises, public institutions, not-for-profit organizations, and institutional capital providers. Operating across Cambodia, Canada, and global markets, the firm supports capital deployment, regulatory navigation, and enterprise decision-making in complex economic and geopolitical environments. Northfield & Associates delivers customized, execution-focused advisory solutions that drive measurable transformation, strengthen competitiveness, and enhance long-term highest value opportunities. The firm incorporates consulting, legal, regulatory, financial, and risk expertise to enable disciplined capital allocation, strong governance, and operational resilience. Northfield & Associates upholds a culture of applied insight and innovation, supporting clients across digital transformation, growth strategy, and organizational capability building. The firm advises individual, leading global corporations, midsize enterprises, government agencies, and mission-driven organizations through long-term partnerships. Enterprise-wide risk management, professional ethics, and fiduciary standards are embedded across all operations. Northfield & Associates’ diverse, globally unified teams are committed to execution certainty and sustainable, risk-adjusted returns aligned with ESG and stakeholder objectives.

Forward-Looking Information

This news release contains forward-looking information. All statements, other than statements of historic fact, that address activities, events or developments that the Company believes, expects or anticipates will or may occur in the future constitute forward-looking information.

This forward-looking information reflects the current expectations or beliefs of the Company based on information currently available to the Company.

Forward-looking information is subject to a number of risks and uncertainties that may cause the actual results of the Company to differ materially from those discussed in the forward-looking information, and even if such actual results are realized or substantially realized, there can be no assurance that they will have the expected consequences to, or effects on the Company. Factors that could cause actual results or events to differ materially from current expectations include, among other things: the failure to finalize negotiations concerning the increase of the Loan or to close such transaction and the failure of the Company to complete the acquisition of the Company Facility; operating performance of facilities; environmental and safety risks; delays in obtaining or failure to obtain necessary permits and approvals from government authorities; unavailability of plant, equipment or labour; inability to retain key management and personnel; changes to regulations or policies affecting the Company’s activities; and the other risks disclosed under the heading “Risk Factors” and elsewhere in the Company’s amended annual information.

Forward-looking information speaks only as of the date on which it is made and, except as may be required by applicable securities laws, the Company disclaims any intent or obligation to update any forward-looking information, whether as a result of new information, future events or results or otherwise. Although the Company believes that the assumptions inherent in the forward-looking information are reasonable, forward-looking information is not a guarantee of future performance and accordingly undue reliance should not be put on such information due to the inherent uncertainty therein.

Questions?

info@northfied.biz

Within Corporate Newsroom

Media Contact:

media@northfied.biz

Press contact

PR consultants press@northfied.biz

NOT LEGAL ADVICE. Information made available on this website in any form is for information purposes only. It is not, and should not be taken as, legal advice. You should not rely on, or take or fail to take any action based upon this information. Never disregard professional legal advice or delay in seeking legal advice because of something you have read on this website. Northfield & Associates professionals will be pleased to discuss resolutions to specific legal concerns you may have.

CRA’s Guidance on Grants to Non-Qualified Donees Explained

In a significant move impacting the Canadian charitable sector, amendments to the Income Tax Act (ITA) in June 2022 introduced alternative options for registered charities to engage with non-qualified charities and organizations abroad. The new “qualifying disbursement” rules allow charities to make certain disbursements to non-qualified donees, and the Income Tax Regulations now mandate additional reporting obligations for disbursements exceeding CA$5,000 in a taxation year.

One of the key developments following these amendments is the release of the Canada Revenue Agency’s (CRA) Draft Guidance on registered charities making grants to non-qualified donees (Guidance CG-032) on November 30, 2022. While the Draft Guidance is still in its draft form, several key takeaways and insights can be drawn.

Key Takeaways:

Opportunity Amidst Caution: Despite the Draft Guidance being in a draft form, charities can now make qualifying disbursements. However, caution is advised until the finalized guidance is released, expected in late summer or early fall 2023 at the earliest.

Reporting Updates: The T3010 and T4033 are undergoing updates and are expected to be available shortly.

Understanding the Landscape: The Old Regime vs. The New Regime

The Old Regime: Before the amendments, charities had limited options, primarily focusing on their own activities or making gifts to qualified donees. Providing resources to non-qualified donees required strict adherence to CRA’s “direction and control” requirements.

The New Regime: The amendments introduced two routes for registered Canadian charities: continuing “own activities” or making a qualified disbursement. The latter allows disbursements to both qualified donees and grantee organizations (non-qualified donees) under specific conditions.

Draft CRA Guidance: Accountability and Risk Assessment

The Draft Guidance delineates accountability standards for eligible disbursements, underscoring the significance of showcasing that the recipient organization allocates the disbursement solely to charitable activities aligned with the charity’s declared mission.

Risk assessment is a crucial aspect, and charities are advised to evaluate the level of risk associated with each grant, with the guidance providing tools for accountability and risk mitigation.

Schedule for Publication of Conclusive CRA Guidance

The Draft Guidance underwent a public comment period until January 31, 2023, with the anticipated release of the finalized version later this year. The entire projected timeframe for the CRA to formulate guidance spans from 10 to 20 months since the enactment of the new legislation.

Moving Forward: Recommended Next Steps

While the Draft Guidance signals positive steps toward flexibility for registered charities, it’s crucial to remember that it is still in draft form. Charities interested in leveraging the new rules should proceed with caution until the CRA addresses public comments and provides further clarity on compliant granting to non-qualified donees.

At Northfield & Associates our expert teams guidance on compliance requirements. Our team understands Canadian charity law and can help ensure your organisation follows proper procedures.

In this evolving economic landscape, collaboration with our firm offers clients a strategic advantage. With Cambodia’s reform-driven investment environment and Canada’s expanding footprint in Southeast Asia, our team of experienced consultants and legal advisors provides tailored guidance to help businesses navigate cross-border opportunities. We focus in developing comprehensive legal strategies, structuring international partnerships, and ensuring compliance in emerging markets.

By leveraging our regional insight and international expertise, you benefit from a trusted partner dedicated to helping you capitalize on growth potential in Cambodia and beyond.

Book a Consultation with Northfield & Associates

Your Trusted Partner in International Bilateral Relations

At Northfield & Associates are focus in Foreign Direct Investment (FDI), international trade missions, and cross-border legal strategy. Our team of experienced consultants and legal advisors offers tailored guidance and strategic insight to help you navigate the complexities of international partnerships and development opportunities.

Whether you choose to meet in person at one of our offices or connect virtually, we provide flexible and accessible consultation options. During your session, we’ll assess your goals, review key documentation, and guide you through every stage of your FDI or trade mission engagement.

Let us help you take the next step with confidence supported by trusted legal and strategic counsel every step of the way.

Take the First Step Today

If you believe you may be eligible for legal relief or simply need sound legal advice, we’re here to help. Contact us today to book your consultation. Let us provide the clarity, strategy, and peace of mind you need to move forward.

We serve our clients in English, Cambodian, Vietnamese, Mandarin and Cantonese, especially in Asian clients.

If you or anybody that you know, think that you meet the requirements and wish to receive further information.

We can help you start the application process and confirm eligibility requirements to participate.

We Offer Consultations & Meetings by Phone & Virtually. Affordable Fees.

Disclaimer:

The information contained in this article is provided for general information purposes only and does not constitute legal or other professional advice. Readers should seek tailored legal advice in relation to their personal circumstances.

Northfield & Associates International Corporation is a global consulting firm serving private enterprises, public institutions, not-for-profit organizations, and institutional capital providers. Operating across Cambodia, Canada, and global markets, the firm supports capital deployment, regulatory navigation, and enterprise decision-making in complex economic and geopolitical environments. Northfield & Associates delivers customized, execution-focused advisory solutions that drive measurable transformation, strengthen competitiveness, and enhance long-term highest value opportunities. The firm incorporates consulting, legal, regulatory, financial, and risk expertise to enable disciplined capital allocation, strong governance, and operational resilience. Northfield & Associates upholds a culture of applied insight and innovation, supporting clients across digital transformation, growth strategy, and organizational capability building. The firm advises individual, leading global corporations, midsize enterprises, government agencies, and mission-driven organizations through long-term partnerships. Enterprise-wide risk management, professional ethics, and fiduciary standards are embedded across all operations. Northfield & Associates’ diverse, globally unified teams are committed to execution certainty and sustainable, risk-adjusted returns aligned with ESG and stakeholder objectives.

Forward-Looking Information

This news release contains forward-looking information. All statements, other than statements of historic fact, that address activities, events or developments that the Company believes, expects or anticipates will or may occur in the future constitute forward-looking information.

This forward-looking information reflects the current expectations or beliefs of the Company based on information currently available to the Company.

Forward-looking information is subject to a number of risks and uncertainties that may cause the actual results of the Company to differ materially from those discussed in the forward-looking information, and even if such actual results are realized or substantially realized, there can be no assurance that they will have the expected consequences to, or effects on the Company. Factors that could cause actual results or events to differ materially from current expectations include, among other things: the failure to finalize negotiations concerning the increase of the Loan or to close such transaction and the failure of the Company to complete the acquisition of the Company Facility; operating performance of facilities; environmental and safety risks; delays in obtaining or failure to obtain necessary permits and approvals from government authorities; unavailability of plant, equipment or labour; inability to retain key management and personnel; changes to regulations or policies affecting the Company’s activities; and the other risks disclosed under the heading “Risk Factors” and elsewhere in the Company’s amended annual information.

Forward-looking information speaks only as of the date on which it is made and, except as may be required by applicable securities laws, the Company disclaims any intent or obligation to update any forward-looking information, whether as a result of new information, future events or results or otherwise. Although the Company believes that the assumptions inherent in the forward-looking information are reasonable, forward-looking information is not a guarantee of future performance and accordingly undue reliance should not be put on such information due to the inherent uncertainty therein.

Questions?

info@northfied.biz

Within Corporate Newsroom

Media Contact:

media@northfied.biz

Press contact

PR consultants press@northfied.biz

NOT LEGAL ADVICE. Information made available on this website in any form is for information purposes only. It is not, and should not be taken as, legal advice. You should not rely on, or take or fail to take any action based upon this information. Never disregard professional legal advice or delay in seeking legal advice because of something you have read on this website. Northfield & Associates professionals will be pleased to discuss resolutions to specific legal concerns you may have.

Charity Registration Timeline: What to Expect at Each Stage

“How long will it take to get our charity registered?” This is often the first question I hear from clients embarking on the registration process. While I wish I could give a simple answer, the reality is that charity registration in Canada involves multiple stages, each with its own timeline and variables.

Having guided hundreds of organizations through this process, I’ve developed a realistic understanding of how the registration timeline unfolds. In this comprehensive guide, I’ll walk you through each stage of the charity registration process, helping you understand typical timelines, potential delays, and strategies for efficient progress. With proper planning and realistic expectations, you can navigate this journey successfully.

Overview of the Canadian Charity Registration Process

Before breaking down the individual stages, let’s look at the complete process from start to finish.

End-to-end Process Map

The charity registration journey typically follows this path:

Pre-application planning: Research, purpose development, and initial planning

Incorporation: Establishing the legal entity (if not already incorporated)

Application preparation: Completing Form T2050 and assembling supporting documents

CRA submission: Filing the application package with the Charities Directorate

Initial review: CRA’s first assessment of the application

Information exchange: Responding to CRA questions and providing additional materials

Post-approval setup: Implementing systems to operate as a registered charity

This sequential process builds toward successful registration, though some stages may overlap or cycle back if issues arise.

Key Milestones and Decision Points

Critical milestones in the registration journey include:

Incorporation completion: Receiving your certificate of incorporation

Application submission: Filing your completed T2050 package

CRA acknowledgment: Receiving confirmation your application is being processed

Information request: Receiving questions from the CRA examiner

Determination letter: Final decision notification from the CRA

Registration number issuance: Receiving your charitable registration number

First donation receipts: Beginning your charitable receipting program

First T3010 filing: Submitting your first annual information return

Each milestone marks progress toward your goal of operating as a registered charity.

Typical Timeline Ranges

While individual experiences vary, these timeframes are typical:

Total process: 8-18 months from initial planning to registration

Pre-application planning: 1-2 months

Incorporation: 2-4 weeks

Application preparation: 2-4 weeks

CRA initial review: 2-3 months

Information exchange: 1-3 months (if required)

Final determination: 1 month after completing information exchange

Post-approval setup: 1 month

Simple applications with clearly charitable purposes may move faster, while complex applications can take longer, particularly if multiple rounds of questions arise.

Factors Affecting Processing Time

Several factors influence how quickly your application progresses:

Application completeness: Thorough, well-organized applications typically process faster

Purpose clarity: Clear charitable purposes aligned with recognized categories face fewer questions

Activity complexity: Novel or complex activities require more thorough review

International activities: Operations outside Canada typically trigger additional scrutiny

CRA backlog: Processing times fluctuate with the CRA’s current workload

Response times: How quickly you respond to CRA questions affects overall timeline

Professional assistance: Expert guidance often streamlines the process

Previous attempts: Prior unsuccessful applications may receive heightened scrutiny

Understanding these factors helps set realistic expectations and identify areas where you can positively influence the timeline.

Current CRA Processing Standards

The CRA’s current service standards:

Initial acknowledgment: Within 2-4 weeks of receiving application

Simple applications: 3-6 months from submission to decision

Standard applications: 6-12 months from submission to decision

Complex applications: 12-18+ months from submission to decision

Response to inquiries: Generally within 30 days

These standards fluctuate based on the CRA’s workload and resources, but provide a general framework for expectations. For information on CRA oversight, see our article on CRA compliance requirements.

Pre-Application Stage (1-2 Months)

The pre-application stage lays the foundation for successful registration.

Research and Planning

Effective preliminary research includes:

Charity sector analysis: Understanding similar organizations in your field

Legal framework research: Familiarizing yourself with charitable purposes and activities

Governance model exploration: Evaluating different board structures and bylaws

CRA guidance review: Reading relevant CRA policies and guidance

Strategic planning: Aligning charitable goals with recognized charitable purposes

Resource assessment: Evaluating financial and human resources needed

Timeline development: Creating a realistic project plan for registration

This research typically takes 2-4 weeks but pays dividends throughout the process.

Purpose Statement Development

Crafting effective charitable purposes involves:

Category selection: Identifying which recognized charitable categories align with your mission

Precision drafting: Creating clear, specific purpose statements

Legal review: Ensuring purposes meet established legal requirements

Scope definition: Clarifying geographic and beneficiary boundaries

Activity alignment: Ensuring purposes connect clearly to planned activities

Comparison research: Examining purposes of similar registered charities

Iteration: Refining language for clarity and compliance

Allow 1-2 weeks for this critical task, as your purpose statements form the foundation of your application.

Activity Planning

Detailed activity planning includes:

Program development: Outlining specific programs and services

Beneficiary identification: Clearly defining who will benefit from activities

Resource allocation: Determining how time and money will be spent

Implementation timelines: Creating realistic schedules for program launch

Outcome metrics: Defining how success will be measured

Risk assessment: Identifying potential challenges and mitigation strategies

Compliance review: Ensuring activities align with charitable purposes

This planning typically takes 2-3 weeks but creates clarity that speeds the later application process.

Governance Structure Development

Establishing appropriate governance includes:

Board composition planning: Identifying director qualifications and recruitment strategy

Bylaw development: Creating governance rules appropriate for a charity

Cost-benefit analysis: Evaluating when professional help provides best value

Professional consultations throughout the pre-application phase typically total 3-6 hours spread across several weeks.

Incorporation Phase for Canadian Charities (2-4 Weeks)

Establishing the legal entity is a critical step in the registration process.

Federal vs. Provincial Considerations

Incorporation jurisdiction selection involves:

Operational scope assessment: Determining geographical reach of planned activities

Name protection needs: Evaluating importance of nationwide name protection

Governance preference: Comparing governance frameworks across jurisdictions

Cost comparison: Evaluating filing fees and ongoing compliance costs

Timeline needs: Comparing processing times across jurisdictions

Regulatory framework: Considering which legislative framework best fits your organization

Future flexibility: Assessing potential for changing operational scope

This decision typically takes 1-2 weeks of research and consideration. For detailed comparison of incorporation options, see our guide to federal vs. provincial incorporation.

Documentation Preparation

Preparing incorporation documents includes:

Articles of Incorporation/Letters Patent: Primary incorporation document

Bylaws: Internal governance rules

Initial director information: Details of founding board members

Registered office address: Official location for corporate records

Corporate name search: NUANS or provincial name search

Address these requirements promptly to establish good compliance practices from the start. For ongoing compliance guidance, see our CRA compliance FAQ.

Post-Registration Setup (1 Month)

After receiving approval, several systems must be established.

Charitable Receipting Systems

Setting up proper receipting includes:

Receipt template design: Creating compliant official donation receipt format

Donation processing systems: Setting up mechanisms for receiving donations

Credit card processing: Establishing merchant services if needed

Financial control implementation: Creating appropriate separation of duties

Banking arrangements should be updated within 2-3 weeks of registration.

Record-keeping Implementation

Establishing proper records includes:

Document retention policy: Creating guidelines for record preservation

Financial record systems: Implementing appropriate accounting processes

Donation tracking: Systems to document all contributions

Program activity documentation: Processes to record charitable activities

Meeting records: Procedures for maintaining corporate minutes

Digital and physical storage: Appropriate secure storage systems

Accessibility planning: Ensuring records can be retrieved when needed

Backup systems: Creating redundancy for critical records

Basic record-keeping systems should be operational within 2-3 weeks of registration.

Policy Development

Essential policies include:

Financial management policy: Guidelines for financial decisions and controls

Conflict of interest policy: Procedures for managing potential conflicts

Gift acceptance policy: Parameters for what gifts will be accepted

Investment policy: Guidelines for managing charitable assets

Volunteer management policy: Framework for volunteer engagement

Privacy policy: Procedures for handling personal information

Disbursement policy: Guidelines for charitable expenditures

Risk management policy: Approaches to managing organizational risk

Develop core policies within the first month, with additional policies to follow.

Board and Staff Training

Essential training topics include:

Director responsibilities: Legal duties and compliance obligations

CRA requirements: Overview of ongoing regulatory expectations

Receipting rules: Specific training on donation receipt requirements

T3010 filing: Information about annual reporting obligations

Financial oversight: Training on financial monitoring responsibilities

Risk management: Education about potential compliance pitfalls

Resource allocation: Guidelines for charitable resource use

Public benefit focus: Maintaining focus on charitable purposes

Initial training should occur within the first month, with ongoing education to follow.

Handling Charity Registration Delays

Sometimes the registration process takes longer than expected.

Identifying Delay Causes

Common delay factors include:

Application incompleteness: Missing information or documents

Purpose clarity issues: Vague or problematic purpose statements

Activity concerns: Activities not clearly furthering charitable purposes

Public benefit questions: Insufficient demonstration of public benefit

Private benefit flags: Potential undue benefits to individuals

CRA backlog: High volume of applications under review

Complex structures: Unusual or complicated organizational arrangements

International activities: Operations outside Canada requiring additional review

Response delays: Slow responses to CRA information requests

Identifying specific causes helps develop appropriate response strategies.

Appropriate Follow-up Techniques

Effective status inquiries include:

Timing appropriateness: Waiting reasonable periods before following up

Contact channel selection: Using appropriate communication methods

File number reference: Always including your application identifier

Tone management: Maintaining professional, courteous approach

Specific questions: Asking clear questions about status

Documentation: Recording all communications and responses

Realistic expectations: Understanding normal processing times

Escalation progression: Starting with basic inquiries before escalating

Balance persistence with patience and professionalism.

Escalation Options

If significant delays occur:

Supervisor inquiry: Requesting to speak with the examiner’s team leader

Formal complaint: Using CRA’s service complaint process if appropriate

Taxpayer Ombudsman: Contacting the Office of the Taxpayer Ombudsman

Director General inquiry: Writing to the Director General of the Charities Directorate

Problem Resolution Program: Accessing CRA’s internal resolution process

Written status request: Sending formal written inquiry about application status

Professional advocate engagement: Having legal counsel communicate on your behalf

Documentation of delays: Maintaining records of all communications and timeframes

Use escalation judiciously and progressively after reasonable waiting periods.

MP Assistance Possibilities

Parliamentary assistance options:

Constituency office inquiry: Requesting MP’s office to inquire about status

Ministerial inquiry: MP inquiry to Minister of National Revenue

Status verification: MP office can confirm application is in process

Process explanation: MP can help clarify procedures

Timing information: MP may obtain processing timeframe estimates

Documentation support: Providing MP with timeline and communication history

Reasonable expectations: Understanding limitations of MP intervention

Professional courtesy: Maintaining respectful approach in all communications

MP assistance can be helpful but has limitations in affecting substantive review.

Legal Intervention Considerations

Legal options for significant delays:

Legal opinion letters: Formal legal position on application merits

Mandamus application: Legal proceeding to compel decision (rare)

Judicial review: Court review of unreasonable delay (very rare)

Legal advocacy letters: Lawyer communication with Charities Directorate

Cost-benefit analysis: Evaluating whether legal intervention is worthwhile

Timing considerations: Understanding when legal options become viable

Success probability: Assessing likelihood of successful intervention

Relationship impact: Considering effect on long-term CRA relationship

Legal interventions are rarely necessary but may be appropriate in extreme cases.

Special Case Timelines for Charity Registration

Certain types of organizations face unique timeline considerations.

International Activities Impact

Organizations with international programs should expect:

Extended review periods: Typically 12-18+ months for approval

Multiple information requests: Detailed questions about international operations

Agency agreement scrutiny: Close examination of international partnerships

Direction and control focus: Emphasis on Canadian organization’s control

Documentation demands: Extensive requirements for international activities

Risk assessment: Thorough review of international risk factors

Country-specific questions: Varying scrutiny based on operational locations

Resource allocation examination: Close review of international spending

International activities consistently extend the registration timeline and require specialized planning.

Religious Organization Considerations

Faith-based organizations often experience:

Advancement of religion analysis: Assessment of whether activities advance religion

Public benefit scrutiny: Questions about benefit beyond adherents

Doctrine examination: Questions about religious teachings and practices

Governance structure review: Analysis of faith-based governance models

Private benefit concerns: Questions about benefits to religious leaders

Specialized examiner assignment: Review by examiners familiar with religious charities

Denominational comparison: Assessment against similar registered organizations

Historical precedent consideration: Evaluation based on established principles

Religious organizations typically face 8-14 month registration timelines.

Educational Institution Process

Educational organizations typically experience:

Advancement of education analysis: Assessment against educational criteria

Public benefit examination: Questions about accessibility and benefit

Curriculum review: Evaluation of educational content

Accreditation questions: Inquiries about educational standards

Student selection process: Review of how beneficiaries are chosen

Faculty qualification assessment: Questions about teacher qualifications

Facility evaluation: Inquiries about educational facilities

Tuition structure analysis: Review of fee structures and accessibility

Educational charities typically face 6-12 month registration timelines.

Healthcare Organization Specifics

Health-focused organizations often encounter:

Public benefit assessment: Questions about who receives services

Qualification verification: Inquiries about practitioner credentials

Treatment validation: Questions about evidence for therapeutic approaches

Accessibility review: Assessment of how beneficiaries access services

Specialized examiner assignment: Review by health charity specialists

Fee structure analysis: Examination of service costs to recipients

Overlap with public healthcare: Questions about relationship to public system

Facility standards: Inquiries about service delivery locations

Healthcare charities typically face 8-14 month registration timelines.

Foundation Registration Nuances

Foundations experience unique considerations:

Funding source scrutiny: Close examination of initial and ongoing funding

Disbursement planning: Review of grant-making plans

Arm’s length assessment: Analysis of board composition and relationships

Investment approach: Questions about fund management

Due diligence procedures: Inquiry into qualified donee assessment process

Private/public determination: Classification based on structure and funding

Donor direction examination: Questions about donor involvement in decisions

Specialized review team: Processing by foundation specialists

Private foundations typically face shorter timelines (3-4 months) than operating charities, while public foundations often fall within standard timeframes. For more details on foundations, see our article on charity vs. nonprofit status.

Accelerating Your Charity Registration in Canada

While much of the timeline is beyond your control, certain strategies can help.

Professional Assistance Benefits

Expert guidance provides:

Application quality improvement: Professional preparation meeting CRA expectations

Common error avoidance: Prevention of typical application mistakes

Thorough pre-submission review typically takes 1-2 weeks but prevents months of potential delays.

Complete Application Strategies

Develop a comprehensive application by:

Detailed activity descriptions: Providing thorough program explanations

Purpose-activity connection: Clearly linking activities to charitable purposes

Proactive question addressing: Anticipating and answering likely CRA questions

Comprehensive documentation: Including all relevant supporting materials

Organizational readiness evidence: Demonstrating capacity to operate

Complete Application Strategies (continued)

Develop a comprehensive application by:

Beneficiary clarification: Clearly defining who will benefit from your work

Public benefit demonstration: Showing how your work benefits the broader community

Private benefit mitigation: Explaining safeguards against improper private benefit

Financial sustainability evidence: Demonstrating viable funding model

Governance strength: Showing appropriate board composition and policies

Complete, proactive applications typically reduce total processing time by 2-4 months.

Follow-up Best Practices

Maintain appropriate communication through:

Status inquiries: Polite checks after reasonable waiting periods (typically 90 days)

Response timeliness: Prompt, thorough replies to CRA questions

Document tracking: Using delivery confirmation for all submissions

Contact consistency: Maintaining a single point of contact with CRA

Call documentation: Recording details of all phone conversations

Availability assurance: Ensuring your contact person is readily available

Professional tone: Maintaining courteous, cooperative communication

Patience with persistence: Balancing respect for process with appropriate follow-up

Effective follow-up and communication can prevent unnecessary delays of 1-3 months.

Alternative Approaches While Waiting

While awaiting registration, consider:

Fiscal sponsorship: Operating under another charity’s umbrella

Non-charitable programs: Conducting activities not requiring charitable status

Infrastructure development: Building organizational systems and policies

Network development: Building partnerships and community connections

Volunteer engagement: Developing volunteer base and programs

Board development: Strengthening governance knowledge and practices

Fundraising preparation: Developing donation systems and relationships

Program planning: Refining program models and implementation plans

These approaches allow meaningful progress while navigating the registration process.

Ready to navigate the charity registration process efficiently?

Work with Northfield & Associates for expert guidance through each stage, from initial planning to post-registration compliance, minimizing delays and maximizing your chances of successful registration.

Conclusion

The charity registration process in Canada involves multiple stages, each with its own timeline and variables. While the total process typically takes 8-18 months, understanding what to expect at each stage helps you plan effectively and minimize unnecessary delays.

By approaching each phase with thorough preparation, prompt responses to CRA inquiries, and appropriate follow-up, you can navigate the registration journey successfully. Remember that the investment of time and effort in proper registration establishes a strong foundation for your charitable work for years to come.

Whether you’re just beginning to explore charitable registration or are already in the midst of the process, maintaining realistic expectations and implementing the strategies outlined in this guide will help you achieve your goal of becoming a registered Canadian charity.

At Northfield & Associates our expert teams guidance on compliance requirements. Our team understands Canadian charity law and can help ensure your organisation follows proper procedures.

In this evolving economic landscape, collaboration with our firm offers clients a strategic advantage. With Cambodia’s reform-driven investment environment and Canada’s expanding footprint in Southeast Asia, our team of experienced consultants and legal advisors provides tailored guidance to help businesses navigate cross-border opportunities. We focus in developing comprehensive legal strategies, structuring international partnerships, and ensuring compliance in emerging markets.

By leveraging our regional insight and international expertise, you benefit from a trusted partner dedicated to helping you capitalize on growth potential in Cambodia and beyond.

Book a Consultation with Northfield & Associates

Your Trusted Partner in International Bilateral Relations

At Northfield & Associates are focus in Foreign Direct Investment (FDI), international trade missions, and cross-border legal strategy. Our team of experienced consultants and legal advisors offers tailored guidance and strategic insight to help you navigate the complexities of international partnerships and development opportunities.

Whether you choose to meet in person at one of our offices or connect virtually, we provide flexible and accessible consultation options. During your session, we’ll assess your goals, review key documentation, and guide you through every stage of your FDI or trade mission engagement.

Let us help you take the next step with confidence supported by trusted legal and strategic counsel every step of the way.

Take the First Step Today

If you believe you may be eligible for legal relief or simply need sound legal advice, we’re here to help. Contact us today to book your consultation. Let us provide the clarity, strategy, and peace of mind you need to move forward.

We serve our clients in English, Cambodian, Vietnamese, Mandarin and Cantonese, especially in Asian clients.

If you or anybody that you know, think that you meet the requirements and wish to receive further information.

We can help you start the application process and confirm eligibility requirements to participate.

We Offer Consultations & Meetings by Phone & Virtually. Affordable Fees.

Disclaimer:

The information contained in this article is provided for general information purposes only and does not constitute legal or other professional advice. Readers should seek tailored legal advice in relation to their personal circumstances.

Northfield & Associates International Corporation is a global consulting firm serving private enterprises, public institutions, not-for-profit organizations, and institutional capital providers. Operating across Cambodia, Canada, and global markets, the firm supports capital deployment, regulatory navigation, and enterprise decision-making in complex economic and geopolitical environments. Northfield & Associates delivers customized, execution-focused advisory solutions that drive measurable transformation, strengthen competitiveness, and enhance long-term highest value opportunities. The firm incorporates consulting, legal, regulatory, financial, and risk expertise to enable disciplined capital allocation, strong governance, and operational resilience. Northfield & Associates upholds a culture of applied insight and innovation, supporting clients across digital transformation, growth strategy, and organizational capability building. The firm advises individual, leading global corporations, midsize enterprises, government agencies, and mission-driven organizations through long-term partnerships. Enterprise-wide risk management, professional ethics, and fiduciary standards are embedded across all operations. Northfield & Associates’ diverse, globally unified teams are committed to execution certainty and sustainable, risk-adjusted returns aligned with ESG and stakeholder objectives.

Forward-Looking Information

This news release contains forward-looking information. All statements, other than statements of historic fact, that address activities, events or developments that the Company believes, expects or anticipates will or may occur in the future constitute forward-looking information.

This forward-looking information reflects the current expectations or beliefs of the Company based on information currently available to the Company.

Forward-looking information is subject to a number of risks and uncertainties that may cause the actual results of the Company to differ materially from those discussed in the forward-looking information, and even if such actual results are realized or substantially realized, there can be no assurance that they will have the expected consequences to, or effects on the Company. Factors that could cause actual results or events to differ materially from current expectations include, among other things: the failure to finalize negotiations concerning the increase of the Loan or to close such transaction and the failure of the Company to complete the acquisition of the Company Facility; operating performance of facilities; environmental and safety risks; delays in obtaining or failure to obtain necessary permits and approvals from government authorities; unavailability of plant, equipment or labour; inability to retain key management and personnel; changes to regulations or policies affecting the Company’s activities; and the other risks disclosed under the heading “Risk Factors” and elsewhere in the Company’s amended annual information.

Forward-looking information speaks only as of the date on which it is made and, except as may be required by applicable securities laws, the Company disclaims any intent or obligation to update any forward-looking information, whether as a result of new information, future events or results or otherwise. Although the Company believes that the assumptions inherent in the forward-looking information are reasonable, forward-looking information is not a guarantee of future performance and accordingly undue reliance should not be put on such information due to the inherent uncertainty therein.

Questions?

info@northfied.biz

Within Corporate Newsroom

Media Contact:

media@northfied.biz

Press contact

PR consultants press@northfied.biz

NOT LEGAL ADVICE. Information made available on this website in any form is for information purposes only. It is not, and should not be taken as, legal advice. You should not rely on, or take or fail to take any action based upon this information. Never disregard professional legal advice or delay in seeking legal advice because of something you have read on this website. Northfield & Associates professionals will be pleased to discuss resolutions to specific legal concerns you may have.

What are the steps to take to incorporate a federal nonprofit in Canada?

Creating a Federal Nonprofit can be a great way to establish a legal entity that can offer services and support to the community and provide a platform for fundraising, grant applications, and partnerships with other organizations. However, the incorporation process may be complex, so it is crucial to follow the steps carefully to ensure that all legal requirements are met.

Select and reserve a corporate name. The name must not directly conflict with a registered corporation or trademark.

Draft Forms 4001 – Articles of Incorporation and 4002 – Initial Directors and Head Office

Ensure that the corporate purposes, membership classes, disbursement clause, and additional provisions clauses reflect the organization’s long-term plans and needs. If you intend to apply for charitable status, the Articles must be drafted per the CRA requirements to qualify for charity status.

The Organization’s Directors must sign forms 4001 and 4002

Draft Articles of Not-for-Profit Incorporation must be signed before filing for incorporation.

File the Articles for Incorporation

The fee for NFP incorporation is $200.00.

Congratulations! You are now officially Incorporated.

Expect to receive the Certificate and registered Articles of Incorporation within 24 hours of applying.

Once you’ve received the Certificate and registered Articles of Incorporation, your nonprofit can start offering services to your community and building partnerships with other organizations. With careful planning and attention to legal requirements, your nonprofit can positively impact the world.

Make a difference in the complex process of incorporating a federal nonprofit. Follow these steps to establish a legal entity that can improve lives and communities.

In this evolving economic landscape, collaboration with our firm offers clients a strategic advantage. With Cambodia’s reform-driven investment environment and Canada’s expanding footprint in Southeast Asia, our team of experienced consultants and legal advisors provides tailored guidance to help businesses navigate cross-border opportunities. We focus in developing comprehensive legal strategies, structuring international partnerships, and ensuring compliance in emerging markets.

By leveraging our regional insight and international expertise, you benefit from a trusted partner dedicated to helping you capitalize on growth potential in Cambodia and beyond.

Book a Consultation with Northfield & Associates

Your Trusted Partner in International Bilateral Relations

At Northfield & Associates are focus in Foreign Direct Investment (FDI), international trade missions, and cross-border legal strategy. Our team of experienced consultants and legal advisors offers tailored guidance and strategic insight to help you navigate the complexities of international partnerships and development opportunities.

Whether you choose to meet in person at one of our offices or connect virtually, we provide flexible and accessible consultation options. During your session, we’ll assess your goals, review key documentation, and guide you through every stage of your FDI or trade mission engagement.

Let us help you take the next step with confidence supported by trusted legal and strategic counsel every step of the way.

Take the First Step Today

If you believe you may be eligible for legal relief or simply need sound legal advice, we’re here to help. Contact us today to book your consultation. Let us provide the clarity, strategy, and peace of mind you need to move forward.

We serve our clients in English, Cambodian, Vietnamese, Mandarin and Cantonese, especially in Asian clients.

If you or anybody that you know, think that you meet the requirements and wish to receive further information.

We can help you start the application process and confirm eligibility requirements to participate.

We Offer Consultations & Meetings by Phone & Virtually. Affordable Fees.

Disclaimer:

The information contained in this article is provided for general information purposes only and does not constitute legal or other professional advice. Readers should seek tailored legal advice in relation to their personal circumstances.

Northfield & Associates International Corporation is a global consulting firm serving private enterprises, public institutions, not-for-profit organizations, and institutional capital providers. Operating across Cambodia, Canada, and global markets, the firm supports capital deployment, regulatory navigation, and enterprise decision-making in complex economic and geopolitical environments. Northfield & Associates delivers customized, execution-focused advisory solutions that drive measurable transformation, strengthen competitiveness, and enhance long-term highest value opportunities. The firm incorporates consulting, legal, regulatory, financial, and risk expertise to enable disciplined capital allocation, strong governance, and operational resilience. Northfield & Associates upholds a culture of applied insight and innovation, supporting clients across digital transformation, growth strategy, and organizational capability building. The firm advises individual, leading global corporations, midsize enterprises, government agencies, and mission-driven organizations through long-term partnerships. Enterprise-wide risk management, professional ethics, and fiduciary standards are embedded across all operations. Northfield & Associates’ diverse, globally unified teams are committed to execution certainty and sustainable, risk-adjusted returns aligned with ESG and stakeholder objectives.

Forward-Looking Information

This news release contains forward-looking information. All statements, other than statements of historic fact, that address activities, events or developments that the Company believes, expects or anticipates will or may occur in the future constitute forward-looking information.

This forward-looking information reflects the current expectations or beliefs of the Company based on information currently available to the Company.

Forward-looking information is subject to a number of risks and uncertainties that may cause the actual results of the Company to differ materially from those discussed in the forward-looking information, and even if such actual results are realized or substantially realized, there can be no assurance that they will have the expected consequences to, or effects on the Company. Factors that could cause actual results or events to differ materially from current expectations include, among other things: the failure to finalize negotiations concerning the increase of the Loan or to close such transaction and the failure of the Company to complete the acquisition of the Company Facility; operating performance of facilities; environmental and safety risks; delays in obtaining or failure to obtain necessary permits and approvals from government authorities; unavailability of plant, equipment or labour; inability to retain key management and personnel; changes to regulations or policies affecting the Company’s activities; and the other risks disclosed under the heading “Risk Factors” and elsewhere in the Company’s amended annual information.

Forward-looking information speaks only as of the date on which it is made and, except as may be required by applicable securities laws, the Company disclaims any intent or obligation to update any forward-looking information, whether as a result of new information, future events or results or otherwise. Although the Company believes that the assumptions inherent in the forward-looking information are reasonable, forward-looking information is not a guarantee of future performance and accordingly undue reliance should not be put on such information due to the inherent uncertainty therein.

Questions?

info@northfied.biz

Within Corporate Newsroom

Media Contact:

media@northfied.biz

Press contact

PR consultants press@northfied.biz

NOT LEGAL ADVICE. Information made available on this website in any form is for information purposes only. It is not, and should not be taken as, legal advice. You should not rely on, or take or fail to take any action based upon this information. Never disregard professional legal advice or delay in seeking legal advice because of something you have read on this website. Northfield & Associates professionals will be pleased to discuss resolutions to specific legal concerns you may have.

Social Activities and Charitable Organizations: It’s a Fine Line

If you are considering registering a charity in Canada, you probably have some lofty goals. Charities are, after all, organizations that are established to uplift and empower. They aim to reduce poverty, increase participation in society, and alleviate suffering.

However, if you were thinking that you would simply host endless high brow soirees to fill the coffers of your organization, there may be a bump in the road. That’s because there are some fairly strict guidelines about what kind of social activities charities can host, and how often they can do so.

A Matter of Definitions

While people sometimes mix up charities and non-profits, Canadian law is actually quite clear that while non-profits can be social, sporting or community organizations, charities have to be predominantly engaged in charitable work. This is actually quite narrowly defined in the law.

Which means that if your charity spends too much time hosting social events, even if it’s for fundraising, you could very well cross the line between these two types of organizations.

In fact, if your charity hosts too many of these types of events, it could be seen as the primary purpose of the organization, which may even cause you to lose your registered charity status.

All of this is very bad news for charities, but it can happen surprisingly easily if you’re not very careful.

Clearly for Fund Raising

Another good piece of advice for anyone who either runs or plans to create a charity is to make sure that any social events you do host are very clearly for fund raising purposes.

The authorities recognize that charities need to raise funds to continue their work, and it is accepted that one way to do this is to host various events. So, whether it is a dinner or a fashion show, a party, or a fun run, make sure that there is a clear element of fund-raising built in.

Make sure that there’s an entry fee to community events, or that the tickets for a formal event are sufficient that they will put money into your organizations accounts that can be used for your charitable work.

All About Proportions

In order to keep your charity on the charitable side of the line, it’s recommended that not more than 10% of your time, funds, resources, and property is devoted to social activities.

It’s a good idea to set up formal methods of measuring this too. While most people want to give charities the benefit of the doubt, if you are consistently overstepping this unwritten guideline, you might get yourself into some trouble.

Focus on the Mission

People who start and work for charities should always be driven by their mission. There’s a reason why you created this organization, and there are people out there who need your help.

If you focus most of your efforts on delivering that help and publicizing that message, you should automatically stay on the right side of the social activities line. Everything you do should be built around the idea of giving as much of the money you raise to the organizations and individuals you support.

Consult a Professional

Fund raising for charities is actually quite a complex matter, since there are many restrictions like this. Aside from limits on the proportion of your time you can spend on social activities, even when they support your fundraising efforts, there are other business activity limitations that apply.

Most people who start a charity are driven by the mission and have the very best intentions. But even the best intentions don’t always put you in the best legal position. So, if you are not sure what you can and can’t do in your charity, be it related to social events or something else, it’s best to talk to a professional.

Create clear guidelines to be implemented in your organization about what can and cannot be done based on their advice. Base your fund-raising activities around these guidelines, so you stay on the right side of the law and of the CRA. Make sure that you are not spending too much of the money you do raise hosting events.

Charities are usually experts in their field. But they don’t always know how to maximize their impact on the world. A legal or tax specialist can help to ensure that your big dreams to change the world aren’t detailed by technicalities.

At Northfield & Associates our expert teams guidance on compliance requirements. Our team understands Canadian charity law and can help ensure your organisation follows proper procedures.

In this evolving economic landscape, collaboration with our firm offers clients a strategic advantage. With Cambodia’s reform-driven investment environment and Canada’s expanding footprint in Southeast Asia, our team of experienced consultants and legal advisors provides tailored guidance to help businesses navigate cross-border opportunities. We focus in developing comprehensive legal strategies, structuring international partnerships, and ensuring compliance in emerging markets.

By leveraging our regional insight and international expertise, you benefit from a trusted partner dedicated to helping you capitalize on growth potential in Cambodia and beyond.

Book a Consultation with Northfield & Associates

Your Trusted Partner in International Bilateral Relations

At Northfield & Associates are focus in Foreign Direct Investment (FDI), international trade missions, and cross-border legal strategy. Our team of experienced consultants and legal advisors offers tailored guidance and strategic insight to help you navigate the complexities of international partnerships and development opportunities.

Whether you choose to meet in person at one of our offices or connect virtually, we provide flexible and accessible consultation options. During your session, we’ll assess your goals, review key documentation, and guide you through every stage of your FDI or trade mission engagement.

Let us help you take the next step with confidence supported by trusted legal and strategic counsel every step of the way.

Take the First Step Today

If you believe you may be eligible for legal relief or simply need sound legal advice, we’re here to help. Contact us today to book your consultation. Let us provide the clarity, strategy, and peace of mind you need to move forward.

We serve our clients in English, Cambodian, Vietnamese, Mandarin and Cantonese, especially in Asian clients.

If you or anybody that you know, think that you meet the requirements and wish to receive further information.

We can help you start the application process and confirm eligibility requirements to participate.

We Offer Consultations & Meetings by Phone & Virtually. Affordable Fees.

Disclaimer:

The information contained in this article is provided for general information purposes only and does not constitute legal or other professional advice. Readers should seek tailored legal advice in relation to their personal circumstances.

Northfield & Associates International Corporation is a global consulting firm serving private enterprises, public institutions, not-for-profit organizations, and institutional capital providers. Operating across Cambodia, Canada, and global markets, the firm supports capital deployment, regulatory navigation, and enterprise decision-making in complex economic and geopolitical environments. Northfield & Associates delivers customized, execution-focused advisory solutions that drive measurable transformation, strengthen competitiveness, and enhance long-term highest value opportunities. The firm incorporates consulting, legal, regulatory, financial, and risk expertise to enable disciplined capital allocation, strong governance, and operational resilience. Northfield & Associates upholds a culture of applied insight and innovation, supporting clients across digital transformation, growth strategy, and organizational capability building. The firm advises individual, leading global corporations, midsize enterprises, government agencies, and mission-driven organizations through long-term partnerships. Enterprise-wide risk management, professional ethics, and fiduciary standards are embedded across all operations. Northfield & Associates’ diverse, globally unified teams are committed to execution certainty and sustainable, risk-adjusted returns aligned with ESG and stakeholder objectives.

Forward-Looking Information

This news release contains forward-looking information. All statements, other than statements of historic fact, that address activities, events or developments that the Company believes, expects or anticipates will or may occur in the future constitute forward-looking information.

This forward-looking information reflects the current expectations or beliefs of the Company based on information currently available to the Company.

Forward-looking information is subject to a number of risks and uncertainties that may cause the actual results of the Company to differ materially from those discussed in the forward-looking information, and even if such actual results are realized or substantially realized, there can be no assurance that they will have the expected consequences to, or effects on the Company. Factors that could cause actual results or events to differ materially from current expectations include, among other things: the failure to finalize negotiations concerning the increase of the Loan or to close such transaction and the failure of the Company to complete the acquisition of the Company Facility; operating performance of facilities; environmental and safety risks; delays in obtaining or failure to obtain necessary permits and approvals from government authorities; unavailability of plant, equipment or labour; inability to retain key management and personnel; changes to regulations or policies affecting the Company’s activities; and the other risks disclosed under the heading “Risk Factors” and elsewhere in the Company’s amended annual information.

Forward-looking information speaks only as of the date on which it is made and, except as may be required by applicable securities laws, the Company disclaims any intent or obligation to update any forward-looking information, whether as a result of new information, future events or results or otherwise. Although the Company believes that the assumptions inherent in the forward-looking information are reasonable, forward-looking information is not a guarantee of future performance and accordingly undue reliance should not be put on such information due to the inherent uncertainty therein.

Questions?

info@northfied.biz

Within Corporate Newsroom

Media Contact:

media@northfied.biz

Press contact

PR consultants press@northfied.biz

NOT LEGAL ADVICE. Information made available on this website in any form is for information purposes only. It is not, and should not be taken as, legal advice. You should not rely on, or take or fail to take any action based upon this information. Never disregard professional legal advice or delay in seeking legal advice because of something you have read on this website. Northfield & Associates professionals will be pleased to discuss resolutions to specific legal concerns you may have.

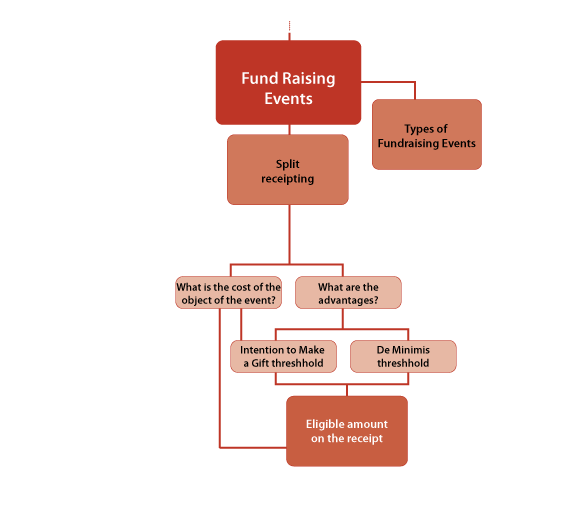

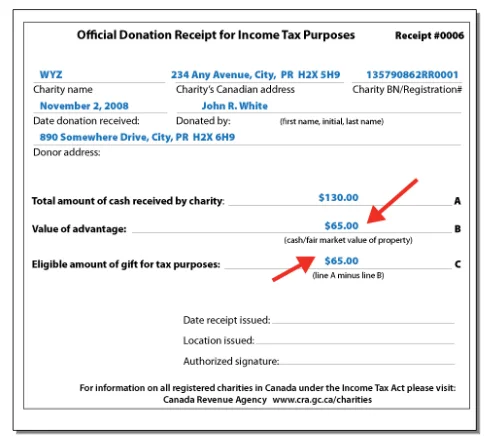

This module provides basic information on advantages. The key areas covered are: What is an advantage? What is split receipting? Advantages and split receipting. How does it work? The importance of Fair Market Value to advantages.

Introduction

This module introduces you to CRA’s Four Part Test.

This is one of two tests that CRA uses to determine if an activity is considered a fundraising or a charitable activity and how the activity‘s expenses have to be reported based on the result of this test.

Note: The other test is the Substantially All Test. Information on the Substantially All Test is available here.

Purpose

The Four Part Test is in the form of four main questions:

Was fundraising the main objective of the activity?

Did the activity include on-going or repeated requests, emotive requests, gift incentives, donor premiums, or other fundraising merchandise?

Was the audience selected based on its ability to give?

Was commission-based remuneration or compensation based on the number or amount of donations?

If you answer “no” to all four questions, a portion of the expenses related to the activity can be reported on the T3010 as charitable, management, or political expenses as applicable and a portion can be reported as fundraising expenses on the T3010.

If you answer “yes” to any one question, all of the activity’s expenses have to be reported as fundraising expenses on the T3010 form.

Example

Charity Z has the mission of helping seniors live a healthy and safe lives. One of its program is the prevention of elder abuse. Charity Z publishes and sends out a 4-page brochure to the general public on:

signs of elder abuse

the public should take action to stop elder abuse

how Charity Z can help

other community resources

The back cover of the brochure describes the programs of Charity Z with a note stating that donations are welcome to support the programs.

The staff and volunteer prepare and mail out this brochure as part of their regular activities. There is no compensation based on the number of donations received.

Explanation: Applying the Four Part Test to the Case of Charity Z

Fundraising is not the main objective of the activity. The purpose of the brochure is to inform the public about elder abuse and to urge them to take action. Less than 25% of the brochure content is about donations.

The brochure does not include on-going, repeated or emotive requests for donations.

The audience was not selected based on its ability to give.

There is no commission-based remuneration or compensation.

A majority of the expenses are to be allocated as charitable expenses with less than 25% as fundraising expenses.

Main Objective

Question 1: Was fundraising the main objective of the activity?

To determine whether the main object of an activity is fundraising, the CRA looks at three things:

the amount of resources devoted to the fundraising component of the activity

the nature of the activity

the content of the activity

Each of these areas is explained more below:

1(a) Amount of Resources

The amount of resources devoted to the fundraising component of the activity.

CRA considers resources to include all of a charity’s financial assets and resources such as staff, volunteers, directors, space, and equipment that the charity can use to further its purposes.

If most of your resources are used for fundraising purposes as reflected in the amount of content and the cost, then the main objective of the activity is fundraising. This is possible even if some resources are used for other objectives.

1(b) Nature of the Activity

These activities by its nature are generally considered as fundraising activities.

Paid advertisement except when the ad is only on the charity’s programs and services.

Infomercial

Telemarketing

Activities with content related to charitable gaming

Activities with content related to products and services being sold as a fundraiser by or on behalf of the charity.

Note: Free Public Service Announcement (PSA) is generally not considered a fundraising activity.

1(c) Content of the Activity

When your activity has both fundraising and charitable components, it may be difficult to separate the two components.

For example, a charity working with autistic children arranges for a television interview to discuss the challenges faced by them and their families. While talking about the issue, the need for funds and how people can donate is discussed. So how can the charitable component be distinguished from the fundraising component?

CRA looks for four features in the content of the activity to determine if it is a fundraising activity or not. In general, if an activity contains one of the features, it is a charitable activity and expenses should be allocated accordingly.

The four features of the contents of an activity that CRA looks for are:

to advance the programs and services of the charity

to raise awareness of an issue

to provide useful information to the public or the stakeholders about the charity’s work or an issue related to that work

to be transparent and accountable for its practices by providing information about its structure, operations, or performance to the public and to its stakeholders.

Each of these features of the contents of an activity is explored in detail below:

Advancing Programs and Services

If the main objective of your activity is:

to provide information to further the objectives of the charity

with

the beneficiaries or potential beneficiaries of the charity as the primary audience

This activity will generally be considered a charitable activity. The expenditures associated with the activity are thus to be reported as charitable expenditures.

Exception: When the programs and services of a charity are profiled as a means to encourage donations, the activity is considered a fundraising activity. The expenses incurred are considered fundraising expenditures.

Example:

A brochure describing the services of a seniors’ centre is distributed to seniors’ households in the area served by the centre.

Costs of the resources for this activity are considered charitable expenses since object of the activity is to further the centre as charitable objectives.

Raising Awareness

Raising awareness among the public or a segment of the public may be considered a charitable activity as long as:

it will fulfill the charity’s objective

OR

the charity has expertise on a matter of public concern

Example: