Northfield & Associate International Corporation Announces Intent to Establish Canada–Cambodia Venture Capital and Private Equity Collaboration Involving 50 Canadian Firms

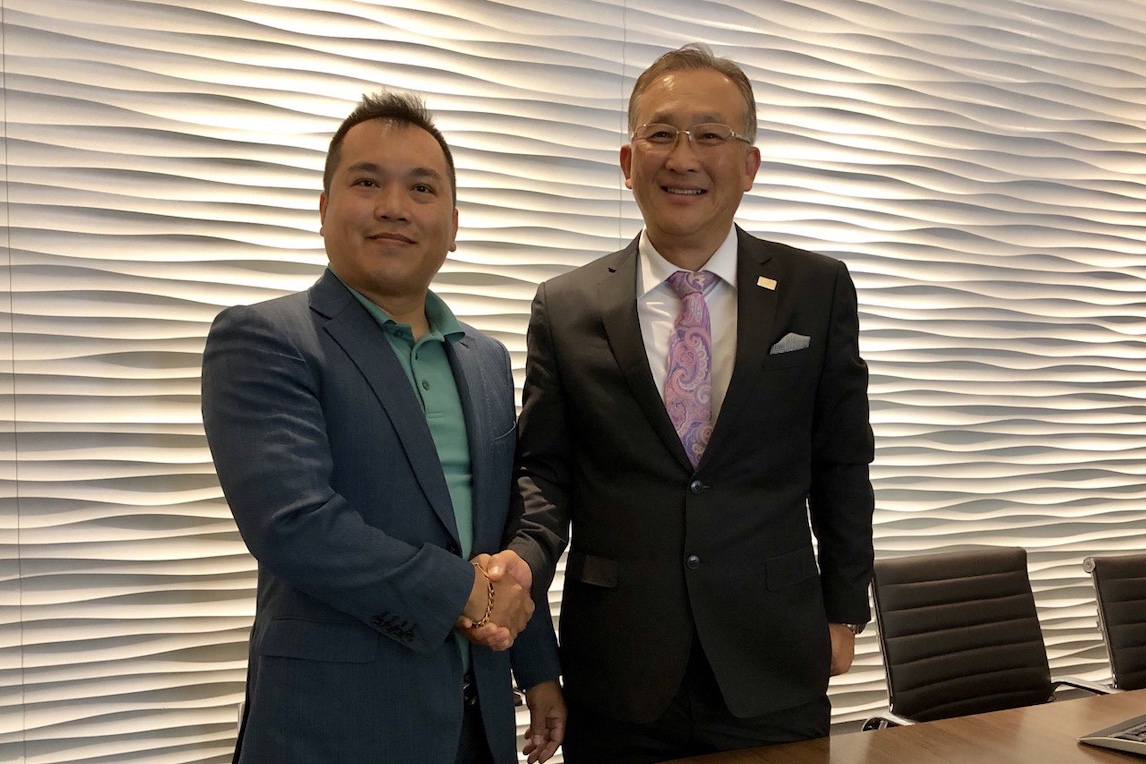

Phnom Penh / Toronto — December 19, 2025 — Mr. Andy Lim, the President of Northfield & Associate International Corporation are pleased to announce on December 19, 2025, the company’s intent to initiate a business collaboration with fifty (50) Canadian venture capital and private equity firms to facilitate bilateral trade and investment opportunities for Cambodian investors.

The proposed collaboration is designed to create an institutional-grade platform enabling compliant capital participation, co-investment, and strategic market access between Canada and Cambodia. The initiative prioritizes governance rigor, risk-adjusted returns, and sector-focused deployment aligned with both jurisdictions’ regulatory frameworks and investment mandates.

Under the contemplated framework, Northfield & Associate International Corporation will coordinate market origination, investor engagement, and cross-border structuring, while the Canadian partner is expected to contribute fund management expertise, due diligence protocols, portfolio construction, and post-investment value creation. Target sectors include advanced manufacturing, agri-business, infrastructure-adjacent services, clean technology, and digital economy enablers, subject to regulatory approvals and final agreements.

“This initiative reflects a disciplined approach to cross-border capital formation grounded in transparency, regulatory compliance, and long-term value creation,” commented by Mr. Andy Lim.

“By aligning Cambodian investor appetite with Canadian private capital expertise, we aim to establish a credible conduit for bilateral trade expansion and sustainable investment.”

The collaboration intends to adhere to applicable securities laws, anti-money laundering and counter-terrorist financing requirements, foreign investment review processes, and tax governance standards in both jurisdictions. Engagement with legal counsel, compliance specialists, and independent advisors will underpin transaction structuring and execution. Next steps include partner selection, definitive documentation, regulatory consultations, and the establishment of an operational governance model. No binding commitments have been executed at this stage.

Phnom Penh / Toronto — 19 décembre 2025 — M. Andy Lim, président de Northfield & Associate International Corporation sont heureux d’annoncer le 19 décembre 2025, l’intention de la société d’entamer une collaboration avec cinquante (50) sociétés canadiennes de capital-risque et de capital-investissement afin de faciliter les échanges commerciaux bilatéraux et les occasions d’investissement pour les investisseurs cambodgiens.

Cette collaboration vise à créer une plateforme institutionnelle permettant une participation au capital conforme à la réglementation, des co-investissements et un accès stratégique aux marchés canadien et cambodgien. L’initiative favorise une gouvernance rigoureuse, des rendements ajustés au risque et un déploiement sectoriel ciblé, conformément aux cadres réglementaires et aux mandats d’investissement des deux juridictions.

Dans le cadre de cette collaboration, Northfield & Associate International Corporation coordonnera les études de marché, la mobilisation des investisseurs et la structuration transfrontalière, tandis que le partenaire canadien apportera son expertise en matière de gestion de fonds, de procédures de vérification préalable, de construction de portefeuille et de création de valeur post-investissement. Les secteurs ciblés comprennent la fabrication de pointe, l’agroalimentaire, les services d’infrastructure, les technologies propres et les catalyseurs de l’économie numérique, sous réserve des approbations réglementaires et des accords définitifs. « Cette initiative témoigne d’une approche rigoureuse en matière de levée de capitaux transfrontalière, fondée sur la transparence, la conformité réglementaire et la création de valeur à long terme », a commenté Andy Lim.

En associant les intérêts des investisseurs cambodgiens à l’expertise canadienne en capital-investissement, nous visons à établir un cadre crédible pour le développement du commerce bilatéral et l’investissement durable.

Cette collaboration vise à se conformer aux lois sur les valeurs mobilières applicables, aux exigences en matière de lutte contre le blanchiment d’argent et le financement du terrorisme, aux processus d’examen des investissements étrangers et aux normes de gouvernance fiscale dans les deux juridictions. Des conseillers juridiques, des spécialistes de la conformité et des conseillers indépendants seront mandatés pour guider et exécuter la transaction. Les prochaines étapes comprennent la sélection du partenaire, la finalisation de la documentation, les consultations réglementaires et la mise en place d’un modèle de gouvernance opérationnelle. Aucun engagement ferme n’a été pris à ce stade.

About Northfield

Northfield & Associates is a consulting firm and a trusted advisor on business strategy in Cambodia. We specialize in the key global sectors, including

agribusiness , aviation and automotive, energy, natural resources, financial services, healthcare, infrastructure, real estate and information technology. Industry Solutions, Service Line and Global & Regional Services.

clients get access to in-depth knowledge in key sectors.

legal, financial management, risk assessment, real estate, IT and enablement of organizations strategies. We partners with array of clients to reach new frontiers and cross uncharted organizations territories. We would work across various sectors in both the private and public, including government domain and focus on strategic, operations, organization and change.

Forward-Looking Information:

This news release contains forward-looking information. All statements, other than statements of historic fact, that address activities, events or developments that the Company believes, expects or anticipates will or may occur in the future constitute forward-looking information.

This forward-looking information reflects the current expectations or beliefs of the Company based on information currently available to the Company.

Forward-looking information is subject to a number of risks and uncertainties that may cause the actual results of the Company to differ materially from those discussed in the forward-looking information, and even if such actual results are realized or substantially realized, there can be no assurance that they will have the expected consequences to, or effects on the Company. Factors that could cause actual results or events to differ materially from current expectations include, among other things: the failure to finalize negotiations concerning the increase of the Loan or to close such transaction and the failure of the Company to complete the acquisition of the Company Facility; operating performance of facilities; environmental and safety risks; delays in obtaining or failure to obtain necessary permits and approvals from government authorities; unavailability of plant, equipment or labour; inability to retain key management and personnel; changes to regulations or policies affecting the Company”s activities; and the other risks disclosed under the heading “Risk Factors” and elsewhere in the Company”s amended annual information.

Forward-looking information speaks only as of the date on which it is made and, except as may be required by applicable securities laws, the Company disclaims any intent or obligation to update any forward-looking information, whether as a result of new information, future events or results or otherwise. Although the Company believes that the assumptions inherent in the forward-looking information are reasonable, forward-looking information is not a guarantee of future performance and accordingly undue reliance should not be put on such information due to the inherent uncertainty therein.

3 Steps to Ensure Your Not-for-Profit’s Compliance to ONCA

Navigating the transition to the new Ontario Not-for-Profit Corporations Act (ONCA) regulations can seem overwhelming for not-for-profit organizations. However, breaking it down into manageable steps can streamline the entire process and help ensure your organization complies with the new regulations.

This post will outline three key steps your not-for-profit organization can take to ensure compliance with ONCA.

Step 1: Understand the Changes

The first crucial step in ensuring compliance with ONCA is to thoroughly understand the critical aspects of the new regulations and how they differ from the current laws. ONCA introduces new rules for membership, governance, and financial reporting. This understanding is not just important, it’s essential as these changes will directly impact your organization’s bylaws, Letters Patent, and other governing documents. To start, delve into the ONCA requirements, consult legal experts, and gather information on how the changes will affect your organization.

Step 2: Review and Update Documents

The next proactive step is to meticulously examine your organization’s bylaws, Letters, Patents, and other governing documents to ensure they align with ONCA requirements. This includes ensuring that your organization’s purpose, membership, governance structure, and decision-making processes comply with ONCA regulations. Review your organization’s governing documents to ensure compliance and identify any areas that require updating. This could include updating your organization’s bylaws to include provisions for electronic voting or updating your Letters Patent to reflect changes in your organization’s name or structure.

Step 3: Educate Your Team

Lastly, it’s of utmost importance to ensure that everyone in your organization, from the board members to the staff, is fully aware of the changes and how they will impact their roles and responsibilities. This includes comprehensive training on the new regulations, updating job descriptions, and communicating any changes to your organization’s policies and procedures. To educate your team, organize training sessions or workshops to ensure everyone is up to date on the new regulations. You can also provide resources such as guides or FAQ documents to help your team navigate the changes.

Following these three steps, your not-for-profit organization can smoothly transition to the new regulations under ONCA, ensuring legal compliance and operational efficiency. It is crucial to begin the process as soon as possible to allow ample time to make necessary changes before the new regulations occur.

Remember, compliance with ONCA is essential for your organization’s success, and taking the necessary steps now can save you time and money in the long run.

Overview of ONCA Compliance for Ontario Not-for-Profit Corporations

Transitioning to the Ontario Not-for-Profit Corporations Act (ONCA) requires careful attention to several core areas of our organization’s governance and operations.

The updated legislation changes how we manage bylaws, membership, and reporting. Our governing documents such as Articles of Incorporation and by-laws may need substantial revision.

Key areas to focus on include:

Membership and Voting Rights: ONCA introduces new rules about membership classes and members’ rights.

These updates include provisions for absentee voting and clearer processes for member participation in meetings and proposals.

Governance and Director Roles: The act clarifies directors’ duties and outlines options for indemnification.

Our leadership must understand these changes to maintain proper oversight.

Financial Accountability: ONCA sets new requirements for financial reporting.

It extends transparency expectations to all not-for-profit corporations, not just public charities under the Canada Revenue Agency.

Document Review and Updates: We must review and update our governing documents—including Letters of Patent and articles of amendment.

Legal advice can help ensure accuracy.

Incorporation and Registry Compliance: The Ontario Business Registry manages filings related to ONCA.

We need to keep up with incorporation documents and ongoing compliance requirements.

Education and Transition Planning: We must educate our team about the new regulations.

Resources like the Not-for-Profit Incorporator’s Handbook and support from groups such as Community Legal Education Ontario can help.

Important deadlines: Ontario not-for-profit corporations had until October 18, 2024, to update their structures under ONCA.

Although the transition deadline has passed, many organizations continue to refine their policies to meet ONCA standards.

ONCA Compliance Areas

What to Review or Update

Key Points

Membership Structure

Membership classes, voting rights

Absentee voting, members’ meeting rules

Governance

Directors’ duties, indemnification

Clear responsibilities, board training

Governing Documents

By-laws, Letters of Patent, articles of amendment

Legal review, alignment with ONCA

Financial Reporting

Audit requirements, transparency standards

Compliance with CRA and ONCA

Incorporation and Filing

Ontario Business Registry submissions

Timely updates and filings

Team Education & Training

Workshops, guides, policy updates

Communication across board and staff

By focusing on these points, we help our organization operate effectively under ONCA’s modernized framework.

Careful planning and active participation from everyone are vital to maintain compliance and support our mandate as a public benefit corporation in Ontario.

Conclusion

Navigating ONCA compliance doesn’t have to be overwhelming when you have the right legal guidance. The transition to Ontario’s modernized not-for-profit framework requires careful attention to governance structures, membership rights, financial reporting, and document updates. While the October 2024 deadline has passed, many organizations are still working to fully align their operations with ONCA standards, making expert legal support more crucial than ever.

At B.I.G. Charity Law Group, we specialize in helping Ontario not-for-profit corporations achieve and maintain ONCA compliance. Our experienced team understands the complexities of transitioning governance documents, updating bylaws, and ensuring your organization meets both provincial and federal requirements. Whether you need assistance with membership structure revisions, director duty clarification, or financial reporting compliance, we provide practical solutions tailored to your organization’s unique needs.

Ready to ensure your not-for-profit is fully ONCA compliant?

Contact us at Northfield & Associates today to take the first step toward confident ONCA compliance and effective governance for your organization.

How Can We Make Sure Our Business Meets Both Local and Federal Rules?

To stay compliant, we must:

Know which rules apply at both local and federal levels.

Keep all registrations and licenses current.

Review changes in laws that affect us.

Train our team on compliance requirements.

Document our compliance efforts for future reference.

What Is Ontario’s Not-for-Profit Corporations Act, 2010 (ONCA)?

ONCA is a law that sets out how non-profit groups in Ontario should form and operate.

It replaced older rules to help non-profits run more smoothly. The Act covers governance, member rights, and reporting duties.

Organizations must update their rules to match ONCA to stay legally compliant.

What Rules Govern Not-for-Profit Organisations?

Not-for-profits must follow rules about:

How they are formed and managed.

How meetings and votes take place.

Keeping financial records and reporting.

Protecting members’ rights.

Filing documents with the government.

Following these rules helps groups stay transparent and accountable.

How Do We Confirm We Are Following All Applicable Laws?

We confirm compliance by:

Checking that our policies align with laws.

Reviewing and updating governing documents.

Conducting internal audits or reviews.

Seeking legal advice when unsure.

Keeping clear records of decisions and actions.

How Do We Stay Compliant with Financial Rules?

To comply with financial regulations, we:

Keep accurate and up-to-date financial records.

Follow proper budgeting and spending procedures.

Prepare and file required financial reports.

Have controls in place to prevent misuse of funds.

Conduct regular financial audits or reviews.

How Do We Ensure We Follow Our Own Policies and Procedures?

To follow our policies, we:

Communicate policies clearly to everyone.

Provide training and resources so everyone understands expectations.

Monitor activities to quickly spot issues.

Address breaches promptly and fairly.

Review and update policies regularly.

Disclaimer: The information contained in this article is provided for general information purposes only and does not constitute legal or other professional advice. Readers should seek tailored legal advice in relation to their personal circumstances.

At Northfield & Associates our expert teams guidance on compliance requirements. Our team understands Canadian law and can help ensure your organization follows proper procedures.

To discuss your specific circumstances and receive expert assistance throughout the reinstatement process with our experienced legal team.

READY FOR BETTER NONPROFIT REPORTING?

At Northfield & Associates, we have a team of professional bookkeepers and accountants to help your organization manage the books so that you can breeze through tax season.

We’re often asked by prospective clients what our Bookkeeping service. People want to know what specific tasks we do, and what their responsibility is. This brief explainer page will answer that question. This is by no means an exhaustive list, but covers the most frequently asked questions.

Getting Started

Review your existing books for needed corrections or back-work

Chart of accounts setup or amendment

Assistance with setting up bank feeds

Limited assistance* with setting up payroll (QBO or Gusto only)

Your books brought current and reconciled if needed

Ongoing Monthly Bookkeeping

After-the-fact transaction recording

Post to general ledger

Post to other ledgers (as needed)

Bank account reconciliation

Monthly financial statements

Other bookkeeping services, as required

Best-practice bookkeeping advice and counsel

Year End

Assistance with 1099-NEC preparation*

Assistance with 1099-MISC preparation*

Year-end financial statements and period-end closing

What We Don’t Do

Pay bills

We do not offer bill-pay services at this time, nor do we manage Accounts Payable (AP) or Accounts Receivable (AR).

Payroll tax responsibility

Our bookkeepers can assist you in setting up your initial payroll service in QBO or Gusto. We are not responsible for entering payroll hours/salary, accruing payroll taxes, nor the transmittal of payroll taxes to the IRS or the state. Your full-service payroll provider (QBO, Gusto, or whatever other service a client uses) will be the responsible party for payroll and payroll tax compliance.

*Payroll deductions and benefits

We provide assistance with setting up a payroll account in either Quickbooks Online or Gusto, including entry of employee data. We do not assist in state registrations, benefits, or advise on deductions. Those service areas are provided directly by either QBO or Gusto.

Preparation of W2s

Similar to the last item, your full-service payroll provider (QBO/Gusto) is responsible for preparation of Form W2 for employees.

Sales tax reporting

For those nonprofits that sell taxable goods and/or services, your bookkeeper will assist in accounting for sales taxes collected and transmitted, but we do not prepare state sales tax reports.

Donation recording

We do not provide individual donation data entry into your neither your donor CRM nor Quickbooks Online, nor do we prepare year-end donor acknowledgements.

Administrative tasks

We cannot provide administrative services unrelated to our bookkeeping function.

Attend board meetings

Due to the constraints of time and distance, we are unable to be present, physically nor virtually, at a meeting of a client’s board of directors.*May incur additional fee per 1099-NEC or 1099-MISC.

Let’s Collaborate & Make a Difference!

Partner with us to amplify your mission. Whether it’s Charity accounting, financial transparency, or strategic growth—we’re here to help you create meaningful impact. Let’s work together to build a better future!

In this evolving economic landscape, collaboration with our firm offers clients a strategic advantage. With Cambodia’s reform-driven investment environment and Canada’s expanding footprint in Southeast Asia, our team of experienced consultants and legal advisors provides tailored guidance to help businesses navigate cross-border opportunities. We focus in developing comprehensive legal strategies, structuring international partnerships, and ensuring compliance in emerging markets.

By leveraging our regional insight and international expertise, you benefit from a trusted partner dedicated to helping you capitalize on growth potential in Cambodia and beyond.

Book a Consultation with Northfield & Associates

Your Trusted Partner in International Bilateral Relations

At Northfield & Associates are focus in Foreign Direct Investment (FDI), international trade missions, and cross-border legal strategy. Our team of experienced consultants and legal advisors offers tailored guidance and strategic insight to help you navigate the complexities of international partnerships and development opportunities.

Whether you choose to meet in person at one of our offices or connect virtually, we provide flexible and accessible consultation options. During your session, we’ll assess your goals, review key documentation, and guide you through every stage of your FDI or trade mission engagement.

Let us help you take the next step with confidence supported by trusted legal and strategic counsel every step of the way.

If you believe you may be eligible for legal relief or simply need sound legal advice, we’re here to help. Contact us today to book your free consultation. Let us provide the clarity, strategy, and peace of mind you need to move forward.

We serve our clients in English, Cambodian, Vietnamese, Mandarin and Cantonese, especially in Asian clients.

If you or anybody that you know, think that you meet the requirements and wish to receive further information.

We can help you start the application process and confirm eligibility requirements to participate.

We Offer Consultations & Meetings by Phone & Virtually. Affordable Fees.

BOOK A CONSULTATION TODAY

Contact Northfield & Associates today to schedule a consultation with an experienced Consultant.

Northfield & Associates is a Canadian consulting firm based in Toronto, Canada. Northfield & Associates specializes in all types of immigration matters, from spousal sponsorships to refugee board appeals. With over eight (8) years of experience and an excellent success rate, Northfield & Associates is recognized as one of Canada’s premier immigration consulting firm.

The purpose of the Free Assessment is to assess whether you are qualified to apply for permanent residence in Canada under the Family Sponsorship, Skilled Worker, or Business Class categories. Please choose which category you would like to be assessed under and complete all fields in the form. We will endeavor to complete your assessment and provide you with a reply within one business day. There is no charge for this service. All information provided will be kept strictly confidential. If our assessment indicates that you are qualified for immigration to Canada, we will contact you to provide further information about our services and fees. Start Your Immigration Application!

Northfield & Associates International Corporation is a global consulting firm serving private enterprises, public institutions, not-for-profit organizations, and institutional capital providers. Operating across Cambodia, Canada, and global markets, the firm supports capital deployment, regulatory navigation, and enterprise decision-making in complex economic and geopolitical environments. Northfield & Associates delivers customized, execution-focused advisory solutions that drive measurable transformation, strengthen competitiveness, and enhance long-term highest value opportunities. The firm incorporates consulting, legal, regulatory, financial, and risk expertise to enable disciplined capital allocation, strong governance, and operational resilience. Northfield & Associates upholds a culture of applied insight and innovation, supporting clients across digital transformation, growth strategy, and organizational capability building. The firm advises individual, leading global corporations, midsize enterprises, government agencies, and mission-driven organizations through long-term partnerships. Enterprise-wide risk management, professional ethics, and fiduciary standards are embedded across all operations. Northfield & Associates’ diverse, globally unified teams are committed to execution certainty and sustainable, risk-adjusted returns aligned with ESG and stakeholder objectives.

NORTHFIELD & ASSOCIATES in Canada

As a global consulting firm, Northfield & Associates helps clients with total transformation, driving complex change, enabling organizations to grow, and driving bottom-line impact.

Learn about our offices in Canada, read our latest thought leadership, and connect with our team.

This news release contains forward-looking information. All statements, other than statements of historic fact, that address activities, events or developments that the Company believes, expects or anticipates will or may occur in the future constitute forward-looking information.

This forward-looking information reflects the current expectations or beliefs of the Company based on information currently available to the Company.

Forward-looking information is subject to a number of risks and uncertainties that may cause the actual results of the Company to differ materially from those discussed in the forward-looking information, and even if such actual results are realized or substantially realized, there can be no assurance that they will have the expected consequences to, or effects on the Company. Factors that could cause actual results or events to differ materially from current expectations include, among other things: the failure to finalize negotiations concerning the increase of the Loan or to close such transaction and the failure of the Company to complete the acquisition of the Company Facility; operating performance of facilities; environmental and safety risks; delays in obtaining or failure to obtain necessary permits and approvals from government authorities; unavailability of plant, equipment or labour; inability to retain key management and personnel; changes to regulations or policies affecting the Company’s activities; and the other risks disclosed under the heading “Risk Factors” and elsewhere in the Company’s amended annual information.

Forward-looking information speaks only as of the date on which it is made and, except as may be required by applicable securities laws, the Company disclaims any intent or obligation to update any forward-looking information, whether as a result of new information, future events or results or otherwise. Although the Company believes that the assumptions inherent in the forward-looking information are reasonable, forward-looking information is not a guarantee of future performance and accordingly undue reliance should not be put on such information due to the inherent uncertainty therein.

Questions?

info@northfied.biz

Within Corporate Newsroom

Media Contact:

media@northfied.biz

Press contact

PR Secretary press@northfied.biz

NOT LEGAL ADVICE. Information made available on this website in any form is for information purposes only. It is not, and should not be taken as, legal advice. You should not rely on, or take or fail to take any action based upon this information. Never disregard professional legal advice or delay in seeking legal advice because of something you have read on this website. Northfield & Associates professionals will be pleased to discuss resolutions to specific legal concerns you may have.

How to Register a Church in Canada: Step-by-Step Guide

Starting a church in Canada involves more than gathering a congregation and holding services. To operate legally and access benefits such as tax exemptions and issuing tax receipts to donors, your church needs proper registration. But how do you register a church in Canada, and is it considered a charity? This guide will walk you through the steps to establish and register a church in compliance with Canadian laws.

Church Registration in Canada: Quick Overview

Before diving into the details, here’s what you need to know at a glance:

Timeline: 3-12 months total (2-4 weeks for provincial incorporation, 4-6 weeks for federal incorporation, 6-12 months for CRA charitable status approval)

Total Costs: $200-$2,500

Provincial incorporation: $200-$350

Federal incorporation: $200-$250

CRA charitable registration: Free

Legal fees (optional): $1,500-$5,000

Basic Requirements:

Minimum 3 directors

Governing documents (articles and bylaws)

Religious purposes that benefit the public

Proper organizational structure

Key Benefits:

Legal entity status and limited liability protection

Tax-exempt status

Ability to issue donation receipts

Enhanced credibility and public trust

What Is Church Registration in Canada?

Churches in Canada generally fall under the category of nonprofit organizations. Many churches also apply for charitable status with the Canada Revenue Agency (CRA) to receive tax-exempt benefits and issue donation receipts. However, registering a church requires meeting specific legal requirements.

A church can be incorporated as a nonprofit religious corporation under the Ontario Not-for-Profit Corporations Act (ONCA) for those in Ontario or the Canada Not-for-Profit Corporations Act (CNCA) for those operating across multiple provinces. This incorporation provides the church with legal recognition, limited liability protection, and a formal governance structure.

Step 1: Define the Purpose and Structure of the Church

Before registering, it’s essential to determine:

The church’s mission, beliefs, and statement of faith

Leadership structure (e.g., pastors, elders, board of directors)

If your church primarily operates in Ontario, you can incorporate under ONCA by filing:

Articles of Incorporation (Form 2)

A NUANS name search report (if applicable)

A cover letter and government fee

For other provinces, similar processes exist under respective provincial nonprofit legislation.

Option 2: Federal Incorporation

If your church will operate across multiple provinces, federal incorporation under CNCA may be better. You’ll need to file:

Articles of Incorporation

A NUANS name search report

Bylaws and governance structure

Once incorporated, your church exists as a legal entity.

Other Provincial Options

British Columbia: Incorporate under the BC Societies Act through BC Registry Services. Cost: approximately $100-$150. Processing time: 1-2 weeks.

Alberta: Use the Alberta Societies Act through Alberta Corporate Registry. Cost: approximately $100. Processing time: 1-2 weeks.

Saskatchewan: Register under the Saskatchewan Non-profit Corporations Act. Cost: approximately $125-$200. Processing time: 2-3 weeks.

Manitoba: Incorporate under The Corporations Act through Companies Office. Cost: approximately $330. Processing time: 2-4 weeks.

Quebec: Quebec has unique requirements under Part III of the Companies Act. Churches may incorporate as legal persons or register under the Civil Code. It’s highly recommended to consult a Quebec charity lawyer due to the province’s distinct legal system. Cost: approximately $200-$400. Processing time: 4-6 weeks.

Maritime Provinces: Each has its own societies or nonprofit corporations legislation with similar processes to other provinces.

Note: Processing times are approximate and can vary based on government workload and application completeness.

Step 4: Apply for a Business Number (BN) and CRA Registration

After incorporation, your church needs a Business Number (BN) from the CRA for tax-related matters. You can apply online through the CRA’s Business Registration system.

Step 5: Apply for Charitable Status (Optional but Recommended)

Not all churches automatically qualify as charities. However, obtaining charitable status allows the church to issue donation receipts and receive tax-exempt status. To apply:

Submit governing documents (e.g., articles of incorporation, bylaws)

Demonstrate the church’s charitable purposes (e.g., advancing religion, providing community services)

The CRA reviews applications to ensure the organization meets the requirements for religious charities.

What Qualifies as “Advancement of Religion” for the CRA?

To receive charitable registration, your church must demonstrate that it advances religion in a way that benefits the public. Here’s what the CRA looks for:

Activities That Qualify:

Regular Worship Services:

Scheduled religious services open to the community

Prayer meetings and religious observances

Celebration of religious holidays and sacraments

Religious Education:

Sunday school or religious education programs

Bible studies and scripture classes

Training programs for religious leaders

Youth programs with religious instruction

Community Outreach:

Missionary work aligned with religious beliefs

Community support programs rooted in religious doctrine

Pastoral care and counselling

Religious publications and media

Maintenance of Places of Worship:

Operating churches, temples, or houses of worship

Providing space for religious ceremonies

Maintaining religious artifacts and symbols

What the CRA Examines:

Public Benefit:

Activities must be available to a significant segment of the public

Cannot be limited to a private group or family

Must demonstrate community benefit

Religious Doctrine:

Clear statement of faith and beliefs

Recognized religious practices

Genuine religious purpose (not primarily social or recreational)

Operational Structure:

Regular religious services and activities

Trained or ordained religious leaders

Formal membership or congregation

Financial Accountability:

At least 80% of resources directed to charitable activities

Proper donation receipting procedures

Transparent financial reporting

Red Flags the CRA Watches For:

Private benefit to founders or directors

Primarily social or cultural activities without religious component

Unclear or constantly changing religious doctrine

Limited public access to activities

Mixing political advocacy with religious activities

Excessive fundraising with minimal religious programming

Pro Tip: When completing Application to Register a Charity, provide specific examples of your religious activities, worship schedules, and how you’ll benefit the public. Vague descriptions like “spreading faith” are insufficient – the CRA wants concrete details about what your church will actually do.

Step 6: Register for Tax Exemptions and Other Benefits

Once approved as a charity, your church can apply for:

Property tax exemptions (varies by municipality)

HST/GST rebates

Payroll deductions for clergy housing allowances

Maintaining tax-exempt status requires compliance with CRA regulations, such as annual reporting and proper financial management.

Annual Compliance Requirements for Registered Churches

After receiving charitable registration, your church has ongoing obligations to maintain its status. Failing to meet these requirements can result in penalties, loss of charitable status, or even legal consequences.

Annual Filing Requirements:

T3010 Registered Charity Information Return:

Must be filed within 6 months of your fiscal year-end

Reports all revenue, expenses, and activities

Publicly available on CRA website

Filing fee: $0

Deadline is strict – late filing results in $500 penalty and possible revocation

Provincial/Federal Annual Returns:

Ontario corporations: Annual return required (currently no fee under ONCA)

Federal corporations: Annual return required ($0-$40 fee)

Update any changes to directors, registered office address

Due dates vary by incorporation jurisdiction

Financial Requirements:

Minimum Spending on Charitable Activities:

Must spend at least 80% of donated funds on religious/charitable activities

Maximum 10% on administration

Maximum 10% on fundraising

These are guidelines; actual spending must be reasonable

Record Keeping (Minimum 7 Years):

All donation receipts and donor records

Financial statements and bank records

Minutes of board meetings

Contracts and agreements

Correspondence with CRA

Property and asset records

Donation Receipts:

Must follow CRA guidelines exactly

Include mandatory information: charity name, registration number, date, amount, donor name

Only issue receipts for eligible donations

Keep copies of all issued receipts

Governance Requirements:

Board Meetings:

Hold regular board meetings (at least annually, ideally quarterly)

Keep detailed minutes

Ensure quorum requirements are met

Document all major decisions

Member Meetings:

Hold annual general meetings if you have members

Provide financial reports to members

Hold director elections as per bylaws

Director Obligations:

Maintain minimum number of directors (usually 3)

Ensure directors are not disqualified (not bankrupt, not convicted of fraud)

Directors must act in the church’s best interests

Update CRA within 30 days of director changes

Operational Requirements:

Stay Within Charitable Purposes:

Activities must align with registered purposes

Cannot change purposes without CRA approval

Cannot engage in prohibited political activities

Limited business activities (must be related to religious purposes)

Avoid Private Benefit:

No distribution of income to members or directors

Compensation must be reasonable for services rendered

Arms-length transactions required

No personal use of church assets

Political Activities (Limited):

Can devote up to 10% of resources to political activities

Must be non-partisan

Must relate to your charitable purposes

Cannot support or oppose political parties or candidates directly

Public Transparency:

Information Available on CRA Website:

T3010 returns (publicly searchable)

Charity registration details

Contact information

Financial summaries

Your Responsibilities:

Keep public informed about activities

Respond to reasonable information requests

Maintain up-to-date contact information with CRA

Consequences of Non-Compliance:

Minor Issues:

Written warnings from CRA

Education letters

Compliance agreements

Serious Issues:

$500-$5,000 penalties

Suspension of donation receipting privileges

Compliance audits

Severe Issues:

Revocation of charitable status

Public disclosure of non-compliance

Legal action for misuse of charitable funds

Pro Tip: Many churches hire a bookkeeper or accountant familiar with charity requirements to ensure compliance. The small cost prevents major problems down the road.

Are Churches Considered Nonprofits or Charities in Canada?

Churches in Canada are generallynonprofits, but not all qualify as registered charities. A nonprofit church can operate legally but won’t receive charitable tax benefits unless it registers with the CRA. To be recognized as a charity, a church must prove its activities advance religion and benefit the public.

How Much Does It Cost to Register a Church in Canada?

The costs vary depending on the registration process:

NUANS name search: $15–$35

Provincial incorporation: $155 (Ontario government fee, other provinces may vary)

Federal incorporation: $200 (Corporations Canada fee)

While DIY registration is possible, hiring an experienced charity lawyer ensures compliance, provides for ideal membership structure, and increases approval chances.

How Long Does It Take to Register a Church in Canada?

Federal incorporation: 1–3 days

Charity registration: 5–12 months (depending on CRA review and how well the application is drafted)

Planning ahead helps avoid delays and ensures smooth registration.

Common Mistakes When Registering a Church in Canada (And How to Avoid Them)

Learning from others’ mistakes can save you time, money, and frustration. Here are the most common errors churches make during registration:

1. Not Having Proper Bylaws Before Incorporating

The Mistake: Rushing to incorporate with generic or incomplete bylaws copied from the internet.

Why It’s a Problem:

CRA will scrutinize your bylaws during charitable registration

Poorly drafted bylaws cause delays or rejection

Bylaws are hard to change once incorporated

How to Avoid It: Have a lawyer draft or review your bylaws before incorporation. Ensure they include mandatory dissolution clauses and comply with CRA requirements.

2. Insufficient Board Members

The Mistake: Starting with only 1-2 directors to keep things simple.

Why It’s a Problem:

Most provinces require minimum 3 directors

CRA looks unfavorably on very small boards

Creates succession problems if a director leaves

How to Avoid It: Start with at least 3-5 qualified directors who understand their fiduciary duties and are committed to the church’s mission.

3. Mixing Personal and Church Finances

The Mistake: Using personal bank accounts for church income and expenses, especially in the early stages.

Why It’s a Problem:

Violates nonprofit and charity rules

Creates personal tax liability

CRA will deny or revoke charitable status

Exposes personal assets to church liabilities

How to Avoid It: Open a dedicated church bank account immediately after incorporation. Never deposit church funds into personal accounts.

4. Not Keeping Proper Donation Records

The Mistake: Informal tracking of donations, issuing receipts before charitable registration, or missing mandatory receipt information.

Why It’s a Problem:

Cannot prove financial accountability to CRA

Donors lose tax credits if receipts are improper

Penalty of 5% of receipted amount for each incorrect receipt

Can lead to loss of charitable status

How to Avoid It:

Only issue official donation receipts after receiving charitable registration

Use CRA-approved receipt formats

Keep detailed donor records for 7 years

Consider donor management software

5. Failing to File Annual Returns on Time

The Mistake: Missing the T3010 filing deadline or forgetting provincial annual returns.

Why It’s a Problem:

Automatic $500 penalty for late T3010

Can lead to revocation of charitable status after 1 year

Provincial penalties for late corporate returns

Creates compliance record with CRA

How to Avoid It:

Mark filing deadlines on calendar (6 months after fiscal year-end)

Consider hiring an accountant for T3010 preparation

File even if you had no activity

Set up CRA online account for reminders

6. Not Understanding the 80/10/10 Rule

The Mistake: Spending too much on administration or fundraising relative to actual charitable activities.

Why It’s a Problem:

CRA expects approximately 80% of resources on religious/charitable activities

Excessive overhead raises red flags

Can lead to CRA investigation or status loss

How to Avoid It:

Budget carefully to prioritize religious programming

Track expenses by category (charitable activities, administration, fundraising)

Keep administration and fundraising each under 20% of total spending

Document that spending is reasonable for your church’s size and activities

7. Copying Another Church’s Documents Without Customization

The Mistake: Using another church’s articles, bylaws, or Application to Register a Charity as a template without proper adaptation.

Why It’s a Problem:

Each church has unique circumstances and needs

Generic documents often contain errors or irrelevant clauses

CRA notices boilerplate applications and scrutinizes them more carefully

May not comply with your specific provincial requirements

How to Avoid It: Use templates as a starting point only. Customize all documents to reflect your church’s actual structure, beliefs, and plans. Have a lawyer review before filing.

8. Unclear or Overly Broad Purpose Statements

The Mistake: Writing vague purposes like “to help people” or overly broad purposes that include non-charitable activities.

Why It’s a Problem:

CRA requires specific charitable purposes

Vague purposes invite CRA questions and delays

Broad purposes may include non-charitable elements that disqualify you

How to Avoid It: Be specific about your religious purposes. Use language like “to advance the Christian faith through worship, religious education, and community ministry” rather than “to help the community.”

9. Starting Operations Before Proper Registration

The Mistake: Holding services, collecting donations, and issuing receipts before completing incorporation and charitable registration.

Why It’s a Problem:

Operating without incorporation removes liability protection

Cannot legally issue donation receipts without charitable registration

Donors cannot claim tax credits

May create personal tax liability

How to Avoid It:

Complete incorporation before commencing formal operations

Wait for charitable registration before issuing donation receipts

You can hold informal gatherings, but don’t collect significant funds until properly registered

10. Ignoring Provincial Requirements When Federally Incorporated

The Mistake: Thinking federal incorporation means you don’t need to register in provinces where you operate.

Why It’s a Problem:

May still need to register for provincial sales tax

Need to register for provincial payroll accounts if hiring staff

May need extra-provincial registration for certain activities

How to Avoid It: Research specific requirements in each province where you’ll operate, even with federal incorporation.

What If My Church’s Charitable Application Is Denied?

Not all church applications for charitable status are approved on the first try. Here’s what you need to know if you receive a denial:

Common Reasons for CRA Denial:

Insufficient Public Benefit:

Activities appear to benefit a private group rather than the broader public

Limited access to services or membership

Family-run organization with insufficient community involvement

Insufficient demonstration of financial accountability

No clear plan for sustainability

Governance Concerns:

Inadequate bylaws or articles

Board members who don’t meet CRA requirements

Conflicts of interest not properly addressed

Documentation Issues:

Incomplete Application to Register a Charity

Missing required supporting documents

Inconsistencies between different documents

What Happens After a Denial?

CRA Notification:

You’ll receive a detailed letter explaining the reasons for denial

Letter will specify what requirements weren’t met

You have 90 days to respond or appeal

Your Options:

Option 1: Provide Additional Information (Within 90 Days)

Submit clarifying documents

Explain misunderstandings

Provide evidence you meet requirements

CRA will reconsider based on new information

Option 2: Revise and Reapply (After Addressing Issues)

Fix the problems identified in the denial letter

Revise governing documents if needed

Submit a new application

No waiting period required if you address the issues properly

Option 3: File an Objection (Within 90 Days)

Formal appeal process if you believe the denial was incorrect

Must provide detailed reasons why you disagree

CRA Appeals Division will review

Can take 6-12 months for resolution

Option 4: Operate as Nonprofit Without Charitable Status

Continue operating as an incorporated nonprofit

Cannot issue donation receipts

No tax-exempt status

Can reapply for charitable status in the future

Tips for Successful Reapplication:

Address Every Issue:

Carefully read the denial letter

Fix each specific problem mentioned

Don’t just resubmit the same application

Strengthen Your Application:

Provide more detailed activity descriptions

Include concrete examples of how you’ll benefit the public

Show evidence of community need

Demonstrate financial viability

Seek Professional Help:

Consider hiring a charity lawyer for reapplication

Lawyers familiar with CRA requirements can significantly improve approval chances

Investment in legal help often saves time and future problems

Document Everything:

Keep copies of all correspondence with CRA

Maintain records of how you addressed each concern

Show progress on implementing required changes

How Long Until You Can Reapply?

Good news: There’s no mandatory waiting period. You can reapply as soon as you’ve addressed the issues that caused the denial. However:

Take time to properly fix the problems

Don’t rush a reapplication with the same flaws

Most successful reapplications happen 2-6 months after denial

Operating Without Charitable Status:

If you decide not to reapply or need time to build your church before trying again:

You Can:

Operate legally as an incorporated nonprofit

Hold religious services and activities

Accept donations (but cannot issue tax receipts)

Build a track record of activities

Reapply for charitable status later when better positioned

Benefits of Waiting:

Demonstrate established operations and community benefit

Build financial history and stability

Refine governance structure

Develop clear track record for CRA

Many churches successfully operate for 1-2 years as nonprofits before applying for charitable status, which can actually strengthen their applications.

Final Thoughts: Should You Register Your Church as a Charity?

Registering a church as a nonprofit provides legal protection and structure, while obtaining charitable status offers tax benefits and donation advantages. If your church relies on donations, charitable registration is highly recommended.

Have more questions about registering your Canadian temple or church?

At Northfield & Associates our expert teams guidance on compliance requirements. Our team understands Canadian charity law and can help ensure your organisation follows proper procedures.

How long does it take to register a church in Canada?

The complete process takes 3-12 months total. Incorporation takes 2-6 weeks, while CRA charitable registration takes 6-12 months. You can operate as a nonprofit immediately after incorporation, but must wait for charitable registration before issuing donation receipts.

Can I start a church without incorporation?

Yes, but it’s not recommended. Without incorporation, you have no liability protection, cannot apply for charitable status, cannot own property in the church’s name, and have less credibility with donors. Most churches incorporate immediately for legal protection.

Do I need a physical location to register a church in Canada?

No, you don’t need a church building. Many churches start by meeting in homes or renting community spaces. You only need a registered office address (can be a home address) and evidence of regular religious activities.

How many members do I need to start a church in Canada?

There’s no minimum number of members, but you need at least 3 directors for your board. For charitable registration, most churches have at least 15-25 regular participants to demonstrate public benefit rather than being a private family group.

What’s the difference between registered and unregistered churches in Canada?

An unregistered church has no legal status or liability protection and cannot issue donation receipts. A registered nonprofit church has legal protection but still cannot issue receipts. A registered charity church can issue donation receipts, receives tax-exempt status, but must meet CRA compliance requirements.

Ready for better nonprofit reporting?

At Northfield & Associates, we have a team of professional bookkeepers and accountants to help your organization manage the books so that you can breeze through tax season.

We’re often asked by prospective clients what our Bookkeeping Service covers? People want to know what specific tasks we do, and what their responsibility is. This brief explainer page will answer that question. This is by no means an exhaustive list, but covers the most frequently asked questions.

Getting Started

Review your existing books for needed corrections or back-work

Chart of accounts setup or amendment

Assistance with setting up bank feeds

Limited assistance* with setting up payroll (QBO or Gusto only)

Your books brought current and reconciled if needed

Ongoing Monthly Bookkeeping

After-the-fact transaction recording

Post to general ledger

Post to other ledgers (as needed)

Bank account reconciliation

Monthly financial statements

Other bookkeeping services, as required

Best-practice bookkeeping advice and counsel

Year End

Assistance with 1099-NEC preparation*

Assistance with 1099-MISC preparation*

Year-end financial statements and period-end closing

What We Don’t Do

Pay bills

We do not offer bill-pay services at this time, nor do we manage Accounts Payable (AP) or Accounts Receivable (AR).

Payroll tax responsibility

Our bookkeepers can assist you in setting up your initial payroll service in QBO or Gusto. We are not responsible for entering payroll hours/salary, accruing payroll taxes, nor the transmittal of payroll taxes to the IRS or the state. Your full-service payroll provider (QBO, Gusto, or whatever other service a client uses) will be the responsible party for payroll and payroll tax compliance.

*Payroll deductions and benefits

We provide assistance with setting up a payroll account in either Quickbooks Online or Gusto, including entry of employee data. We do not assist in state registrations, benefits, or advise on deductions. Those service areas are provided directly by either QBO or Gusto.

Preparation of W2s

Similar to the last item, your full-service payroll provider (QBO/Gusto) is responsible for preparation of Form W2 for employees.

Sales tax reporting

For those nonprofits that sell taxable goods and/or services, your bookkeeper will assist in accounting for sales taxes collected and transmitted, but we do not prepare state sales tax reports.

Donation recording

We do not provide individual donation data entry into your neither your donor CRM nor Quickbooks Online, nor do we prepare year-end donor acknowledgements.

Administrative tasks

We cannot provide administrative services unrelated to our bookkeeping function.

Attend board meetings

Due to the constraints of time and distance, we are unable to be present, physically nor virtually, at a meeting of a client’s board of directors.*May incur additional fee per 1099-NEC or 1099-MISC.

Let’s Collaborate & Make a Difference!

Partner with us to amplify your mission. Whether it’s Charity accounting, financial transparency, or strategic growth—we’re here to help you create meaningful impact. Let’s work together to build a better future!

In this evolving economic landscape, collaboration with our firm offers clients a strategic advantage. With Cambodia’s reform-driven investment environment and Canada’s expanding footprint in Southeast Asia, our team of experienced consultants and legal advisors provides tailored guidance to help businesses navigate cross-border opportunities. We focus in developing comprehensive legal strategies, structuring international partnerships, and ensuring compliance in emerging markets.

By leveraging our regional insight and international expertise, you benefit from a trusted partner dedicated to helping you capitalize on growth potential in Cambodia and beyond.

Your Trusted Partner in International Bilateral Relations

At Northfield & Associates are focus in Foreign Direct Investment (FDI), international trade missions, and cross-border legal strategy. Our team of experienced consultants and legal advisors offers tailored guidance and strategic insight to help you navigate the complexities of international partnerships and development opportunities.

Whether you choose to meet in person at one of our offices or connect virtually, we provide flexible and accessible consultation options. During your session, we’ll assess your goals, review key documentation, and guide you through every stage of your FDI or trade mission engagement.

Let us help you take the next step with confidence supported by trusted legal and strategic counsel every step of the way.

Northfield & Associates

Advancing Global Partnerships, Together.

Take the First Step Today

If you believe you may be eligible for legal relief or simply need sound legal advice, we’re here to help. Contact us today to book your consultation. Let us provide the clarity, strategy, and peace of mind you need to move forward.

Disclaimer: The information contained in this article is provided for general information purposes only and does not constitute legal or other professional advice. Readers should seek tailored legal advice in relation to their personal circumstances.

We serve our clients in English, Cambodian, Vietnamese, Mandarin and Cantonese, especially in Asian clients.

If you or anybody that you know, think that you meet the requirements and wish to receive further information.

We can help you start the application process and confirm eligibility requirements to participate.

We Offer Consultations & Meetings by Phone & Virtually. Affordable Fees.

Book a Consultation Today

Contact Northfield & Associates today to schedule a consultation with an experienced Consultant.

Northfield & Associates International Corporation is a global consulting firm serving private enterprises, public institutions, not-for-profit organizations, and institutional capital providers. Operating across Cambodia, Canada, and global markets, the firm supports capital deployment, regulatory navigation, and enterprise decision-making in complex economic and geopolitical environments. Northfield & Associates delivers customized, execution-focused advisory solutions that drive measurable transformation, strengthen competitiveness, and enhance long-term highest value opportunities. The firm incorporates consulting, legal, regulatory, financial, and risk expertise to enable disciplined capital allocation, strong governance, and operational resilience. Northfield & Associates upholds a culture of applied insight and innovation, supporting clients across digital transformation, growth strategy, and organizational capability building. The firm advises individual, leading global corporations, midsize enterprises, government agencies, and mission-driven organizations through long-term partnerships. Enterprise-wide risk management, professional ethics, and fiduciary standards are embedded across all operations. Northfield & Associates’ diverse, globally unified teams are committed to execution certainty and sustainable, risk-adjusted returns aligned with ESG and stakeholder objectives.

Forward-Looking Information

This news release contains forward-looking information. All statements, other than statements of historic fact, that address activities, events or developments that the Company believes, expects or anticipates will or may occur in the future constitute forward-looking information.

This forward-looking information reflects the current expectations or beliefs of the Company based on information currently available to the Company.

Forward-looking information is subject to a number of risks and uncertainties that may cause the actual results of the Company to differ materially from those discussed in the forward-looking information, and even if such actual results are realized or substantially realized, there can be no assurance that they will have the expected consequences to, or effects on the Company. Factors that could cause actual results or events to differ materially from current expectations include, among other things: the failure to finalize negotiations concerning the increase of the Loan or to close such transaction and the failure of the Company to complete the acquisition of the Company Facility; operating performance of facilities; environmental and safety risks; delays in obtaining or failure to obtain necessary permits and approvals from government authorities; unavailability of plant, equipment or labour; inability to retain key management and personnel; changes to regulations or policies affecting the Company’s activities; and the other risks disclosed under the heading “Risk Factors” and elsewhere in the Company’s amended annual information.

Forward-looking information speaks only as of the date on which it is made and, except as may be required by applicable securities laws, the Company disclaims any intent or obligation to update any forward-looking information, whether as a result of new information, future events or results or otherwise. Although the Company believes that the assumptions inherent in the forward-looking information are reasonable, forward-looking information is not a guarantee of future performance and accordingly undue reliance should not be put on such information due to the inherent uncertainty therein.

Questions?

info@northfied.biz

Within Corporate Newsroom

Media Contact:

media@northfied.biz

Press contact

PR consultants press@northfied.biz

NOT LEGAL ADVICE. Information made available on this website in any form is for information purposes only. It is not, and should not be taken as, legal advice. You should not rely on, or take or fail to take any action based upon this information. Never disregard professional legal advice or delay in seeking legal advice because of something you have read on this website. Northfield & Associates professionals will be pleased to discuss resolutions to specific legal concerns you may have.

How Do You Register Your Federal Nonprofit or Charity as an Extra-Provincial Corporation in Ontario?

Are you planning to operate your federally incorporated nonprofit or charity in Ontario? If so, you’ll need to register it as an extra-provincial corporation with the Ontario Business Registry. This step ensures that your organization follows provincial laws, avoids penalties, and can operate, fundraise, and grow within Ontario legally.

This guide explains what extra-provincial registration means, how to do it, and also answers common questions like:

How much does it cost to register a nonprofit in Ontario?

What’s the difference between a nonprofit and a charity?

Can you start a nonprofit by yourself in Canada?

Is there a difference between “nonprofit” and “not-for-profit” in Ontario?

Let’s break it down.

Understanding Federal Versus Provincial Incorporation

When deciding between federal and provincial incorporation for a nonprofit or charity, it’s important to understand the legal frameworks and operational realities involved.

Each option offers distinct benefits and responsibilities that affect how we manage and expand our organization in Ontario and across Canada.

Key Differences Between CNCA and ONCA

The Canada Not-for-profit Corporations Act (CNCA) governs federal incorporation and provides a national standard.

It allows us to operate across all provinces without needing to re-incorporate. In contrast, the Ontario Not-for-profit Corporations Act (ONCA) applies only to Ontario-based nonprofits.

Under CNCA, our organization’s name is protected nationwide after approval. With ONCA, name protection applies only within Ontario.

Federal corporations must still register as extra-provincial when working in another province. Provincial corporations generally don’t have this national reach without extra registration.

These two acts also differ in meeting and reporting requirements. CNCA has detailed rules for member rights and annual filings.

ONCA has more flexibility but applies only within Ontario’s jurisdiction.

Wondering how federal nonprofits and charities can operate in Ontario? Learn more about CNCA vs. ONCA and explore our guide to extra-provincial registration.

It grants name protection across all provinces and territories, reducing the risk of similar names in other jurisdictions.

Federal incorporation makes it easier to open branches or conduct fundraising activities nationwide without forming new corporations.

It also enhances recognition; federally incorporated nonprofits are often seen as more credible by funders and partners outside Ontario.

Additionally, Corporations Canada provides online services to file documents and pay fees. This streamlines administrative work for organizations managing activities in multiple provinces.

Implications of Provincial Registration

Even federally incorporated nonprofits operating in Ontario must register as extra-provincial corporations under Ontario law.

This means filing documents with the Ontario government to obtain permission to carry out activities here.

Without this extra-provincial registration, we risk penalties or legal issues. The process includes submitting forms, paying fees, and keeping up with Ontario’s reporting rules.

Provincial incorporation under ONCA avoids the extra-provincial step if we work only in Ontario.

However, expanding outside Ontario requires registration in every other province where we operate. This can add complexity and costs.

Balancing extra-provincial requirements with our operational goals helps us choose the best path for managing our nonprofit or charity.

What is Extra-Provincial Registration in Ontario?

If your nonprofit or charity is incorporated federally or in another province, and you want to carry out activities in Ontario (like fundraising or hosting events), you must register as an extra-provincial corporation.

This registration tells the Ontario government that you’re doing business in the province and agree to follow its rules for nonprofits and charities.

Why You Need to Register

Registering your organization as an extra-provincial corporation allows you to:

Legally operate and fundraise in Ontario

Build trust with donors, volunteers, and grant providers

Avoid fines or penalties for non-compliance

If you skip registration, your nonprofit may not be allowed to open a bank account, apply for grants, or sign contracts in Ontario.

Step-by-Step: How to Register Your Federal Nonprofit or Charity in Ontario

Here’s a simple guide to help you through the process:

1. Confirm Federal Incorporation

Your organization must already be incorporated federally through Corporations Canada. This allows you to operate in any province, but each province including Ontario has extra steps to complete.

2. Gather Your Documents

You’ll need the following:

Certificate of Incorporation from Corporations Canada

Articles of Incorporation showing your purpose and structure

Certificate of Good Standing (proof that your nonprofit is following federal rules), when applicable

3. Complete the Ontario Application

Go to the Ontario Business Registry and fill out the Extra-Provincial Corporation application. Make sure the name and information match exactly what’s on your federal documents.

4. Appoint an Agent for Service in Ontario

You must list someone who lives in Ontario and can receive legal documents on your behalf. This can be:

A board member

A lawyer

A trusted person with a physical address in Ontario

5. Submit Your Application

Once you complete the form and upload your documents, submit everything online through the Ontario Business Registry.

6. Get Your Registration Details

After approval, you’ll receive:

An Ontario Corporation Number (OCN)

Your entity’s registered name

A transaction number

These will be needed for banking, grant applications, and other official uses.

How Much Does It Cost to Register a Nonprofit in Ontario?

The cost to register as an extra-provincial nonprofit in Ontario is currently free (as of 2025), when done through the Ontario Business Registry and where the nonprofit is incorporated federally. However, you may also have small additional costs for legal help or document preparation, or where the nonprofit is incorporated in a different province.

You should also factor in yearly maintenance costs, such as annual filings or professional assistance to keep your organization in good standing.

What’s the Difference Between a Nonprofit and a Charity in Canada?

Understanding the difference between a nonprofit and a charity in Canada is crucial before registering your organization as an extra-provincial corporation in Ontario, as each type has distinct registration requirements and procedures.

Many people use these terms interchangeably, but they’re not the same.

Nonprofit Organization

Registered Charity

Can operate for social, recreational, or advocacy purposes

Must have charitable purposes (e.g., relieving poverty, advancing education)

Cannot issue tax receipts for donations

Can issue official tax receipts for donations

Registered only under federal or provincial nonprofit laws

Must be approved and registered by the Canada Revenue Agency (CRA)

Less strct reporting rules

Must file an annual T3010 return and follow CRA rules

So, all charities are nonprofits, but not all nonprofits are charities.

What’s the Difference Between “Nonprofit” and “Not-for-Profit” in Ontario?

In Ontario, the terms nonprofit and not-for-profit mean the same thing. Both refer to organizations that do not operate to make a profit for owners or shareholders. Instead, they use their income to support their mission.

Can I Start a Nonprofit by Myself in Canada?

Yes, you can! Many people start nonprofits on their own, especially at the federal level. However, to legally incorporate your nonprofit in Ontario and most provinces, you’ll need to list at least three directors who are over 18 years old and not bankrupt. On the federal level, you can incorporate a nonprofit with just 1 director.

You can be one of the directors and bring in trusted friends, family members, or colleagues who share your vision.

Tips for a Smooth Registration

Double-Check Everything: Make sure all names, dates, and addresses match exactly with your federal records.

Stay Compliant: After registration, you must file annual returns in both Ontario and with Corporations Canada to keep your nonprofit active.

Get Help If Needed: A lawyer or nonprofit consultant can help you avoid mistakes and delays.

Benefits of Extra-Provincial Registration

Registering your federally incorporated nonprofit or charity in Ontario gives you:

Access to Ontario grants and provincial partnership programs

Room to grow your programs across Canada’s largest province

Compliance and Ongoing Obligations After Registration

Registering as an extra-provincial corporation in Ontario is just the beginning.

We must stay up to date with ongoing reporting, keep our corporate information current, and maintain any necessary permits or tax accounts.

These steps help us comply with provincial rules and keep our nonprofit in good standing with the Ontario Business Registry.

Annual Return and Reporting

We have to file an annual return with the Ontario Business Registry to maintain our registration as an extra-provincial corporation.

This return confirms our organization’s details and shows we are active in Ontario.

Typically, the annual return includes updates on the corporation’s directors, address, and contact information.

Failing to file the annual return on time can result in penalties or even the cancellation of our registration.

We must also continue filing any required reports federally with Corporations Canada.

Together, these filings keep us compliant with both provincial and federal regulations.

Updating Corporate Information

When any key changes happen—like amendments to our articles of incorporation, changes in directors, or a new registered agent in Ontario—we need to update the Ontario Business Registry.

Keeping our corporate information accurate is essential for legal notices and official communications.

We should submit updates promptly to avoid non-compliance.

The Registry requires updated forms and may charge fees for some changes.

Designating a reliable agent for service in Ontario ensures someone is always available to receive legal documents on our behalf.

Permits, Licences, and Tax Accounts

Operating legally in Ontario may require permits or licences depending on our activities.

We need to check municipal and provincial requirements to hold any necessary permissions, especially if we fundraise or hold events.

We also must keep any tax accounts in good standing, including those related to the Canada Revenue Agency and the Ontario Ministry of Finance.

This includes registering for charitable tax exemptions if applicable and remitting any required filings.

Staying on top of these ensures we avoid fines and protect our organization’s reputation.

Professional Support and Resources for Nonprofits

Navigating the registration of a federal nonprofit as an extra-provincial corporation in Ontario can involve complex legal and procedural requirements.

Expert advice, reliable service providers, and trustworthy resources can make this process smoother and help maintain ongoing compliance with Ontario’s laws.

Legal and Compliance Advisory

We recommend consulting knowledgeable legal advisors who specialize in nonprofit and charity law.

They ensure your application meets all Ontario requirements and help avoid costly errors.

Legal experts can explain the differences between nonprofit and charity statuses, guide you on appointing directors, and review your governing documents.

Organizations like B.I.G. Charity Law Group offer tailored services to handle registration paperwork correctly.

They also provide ongoing compliance advice, such as annual filing requirements and how to manage legal obligations after registration.

Though legal help is not mandatory, it significantly reduces the risk of delays or rejection of your application.

Using Intermediaries and Service Providers

We often use intermediaries or service providers that specialize in nonprofit registrations.

These services can handle your Ontario Business Registry filings, collect necessary documents, and liaise with provincial authorities on your behalf.

Using trusted intermediaries saves time and reduces stress.

They ensure your federal incorporation details match exactly in the Ontario application.

Some providers also offer packages that include guidance for future annual reports or changes to your corporation’s structure.

Choosing well-reviewed firms or groups with experience in Ontario’s nonprofit sector adds confidence.

This is especially useful if your team lacks familiarity with extra-provincial registration procedures.

Where to Find Additional Guidance

Official government sites and nonprofit-focused organizations provide up-to-date information. The Ontario Business Registry website serves as the main portal for submitting extra-provincial registration applications.

It offers guides and FAQs to explain steps and document requirements. The Canada Revenue Agency and Corporations Canada websites give details on federal incorporation and charity status.

Ontario nonprofits often consult professional groups like B.I.G. Charity Law Group for legal insights. These groups support charities and nonprofits across Canada.

Joining local nonprofit associations or networks connects you with peers and experts. You can receive informal advice and learn from shared experiences.

Final Thoughts