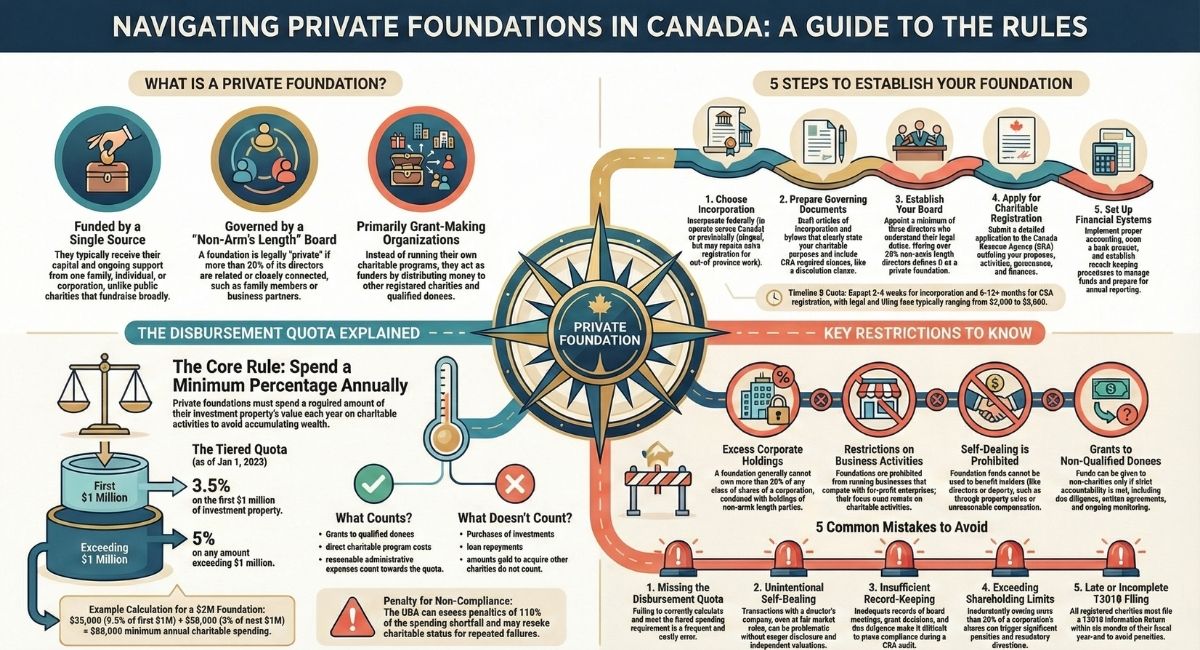

What is the Cost to Register a Charity in Canada?

Registering a charity in Canada is a meaningful endeavor, but it’s important to be aware of the financial responsibilities involved. From legal fees to ongoing administrative costs, understanding these expenses can help you plan effectively. In this detailed guide, we’ll explore the various costs associated with setting up a registered charity in Canada, helping you navigate the process with confidence.

Quick Cost Overview: At a Glance

Before diving into the details, here’s a snapshot of the main costs you’ll encounter when registering and maintaining a charity in Canada:

| Cost Category | One-Time Costs | Annual Costs |

|---|---|---|

| Legal Fees (Registration) | $2,500 – $7,500 | — |

| Incorporation | $200 – $750 | — |

| Accounting & Financial Statements | — | $1,000+ |

| T3010 Filing | — | $1,000+ |

| Liability Insurance | — | $700 – $2,000 |

| Fundraising Expenses | — | 10-15% of funds raised |

| Governance Costs | — | $500 – $5,000 |

| Software & Technology | — | $500 – $3,000 |

| Total Estimated Range | $2,700 – $8,250 | $3,700 – $12,000+ |

Now let’s break down each of these costs in detail.

Understanding Registered Charities in Canada

Registering a charity in Canada is a meaningful endeavour, but it’s important to be aware of the financial responsibilities involved. From legal fees to ongoing administrative costs, understanding these expenses can help you plan effectively. In this detailed guide, we’ll explore the various costs associated with setting up a registered charity in Canada, helping you navigate the process with confidence.

A registered charity in Canada is an organization that is officially recognized by the Canada Revenue Agency (CRA) – Charities Directorate, allowing it to issue tax receipts for donations and benefit from tax exemptions. Registered charities must operate exclusively for charitable purposes as defined by Canadian law, and they are subject to regulatory oversight to ensure compliance with the Income Tax Act.

Upfront Costs for Charity Registration

Legal Fees for Charity Registration

To register a charity with the CRA, you must submit an Application to Register a Charity under the Income Tax Act. There is no government fee to submit this form, but many organizations seek the assistance of experienced charity lawyers or a charity law firm to ensure the application is thorough, accurate, and likely to be successful. Mistakes in the application can result in significant delays or even rejection (the CRA typically rejects over 50% of charity applications), making charity law counsel a valuable and frequently crucial investment.

What’s Included in Legal Fees?

When you hire a charity lawyer, understanding what’s covered in their fee structure is essential. Comprehensive legal services for charity registration should include:

- Document Preparation: Drafting your governing documents, charitable purposes, and all required application materials

- CRA Correspondence: All communication with the CRA throughout the application process, including responding to questions and requests for additional information

- Application Review & Revisions: Multiple rounds of review and refinement to ensure your application meets CRA standards

- Consultation Hours: Strategic advice on structuring your charity, choosing the right charitable category, and planning for compliance

- Registration Support: Guidance from incorporation through to final CRA approval

Watch Out for Hidden Legal Costs: Some charity lawyers quote an attractive fixed fee but include significant carve-outs that can add thousands of dollars to your final bill. Common extra charges include:

- CRA correspondence and follow-up questions ($200-$500 per response)

- Revisions beyond a set number ($150-$300 per revision)

- Phone consultations after initial meetings ($250-$400 per hour)

- Document amendments during the process ($500-$1,500)

Questions to Ask Your Charity Lawyer

When selecting legal counsel for charity registration, consider asking:

(1) What is your charity registration success rate?

(2) Does your quote for legal fees include everything, including any questions relating to the charity formation and registration, as well as all correspondence with the CRA until the charity is registered (some charity lawyers quote a fixed fee, but neglect to advise that there are significant carve outs to the quote, including CRA correspondence, which can often run many additional thousands of dollars. It’s critical to ensure that the quote for charity registration includes A-Z, from incorporation through CRA Charity Registration)?; and

(3) Do you provide your charity application clients a 100% money-back guarantee of registration?

Incorporation Costs

While it’s not mandatory for all charities, many opt to incorporate to protect their directors and add a formal structure to their operations. Incorporation can be done at either the federal or provincial level.

Federal vs. Provincial Incorporation: Cost Comparison

Choosing between federal and provincial incorporation affects both your initial costs and your charity’s operational scope. Here’s what you need to know:

Federal Incorporation:

- Online filing: $200

- Paper filing: $250

- Benefits: Operate across all provinces and territories, name protection nationwide, perceived credibility for national organizations

- Best for: Charities planning multi-provincial operations or national fundraising campaigns

Provincial Incorporation Costs:

- Ontario: $155 (online) | $175 (mail)

- British Columbia: $100 (online) | $150 (paper)

- Alberta: $100 (online)

- Quebec: $163 (requires bilingual documentation, which may increase translation costs by $500-$2,000)

- Nova Scotia: $150

- Manitoba: $150

Important Considerations:

- Provincial incorporation limits operations to that province without extra-provincial registration

- Extra-provincial registration in additional provinces costs $100-$350 per province

- Some provinces require annual corporate filings ($20-$40) in addition to CRA requirements

- Federal corporations must file annual corporate returns ($20 online)

Cost-Saving Tip: If you’re unsure about your geographic scope, federal incorporation provides flexibility without the hassle of multiple provincial registrations later.

Ongoing Annual Costs for Registered Charities

Once your charity is registered, there are several recurring costs to consider. These expenses are essential to maintaining compliance with CRA regulations and ensuring the smooth operation of your organization.

Accounting and Financial Statements ($1,000+)

Registered charities are required to submit annual financial statements to the CRA, regardless of size. While smaller organizations with simple financials may be able to handle this internally, most charities hire professional accountants or bookkeepers. Accounting services for preparing financial statements start at $1,000 for very small charities, and rise proportionally for larger charities, depending on the complexity of the charity’s operations and volume of revenue. Larger organizations may also need to undergo audits, which could increase this cost.

T3010 Filing Costs ($1,000+)

Every registered charity in Canada must file a T3010 form (Registered Charity Information Return) annually. This form details the charity’s financial activities and ensures compliance with CRA rules. While smaller organizations may handle this task internally, many charities choose to hire an accounting firm, with costs starting at $1,000.

Fundraising Expenses (10-15% of Funds Raised)

Fundraising is a key part of any charity’s financial plan, but it also comes with costs. Whether your charity relies on events, professional fundraisers, online donations, or direct mail campaigns, it’s essential to budget for fundraising expenses. These costs can vary significantly depending on the method used but generally range between 10% to 15% of the total funds raised. For example, organizing a charity gala may involve renting a venue, hiring staff, and producing marketing materials, all of which contribute to the fundraising budget.

Governance and Board Meeting Costs ($500 – $5,000)

Strong governance is vital for any charity’s success. This includes maintaining an active board of directors, holding regular meetings, and ensuring that all necessary governance documents are up to date. Depending on the size of the charity, these governance costs could range from $500 to $5,000 per year, including expenses such as meeting room rentals, travel reimbursements for board members, and filing fees for updating incorporation documents.

Liability Insurance ($700 – $2,000)

Liability insurance is often necessary for charities, especially those running public programs or events. The cost of insurance can vary depending on the nature of the charity’s activities, with most organizations spending between $700 and $2,000 per year on basic coverage.

Additional Operating Costs to Consider

In addition to the primary costs mentioned above, charities may incur other expenses depending on their specific needs and operations.

Software and Technology ($500 – $3,000)

Many charities rely on software to manage donors, track finances, and automate their communications. Popular options like donor management software, accounting programs, and customer relationship management (CRM) tools can cost between $500 and $3,000 annually, depending on the size of the organization and the features required.

Staff Training and Professional Development ($100 – $1,000 per person)

Investing in staff training is essential to keep up with evolving regulations and best practices. Charities often provide professional development opportunities for their team members, which may include attending conferences, workshops, or online courses. Training costs can range from $100 to $1,000 per staff member annually.

Office Space and Utilities ($500 – $10,000)

If your charity requires physical office space, rent and utilities can be significant expenses. While some smaller charities operate out of home offices or shared spaces, others may require dedicated office space, with costs ranging from $500 to $10,000 annually, depending on the location and size.

Hidden Costs Many Charities Overlook

When budgeting for your charity, don’t forget these often-overlooked expenses that can catch new organizations off guard:

Translation Services (Quebec & Bilingual Requirements) — $500 – $2,000

Charities operating in Quebec or providing services in both official languages need bilingual documentation. This includes:

- Governing documents and bylaws translation

- Fundraising materials in both English and French

- Website content translation

- Annual reports and public communications

Professional translation services for charity documents typically cost $0.15-$0.25 per word, with full document packages ranging from $500 to $2,000.

CRA Audit Response Legal Fees — $3,000 – $10,000

If the CRA selects your charity for an audit or compliance review (which happens to approximately 1 in 10 charities over a five-year period), you’ll likely need legal representation. Costs include:

- Reviewing CRA audit letters and information requests

- Preparing comprehensive responses

- Representing your charity in discussions with the CRA

- Implementing recommended changes

Budget for $3,000-$10,000 in legal fees if your charity faces a CRA audit.

Amendment Fees (Changing Purposes or Structure) — $500 – $3,000

As your charity evolves, you may need to amend your governing documents or charitable purposes. This requires:

- Legal review and document drafting: $500-$1,500

- CRA approval process support: $500-$1,000

- Provincial corporate filing fees: $50-$200

- Legal correspondence with CRA: $500-$1,500

Total amendment costs typically range from $500 to $3,000, depending on complexity.

Bank Fees and Payment Processing — 2-3% of Donations

Don’t forget the ongoing costs of accepting donations:

- Credit card processing fees: 2.5-3% per transaction

- Monthly bank account fees: $15-$50 for charity accounts

- Online donation platform fees: 2-5% plus $0.30 per transaction

- Cheque printing and bank drafts: $50-$200 annually

For a charity receiving $50,000 in donations annually, expect $1,000-$1,500 in banking and processing fees.

Website Hosting, Domain, and Maintenance — $200 – $1,000/year

A professional online presence is essential for credibility and fundraising:

- Domain registration: $15-$50/year

- Website hosting: $100-$400/year

- SSL certificate (security): $0-$100/year (often free)

- Website maintenance and updates: $0-$500/year

- Email hosting (professional addresses): $60-$150/year

Budget $200-$1,000 annually depending on your website’s complexity.

Legal Compliance and Policy Updates — $500 – $2,000

Laws change, and your charity needs to stay compliant:

- Annual policy reviews and updates

- Privacy policy compliance (PIPEDA)

- Employment law updates

- Contract reviews for partnerships or leases

- Legal advice on new activities or programs

Annual legal compliance work typically costs $500-$2,000 for established charities.

Cost-Saving Strategies for New Charities

Starting a charity on a limited budget? Here are proven strategies to reduce your initial and ongoing costs:

1. Start with Federal Incorporation

Federal incorporation costs slightly more upfront ($200 vs. $100-$155 provincially) but saves money long-term if you plan to operate in multiple provinces. Registering extra-provincially in each province later costs $100-$350 per province.

2. Use Free or Low-Cost Software Initially

Many software providers offer discounted or free plans for nonprofits:

- Google Workspace for Nonprofits: Free (email, cloud storage, collaboration tools)

- Microsoft 365 for Nonprofits: Free or heavily discounted

- Canva for Nonprofits: Free design tool

- Mailchimp: Free up to 500 subscribers

- Wave Accounting: Free accounting software

Upgrade to paid versions as your charity grows and requires advanced features.

3. Leverage Volunteer Expertise

Recruit board members and volunteers with professional skills:

- Accountants or bookkeepers for financial statement preparation

- Lawyers for contract reviews and basic legal questions

- Marketing professionals for fundraising campaigns

- IT specialists for website and tech support

Important: While volunteers can help with routine tasks, always use licensed professionals for CRA submissions, charity registration, and audits.

4. Apply for Start-Up Grants

Several organizations provide grants specifically for charity start-up costs:

- Community foundations often have capacity-building grants ($1,000-$5,000)

- Provincial government programs support social enterprises and nonprofits

- Corporate sponsorships may cover incorporation or registration costs

- National organizations like Community Foundations of Canada offer support

Research grants available in your province or sector.

5. Consider Fiscal Sponsorship Temporarily

If registration costs are prohibitive, work under an existing charity’s umbrella through fiscal sponsorship:

- Benefits: Immediate tax receipt issuing, lower overhead, mentorship, shared services

- Costs: 5-15% administrative fee on donations received

- Timeline: Use fiscal sponsorship while saving for full registration (typically 1-2 years)

Once you’ve built capacity and funding, transition to independent registration.

6. Bundle Services for Better Rates

Many charity service providers offer package deals:

- Combined incorporation + registration: Save $500-$1,000

- Annual accounting + T3010 filing: Save $200-$500

- Multi-year retainer agreements with lawyers: Save 10-20%

Ask potential service providers if they offer bundled pricing.

7. Join Sector Associations for Resources

Membership in charity sector associations provides:

- Discounted legal and accounting services

- Free templates and policy documents

- Training webinars and workshops

- Networking and mentorship opportunities

Examples:

- Imagine Canada

- Ontario Nonprofit Network

- Provincial nonprofit associations

Membership fees ($100-$500/year) often pay for themselves through savings on services and resources.

Timeline: What to Expect During the Registration Process

Understanding the registration timeline helps you plan effectively and budget for the entire journey:

Month 1-2: Preparation Phase

- Initial consultations with lawyers

- Drafting governing documents

- Defining charitable purposes

- Establishing board of directors

- Costs incurred: Initial legal fees, incorporation fees

Month 3-4: Application Submission

- Final application review

- CRA submission

- Await initial CRA response

- Costs incurred: Remaining legal fees

Month 5-9: CRA Review Period

- CRA reviews application

- Potential questions or requests for clarification

- Lawyer responds to CRA inquiries

- Costs incurred: None if comprehensive legal package; $200-$500 per response if not included

Month 10-12: Final Approval

- CRA issues registration approval

- Charity number assigned

- Begin operations as registered charity

- Costs incurred: Initial annual costs begin (insurance, bank accounts, etc.)

Total Timeline: 6-12 months on average, though complex applications may take longer.

Conclusion

Setting up a registered charity in Canada involves a range of costs, from initial legal fees to ongoing expenses for compliance and governance. By planning ahead and understanding these costs, you can ensure your charity is financially prepared for both the registration process and long-term operations.

Total Initial Investment: Expect to invest $2,700 to $8,250 in your first year for incorporation, legal fees, and initial setup costs.

Annual Operating Costs: Budget $2,500 to $12,000+ annually depending on your charity’s size and complexity.

While the financial commitment may seem substantial, the benefits of charitable status—including tax exemptions and the ability to issue donation receipts to donors, thereby encouraging increased donations—make the investment worthwhile for most organizations.

Regional Considerations: Costs may vary by province, particularly in Quebec where bilingual documentation is required, potentially adding $500-$2,000 in translation costs. Additionally, provincial incorporation fees and annual filing requirements differ across Canada, so research your specific province’s requirements.

The registration process typically takes 6 to 12 months from application to approval, so factor this timeline into your planning and budget accordingly.

Ready to Start Your Charity? We’re Here to Help

Looking to start a charity? Contact the experienced and knowledgeable Charity Registration Lawyers at B.I.G. Charity Law Group for a streamlined, affordable and efficient charity registration.

Contact Us Today:

Phone: 416-488-5888

Email: ask@charitylawgroup.ca

Schedule a Free Consultation: Book your free, 15-minute meeting with our legal team here where we can answer all your questions about registering your charity in Canada.

Charity and Nonprofit Law: It’s all we do.

Frequently Asked Questions

How long does charity registration take in Canada?

The charity registration process typically takes 6 to 12 months from initial application submission to final CRA approval. However, timelines vary based on several factors:

- Application complexity: Simple applications may be approved in 4-6 months, while complex structures can take 12-18 months

- CRA workload: Processing times fluctuate based on the CRA’s backlog

- Completeness of application: Applications requiring multiple rounds of CRA questions take longer

- Time of year: Applications submitted in early fall may face delays due to year-end processing

Pro tip: Working with experienced charity lawyers often reduces processing time by 2-4 months because applications are complete and error-free from the start.

Can I get a refund if my charity application is rejected?

Refund policies depend entirely on your legal service provider:

- CRA fees: The CRA doesn’t charge application fees, so there’s nothing to refund from them

- Legal fees: Most charity lawyers do not offer refunds for rejected applications because significant work was still completed

- Our guarantee: At B.I.G. Charity Law Group, we provide a 100% money-back guarantee if your charity application is rejected—a unique offering in the industry that reflects our confidence in our registration success rate

Always clarify refund policies in writing before engaging legal services.

Do I need a lawyer to register a charity in Canada?

No, hiring a lawyer is not legally required to register a charity. You can complete and submit the CRA application yourself at no cost.

However, legal representation is highly recommended because:

- The CRA rejects over 50% of charity applications, often due to incomplete documentation, unclear charitable purposes, or inadequate governance structures

- Rejected applications waste 6-12 months and require complete resubmission

- Lawyers experienced in charity law understand CRA requirements and anticipate potential issues

- Professional applications are typically approved faster with fewer rounds of CRA questions

Bottom line: While you can register without a lawyer, the investment in professional legal services ($2,500-$7,500) significantly increases your chances of success and saves time.

What happens if I can’t afford the registration costs?

If charity registration costs are beyond your current budget, consider these alternatives:

1. Fiscal Sponsorship Work under an existing charity’s registration for 1-2 years while building capacity. Sponsors typically charge 5-15% of donations but provide immediate tax-receipting ability.

2. Phased Approach Operate as an unincorporated nonprofit initially (no tax receipts) and transition to registered charity status once you’ve raised sufficient funds.

3. Start-Up Grants Apply for capacity-building grants from community foundations, corporate sponsors, or government programs that specifically support new nonprofits.

4. Payment Plans Some charity lawyers offer installment payment plans for registration fees, allowing you to spread costs over 6-12 months.

5. Pro Bono Services Law schools and legal clinics occasionally provide pro bono charity registration support, though availability is limited and competitive.

Are there government grants to help with registration costs?

While there’s no federal grant specifically for charity registration costs, several funding sources can help:

Provincial Programs:

- Ontario Trillium Foundation: Seed grants for new organizations ($5,000-$75,000)

- British Columbia Gaming Grants: Support for startup costs

- Alberta Community Initiatives Program: Capacity building funding

- Quebec community support programs: Various provincial initiatives

Other Funding Sources:

- Community foundations: Often provide $1,000-$5,000 capacity-building grants

- United Way agencies: Support for new community organizations

- Corporate foundation programs: Many corporations fund nonprofit startup costs

- Crowdfunding: Some organizations successfully crowdfund registration costs from supporters

Important: Most grants require either existing charity status or fiscal sponsorship, so explore fiscal sponsorship first to access grant funding.

How much does it cost to maintain charity status annually in Canada?

After registration, expect ongoing annual costs of $2,500 to $10,000+ depending on your charity’s size and complexity:

Minimum Annual Costs (Small Charity):

- T3010 filing: $1,000

- Accounting/financial statements: $1,000

- Liability insurance: $700

- Bank fees: $200-$500

- Total minimum: ~$2,900

Mid-Size Charity Annual Costs:

- T3010 filing: $1,500

- Accounting/audit: $3,000-$5,000

- Insurance: $1,500

- Governance costs: $1,000

- Software/technology: $1,000

- Fundraising (10-15% of funds raised)

- Total: ~$8,000-$12,000+

Large Charity Annual Costs:

- Professional audit: $10,000+

- Full-time bookkeeping staff

- Comprehensive insurance: $3,000-$5,000

- Legal compliance: $2,000-$5,000

- Advanced donor management systems: $3,000+

- Total: $20,000+

What are the costs if CRA audits my charity?

CRA audits or compliance reviews occur for approximately 1 in 10 charities over a five-year period. Costs include:

Legal Representation:

- Initial audit response: $3,000-$5,000

- Comprehensive audit defense: $5,000-$10,000

- Complex compliance issues: $10,000-$25,000+

Accounting Services:

- Document preparation and financial analysis: $1,500-$3,000

- Restating financial statements if required: $2,000-$5,000

Administrative Time:

- Staff time gathering documents and responding to CRA requests (50-200 hours)

Potential Penalties:

- Penalties for non-compliance vary but can include revocation of charitable status in severe cases

Prevention is cheaper: Annual legal compliance reviews ($500-$1,500) and proper bookkeeping significantly reduce audit risk and costs.

Is GST/HST applicable to charity registration services?

Legal services are GST/HST exempt in Canada, meaning:

- Lawyers’ fees for charity registration and legal advice are not subject to GST/HST

- Accounting services for charities are also GST/HST exempt

- Government filing fees (incorporation, etc.) do not include GST/HST

However, some services may include GST/HST:

- Software subscriptions: Subject to GST/HST

- Office supplies: Subject to GST/HST

- Certain consulting services: May be subject to GST/HST depending on the provider’s status

When you receive quotes for charity registration services from lawyers and accountants, the prices quoted are typically final amounts without additional tax.

Contact To Action

Contact us today to schedule your consultation.

Working with Our Firm

In this evolving economic landscape, collaboration with our firm offers clients a strategic advantage. With Cambodia’s reform-driven investment environment and Canada’s expanding footprint in Southeast Asia, our team of experienced consultants and legal advisors provides tailored guidance to help businesses navigate cross-border opportunities. We focus in developing comprehensive legal strategies, structuring international partnerships, and ensuring compliance in emerging markets.

By leveraging our regional insight and international expertise, you benefit from a trusted partner dedicated to helping you capitalize on growth potential in Cambodia and beyond.

At Northfield & Associates are focus in Foreign Direct Investment (FDI), international trade missions, and cross-border legal strategy. Our team of experienced consultants and legal advisors offers tailored guidance and strategic insight to help you navigate the complexities of international partnerships and development opportunities.

Whether you choose to meet in person at one of our offices or connect virtually, we provide flexible and accessible consultation options. During your session, we’ll assess your goals, review key documentation, and guide you through every stage of your FDI or trade mission engagement.

Let us help you take the next step with confidence supported by trusted legal and strategic counsel every step of the way.

Take the First Step Today

If you believe you may be eligible for legal relief or simply need sound legal advice, we’re here to help. Contact us today to book your consultation. Let us provide the clarity, strategy, and peace of mind you need to move forward.

We serve our clients in English, Cambodian, Vietnamese, Mandarin and Cantonese, especially in Asian clients.

- If you or anybody that you know, think that you meet the requirements and wish to receive further information.

- We can help you start the application process and confirm eligibility requirements to participate.

- We Offer Consultations & Meetings by Phone & Virtually. Affordable Fees.

Disclaimer:

The information contained in this article is provided for general information purposes only and does not constitute legal or other professional advice. Readers should seek tailored legal advice in relation to their personal circumstances.

About Northfield

Northfield & Associates International Corporation is a global consulting firm serving private enterprises, public institutions, not-for-profit organizations, and institutional capital providers. Operating across Cambodia, Canada, and global markets, the firm supports capital deployment, regulatory navigation, and enterprise decision-making in complex economic and geopolitical environments. Northfield & Associates delivers customized, execution-focused advisory solutions that drive measurable transformation, strengthen competitiveness, and enhance long-term highest value opportunities. The firm incorporates consulting, legal, regulatory, financial, and risk expertise to enable disciplined capital allocation, strong governance, and operational resilience. Northfield & Associates upholds a culture of applied insight and innovation, supporting clients across digital transformation, growth strategy, and organizational capability building. The firm advises individual, leading global corporations, midsize enterprises, government agencies, and mission-driven organizations through long-term partnerships. Enterprise-wide risk management, professional ethics, and fiduciary standards are embedded across all operations. Northfield & Associates’ diverse, globally unified teams are committed to execution certainty and sustainable, risk-adjusted returns aligned with ESG and stakeholder objectives.

Forward-Looking Information

This news release contains forward-looking information. All statements, other than statements of historic fact, that address activities, events or developments that the Company believes, expects or anticipates will or may occur in the future constitute forward-looking information.

This forward-looking information reflects the current expectations or beliefs of the Company based on information currently available to the Company.

Forward-looking information is subject to a number of risks and uncertainties that may cause the actual results of the Company to differ materially from those discussed in the forward-looking information, and even if such actual results are realized or substantially realized, there can be no assurance that they will have the expected consequences to, or effects on the Company. Factors that could cause actual results or events to differ materially from current expectations include, among other things: the failure to finalize negotiations concerning the increase of the Loan or to close such transaction and the failure of the Company to complete the acquisition of the Company Facility; operating performance of facilities; environmental and safety risks; delays in obtaining or failure to obtain necessary permits and approvals from government authorities; unavailability of plant, equipment or labour; inability to retain key management and personnel; changes to regulations or policies affecting the Company’s activities; and the other risks disclosed under the heading “Risk Factors” and elsewhere in the Company’s amended annual information.

Forward-looking information speaks only as of the date on which it is made and, except as may be required by applicable securities laws, the Company disclaims any intent or obligation to update any forward-looking information, whether as a result of new information, future events or results or otherwise. Although the Company believes that the assumptions inherent in the forward-looking information are reasonable, forward-looking information is not a guarantee of future performance and accordingly undue reliance should not be put on such information due to the inherent uncertainty therein.

Questions?

info@northfied.biz

Within Corporate Newsroom

Media Contact:

media@northfied.biz

Press contact

PR consultants

press@northfied.biz

NOT LEGAL ADVICE. Information made available on this website in any form is for information purposes only. It is not, and should not be taken as, legal advice. You should not rely on, or take or fail to take any action based upon this information. Never disregard professional legal advice or delay in seeking legal advice because of something you have read on this website. Northfield & Associates professionals will be pleased to discuss resolutions to specific legal concerns you may have.