This module provides basic information on advantages. The key areas covered are: What is an advantage? What is split receipting? Advantages and split receipting. How does it work? The importance of Fair Market Value to advantages.

Introduction

This module introduces you to CRA’s Four Part Test.

This is one of two tests that CRA uses to determine if an activity is considered a fundraising or a charitable activity and how the activity‘s expenses have to be reported based on the result of this test.

Note: The other test is the Substantially All Test. Information on the Substantially All Test is available here.

Purpose

The Four Part Test is in the form of four main questions:

Was fundraising the main objective of the activity?

Did the activity include on-going or repeated requests, emotive requests, gift incentives, donor premiums, or other fundraising merchandise?

Was the audience selected based on its ability to give?

Was commission-based remuneration or compensation based on the number or amount of donations?

If you answer “no” to all four questions, a portion of the expenses related to the activity can be reported on the T3010 as charitable, management, or political expenses as applicable and a portion can be reported as fundraising expenses on the T3010.

If you answer “yes” to any one question, all of the activity’s expenses have to be reported as fundraising expenses on the T3010 form.

Example

Charity Z has the mission of helping seniors live a healthy and safe lives. One of its program is the prevention of elder abuse. Charity Z publishes and sends out a 4-page brochure to the general public on:

signs of elder abuse

the public should take action to stop elder abuse

how Charity Z can help

other community resources

The back cover of the brochure describes the programs of Charity Z with a note stating that donations are welcome to support the programs.

The staff and volunteer prepare and mail out this brochure as part of their regular activities. There is no compensation based on the number of donations received.

Explanation: Applying the Four Part Test to the Case of Charity Z

Fundraising is not the main objective of the activity. The purpose of the brochure is to inform the public about elder abuse and to urge them to take action. Less than 25% of the brochure content is about donations.

The brochure does not include on-going, repeated or emotive requests for donations.

The audience was not selected based on its ability to give.

There is no commission-based remuneration or compensation.

A majority of the expenses are to be allocated as charitable expenses with less than 25% as fundraising expenses.

Main Objective

Question 1: Was fundraising the main objective of the activity?

To determine whether the main object of an activity is fundraising, the CRA looks at three things:

the amount of resources devoted to the fundraising component of the activity

the nature of the activity

the content of the activity

Each of these areas is explained more below:

1(a) Amount of Resources

The amount of resources devoted to the fundraising component of the activity.

CRA considers resources to include all of a charity’s financial assets and resources such as staff, volunteers, directors, space, and equipment that the charity can use to further its purposes.

If most of your resources are used for fundraising purposes as reflected in the amount of content and the cost, then the main objective of the activity is fundraising. This is possible even if some resources are used for other objectives.

1(b) Nature of the Activity

These activities by its nature are generally considered as fundraising activities.

Paid advertisement except when the ad is only on the charity’s programs and services.

Infomercial

Telemarketing

Activities with content related to charitable gaming

Activities with content related to products and services being sold as a fundraiser by or on behalf of the charity.

Note: Free Public Service Announcement (PSA) is generally not considered a fundraising activity.

1(c) Content of the Activity

When your activity has both fundraising and charitable components, it may be difficult to separate the two components.

For example, a charity working with autistic children arranges for a television interview to discuss the challenges faced by them and their families. While talking about the issue, the need for funds and how people can donate is discussed. So how can the charitable component be distinguished from the fundraising component?

CRA looks for four features in the content of the activity to determine if it is a fundraising activity or not. In general, if an activity contains one of the features, it is a charitable activity and expenses should be allocated accordingly.

The four features of the contents of an activity that CRA looks for are:

to advance the programs and services of the charity

to raise awareness of an issue

to provide useful information to the public or the stakeholders about the charity’s work or an issue related to that work

to be transparent and accountable for its practices by providing information about its structure, operations, or performance to the public and to its stakeholders.

Each of these features of the contents of an activity is explored in detail below:

Advancing Programs and Services

If the main objective of your activity is:

to provide information to further the objectives of the charity

with

the beneficiaries or potential beneficiaries of the charity as the primary audience

This activity will generally be considered a charitable activity. The expenditures associated with the activity are thus to be reported as charitable expenditures.

Exception: When the programs and services of a charity are profiled as a means to encourage donations, the activity is considered a fundraising activity. The expenses incurred are considered fundraising expenditures.

Example:

A brochure describing the services of a seniors’ centre is distributed to seniors’ households in the area served by the centre.

Costs of the resources for this activity are considered charitable expenses since object of the activity is to further the centre as charitable objectives.

Raising Awareness

Raising awareness among the public or a segment of the public may be considered a charitable activity as long as:

it will fulfill the charity’s objective

OR

the charity has expertise on a matter of public concern

Example:

A charity buys a newspaper advertisement announcing a public forum on Labour Standards and Temporary Foreign Workers. One-quarter of the ad space states that the charity needs funds to conduct research on the issue and that donations are welcome.

The main objective of this activity is to increase public awareness and not to fundraise.

So, 75% of the expenses are charitable expenses 25% of the expenses are fundraising expenses

iii. Providing Useful Information

In this feature, a charity’s activity can be considered charitable if the activity provides useful information to:

prompt an action

OR

to change a behaviour related to its charitable objectives

AND

is directed towards its beneficiaries and/or potential beneficiaries

Providing information on the charity’s programs, services, and operations to the general public is not generally considered under this feature.

Example:

A charity whose object is to prevent prostate cancer may publish information on what prostate cancer is and why regular testing is important.

This activity is considered a charitable and not fundraising activity. Therefore, expenses incurred by this activity are not fundraising expenses.

Being Transparent and Accountable

Your charity may regularly publish reports such as annual reports, financial information, and other reports about its performance. Part of these reports may contain information acknowledging donor support and requesting further support. Because your main objective of these reports is not fundraising but rather part of being transparent and accountable, this activity would not be considered as a fundraising activity.

Exceptions:

Activities for generic branding, that is, for the promotion and marketing of your charity’s name, logo, or past work, are usually considered fundraising activities.

Promotions or branding through cause-related marketing is considered fundraising and any expenses incurred are fundraising expenses.

Question 2: Did the activity include on-going or repeated requests, emotive requests, gift incentives, donor premiums, or other fundraising merchandise?

The following activities are generally considered fundraising:

an activity including repeated or ongoing solicitations

activities that use emotional appeals in the request

telethons are usually considered fundraising as they appeal to emotion

activities that provide incentives, premiums, or merchandise to donors or prospective donors regardless of how the items are treated on the receipts.

Question 3: Target Audience – Was the audience selected based on its ability to give?

The following conditions will make an activity a fundraising activity:

the audience is selected based on its ability to give

the medium chosen for the activity attracts an audience that has the ability to give and not the potential beneficiaries or the audience that would have an interest in the charity’s programming activities

Question 4: Was commission-based remuneration or compensation based on the number or amount of donations?

This part of the test is based on how your charity calculates compensation for people involved in the charity’s activities.

If a person responsible for an activity is paid by commission or other compensation based on the amount or number of donations, the whole activity is considered fundraising.

If compensation is based on the amount of work done and not on the results, and the main objective is not fundraising, then the activity may not be considered wholly fundraising.

Exceptions

CRA recognizes that there are instances where an activity may serve multiple purposes. It may advance a charity’s programs and as a means to raise funds for the charity. So the Guidance lists three exceptions to allocation of fundraising expenditures:

An activity that raises revenues based on the charity’s work with its beneficiaries such as the sale of goods from the operation of a sheltered workshop involving persons with disabilities.

The charity mounts an event featuring its beneficiaries for treatment purposes or to foster their skills or well-being, such as a concert performance by autistic children or an endurance race to build the stamina of cancer survivors;

The charity ties a fundraising event appeal to a political activity allowed under the Income Tax Act such as mounting a public awareness campaign about a policy issue.

Note: Political activity allowed under the Income Tax Act has to be non-partisan and using less than 10% of the charity’s resources.

Summary

The four main questions in the Four Part Test are:

Was fundraising the main objective of the activity?

Did the activity include on-going or repeated requests, emotive requests, gift incentives, donor premiums, or other fundraising merchandise?

Was the audience selected based on its ability to give?

Was commission-based remuneration or compensation based on the number or amount of donations?

More information on the Four Part Test can be found at the CRA website here.

Notice

Information in this module is provided for general educational purposes and not as legal or accounting advice. Consult a lawyer or accountant for professional advice.

Information is accurate as of 2019.

For changes after this date, consult Canada Revenue Agency.

In this evolving economic landscape, collaboration with our firm offers clients a strategic advantage. With Cambodia’s reform-driven investment environment and Canada’s expanding footprint in Southeast Asia, our team of experienced consultants and legal advisors provides tailored guidance to help businesses navigate cross-border opportunities. We focus in developing comprehensive legal strategies, structuring international partnerships, and ensuring compliance in emerging markets.

By leveraging our regional insight and international expertise, you benefit from a trusted partner dedicated to helping you capitalize on growth potential in Cambodia and beyond.

Book a Consultation with Northfield & Associates

Your Trusted Partner in International Bilateral Relations

At Northfield & Associates are focus in Foreign Direct Investment (FDI), international trade missions, and cross-border legal strategy. Our team of experienced consultants and legal advisors offers tailored guidance and strategic insight to help you navigate the complexities of international partnerships and development opportunities.

Whether you choose to meet in person at one of our offices or connect virtually, we provide flexible and accessible consultation options. During your session, we’ll assess your goals, review key documentation, and guide you through every stage of your FDI or trade mission engagement.

Let us help you take the next step with confidence supported by trusted legal and strategic counsel every step of the way.

Take the First Step Today

If you believe you may be eligible for legal relief or simply need sound legal advice, we’re here to help. Contact us today to book your consultation. Let us provide the clarity, strategy, and peace of mind you need to move forward.

We serve our clients in English, Cambodian, Vietnamese, Mandarin and Cantonese, especially in Asian clients.

If you or anybody that you know, think that you meet the requirements and wish to receive further information.

We can help you start the application process and confirm eligibility requirements to participate.

We Offer Consultations & Meetings by Phone & Virtually. Affordable Fees.

Disclaimer:

The information contained in this article is provided for general information purposes only and does not constitute legal or other professional advice. Readers should seek tailored legal advice in relation to their personal circumstances.

Northfield & Associates International Corporation is a global consulting firm serving private enterprises, public institutions, not-for-profit organizations, and institutional capital providers. Operating across Cambodia, Canada, and global markets, the firm supports capital deployment, regulatory navigation, and enterprise decision-making in complex economic and geopolitical environments. Northfield & Associates delivers customized, execution-focused advisory solutions that drive measurable transformation, strengthen competitiveness, and enhance long-term highest value opportunities. The firm incorporates consulting, legal, regulatory, financial, and risk expertise to enable disciplined capital allocation, strong governance, and operational resilience. Northfield & Associates upholds a culture of applied insight and innovation, supporting clients across digital transformation, growth strategy, and organizational capability building. The firm advises individual, leading global corporations, midsize enterprises, government agencies, and mission-driven organizations through long-term partnerships. Enterprise-wide risk management, professional ethics, and fiduciary standards are embedded across all operations. Northfield & Associates’ diverse, globally unified teams are committed to execution certainty and sustainable, risk-adjusted returns aligned with ESG and stakeholder objectives.

Forward-Looking Information

This news release contains forward-looking information. All statements, other than statements of historic fact, that address activities, events or developments that the Company believes, expects or anticipates will or may occur in the future constitute forward-looking information.

This forward-looking information reflects the current expectations or beliefs of the Company based on information currently available to the Company.

Forward-looking information is subject to a number of risks and uncertainties that may cause the actual results of the Company to differ materially from those discussed in the forward-looking information, and even if such actual results are realized or substantially realized, there can be no assurance that they will have the expected consequences to, or effects on the Company. Factors that could cause actual results or events to differ materially from current expectations include, among other things: the failure to finalize negotiations concerning the increase of the Loan or to close such transaction and the failure of the Company to complete the acquisition of the Company Facility; operating performance of facilities; environmental and safety risks; delays in obtaining or failure to obtain necessary permits and approvals from government authorities; unavailability of plant, equipment or labour; inability to retain key management and personnel; changes to regulations or policies affecting the Company’s activities; and the other risks disclosed under the heading “Risk Factors” and elsewhere in the Company’s amended annual information.

Forward-looking information speaks only as of the date on which it is made and, except as may be required by applicable securities laws, the Company disclaims any intent or obligation to update any forward-looking information, whether as a result of new information, future events or results or otherwise. Although the Company believes that the assumptions inherent in the forward-looking information are reasonable, forward-looking information is not a guarantee of future performance and accordingly undue reliance should not be put on such information due to the inherent uncertainty therein.

Questions?

info@northfied.biz

Within Corporate Newsroom

Media Contact:

media@northfied.biz

Press contact

PR consultants press@northfied.biz

NOT LEGAL ADVICE. Information made available on this website in any form is for information purposes only. It is not, and should not be taken as, legal advice. You should not rely on, or take or fail to take any action based upon this information. Never disregard professional legal advice or delay in seeking legal advice because of something you have read on this website. Northfield & Associates professionals will be pleased to discuss resolutions to specific legal concerns you may have.

Must a Canadian Charity Provide Donation Receipts?

Donors expect tax receipts for their charitable contributions, but many wonder whether Canadian charities must provide them by law.

Canadian charities are not legally required to issue donation receipts. However, registered charities that choose to issue receipts must follow strict Canada Revenue Agency rules about format, timing, and eligible donations. Only registered charities can issue official donation receipts that donors can use for tax deductions.

This article explores when charities must issue receipts, what rules they must follow, and how these requirements affect both donors and charitable organizations across Canada.

Are Canadian Charities Obligated to Provide Donation Receipts?

Canadian law does not require charities to issue donation receipts. Understanding the voluntary nature of receipting helps organizations develop appropriate policies.

Legal Requirements for Issuing Receipts

Canadian law does not force charities to issue donation receipts. The Canada Revenue Agency allows registered charities to choose whether they provide receipts to donors. This means charities can accept donations without giving any receipt at all.

However, once a charity decides to issue receipts, it must follow specific CRA guidelines. These rules cover receipt format, required information, and timing of issuance. Charities that issue receipts incorrectly risk losing their registered status.

Only registered charities can issue official donation receipts that qualify for tax deductions. Non-registered organizations, even if they do charitable work, cannot provide tax-deductible receipts to their supporters.

Charity Discretion and Internal Policies

Most charities develop internal policies about when and how they issue receipts. These policies often depend on donation size, donor relationship, and administrative capacity. Small charities might only issue receipts for donations over a certain amount to manage costs.

Charities can set minimum thresholds for receipt issuance. For example, an organization might only provide receipts for donations of $20 or more. This practice helps reduce administrative burden while still serving donors who need tax documentation.

Some charities issue receipts automatically for all donations, while others require donors to specifically request them. Both approaches are legally acceptable as long as the charity communicates its policy clearly to donors.

Transparency with Donors

Clear communication about receipt policies protects both charities and donors. Charities should inform potential donors about their receipt practices before accepting donations. This prevents misunderstandings and ensures donors can make informed giving decisions.

Donors who need tax receipts should ask about a charity’s receipt policy before making their contribution. This is especially important for year-end giving when donors need receipts by December 31st for that tax year.

Charities benefit from having written receipt policies that staff can reference consistently. These policies should address donation minimums, processing timelines, and replacement procedures for lost receipts.

Who Can Issue Official Donation Receipts in Canada?

Only qualified donees recognized by the CRA can issue tax-deductible donation receipts. This status determines which organizations can provide valid receipts to donors.

Registered Charities versus Qualified Donees

Only qualified donees can issue official donation receipts that allow tax deductions in Canada. The Canada Revenue Agency maintains a strict list of organizations that qualify for this status. Most qualified donees are registered charities, but the category includes other specific organization types.

Registered charities form the largest group of qualified donees. These organizations must apply for registration with the CRA and meet ongoing compliance requirements. They receive a unique registration number that must appear on all official receipts.

Other qualified donees include registered Canadian amateur athletic associations, housing corporations, municipalities, universities, and certain government bodies. Each type has specific eligibility criteria and operates under different regulatory frameworks.

Non-profit organizations that are not registered as charities cannot issue tax-deductible receipts. Even if these groups do excellent charitable work, their donors cannot claim tax deductions for contributions without proper qualified donee status.

Registration Number Requirements

Every official donation receipt must display the organization’s CRA registration number. This number proves the organization’s qualified donee status and allows the CRA to verify receipt authenticity during tax filing.

The registration number follows a specific format: a nine-digit number followed by two letters (RR for registered charity). For example, a typical number looks like 123456789RR0001. This number must appear clearly on every receipt.

Donors should always verify registration numbers before claiming tax deductions. The CRA provides an online search tool where anyone can confirm an organization’s registered status and view its registration details.

Organizations that use incorrect or outdated registration numbers on receipts create problems for donors and face potential penalties. Charities must update their receipt templates immediately after any registration changes.

Consequences of Non-Compliance

Charities that issue improper receipts face serious penalties from the CRA. These consequences can include monetary penalties, suspension of receipting privileges, or complete revocation of charitable status.

The CRA conducts regular audits of charitable organizations and their receipting practices. Auditors examine receipt formats, donation records, and compliance with timing requirements. Organizations with poor receipting practices often trigger more frequent audits.

Donors who claim deductions using invalid receipts may face tax reassessments and penalties. The CRA can disallow claimed donations and charge interest on additional taxes owed. This creates problems for donors who trusted the organization’s receipt validity.

Loss of charitable status represents the most severe consequence for non-compliant organizations. Once revoked, organizations cannot issue receipts, may owe taxes on accumulated assets, and face significant barriers to re-registration.

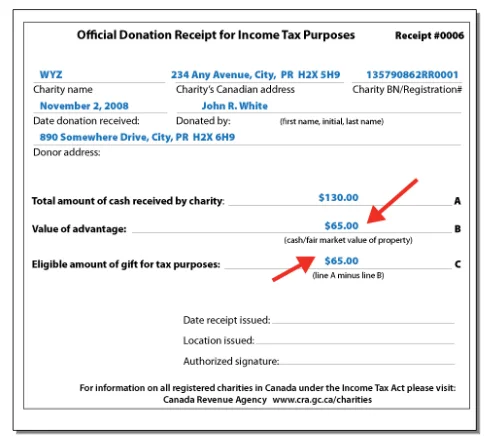

What Constitutes an Official Donation Receipt?

Official receipts must meet specific CRA requirements to be valid for tax purposes. Missing elements can invalidate receipts and prevent donors from claiming tax credits.

Mandatory Information on Receipts

The CRA requires specific information on every official donation receipt. Missing any required element makes the receipt invalid for tax purposes. Charities must include:

Organization’s complete legal name and address

Registration number (format: 123456789RR0001)

Receipt serial number for tracking

Date of donation and receipt issue date

Donor’s complete name and address

Donation amount in Canadian dollars

Description of donated items (for gifts-in-kind)

Statement that the receipt is for income tax purposes

Authorized signature from organization representative

Receipts must clearly state the donation amount. For cash donations, charities list the exact dollar figure. For gifts-in-kind, they must include fair market value determined by qualified appraisal.

The receipt must specify whether the donor received any advantage in return. If the donor got goods or services worth more than minimal value, the receipt must show the eligible donation amount after deducting the advantage value.

Every receipt needs a unique serial number that the charity can track. This number helps the CRA verify receipt authenticity and prevents duplicate claims. Charities design their own numbering systems but must ensure each receipt has a distinct identifier.

Most organizations use sequential numbering systems like 2024-001, 2024-002, etc. Others combine letters and numbers or include location codes. The system doesn’t matter as long as each receipt gets a unique number.

Charities must maintain detailed records linking each serial number to:

Donor information

Donation details

Issue date

Supporting documentation

These records help charities respond to CRA inquiries and replace lost receipts. The CRA requires organizations to keep these records for at least two years after the last tax return filing deadline.

Authorized Signatures and Validity

Official receipts require signatures from authorized organization representatives. The CRA doesn’t specify who can sign, but charities typically authorize board members, senior staff, or designated volunteers.

Organizations should maintain a list of authorized signers and update it regularly. Staff changes, board turnover, and policy updates can affect who has signing authority. Current signers need access to signature specimens for consistency.

Digital signatures are acceptable if they meet security requirements. Electronic receipt systems must prevent unauthorized access and maintain audit trails. Many charities use password-protected systems with user authentication.

Receipts become valid when the charity issues them, not when donors receive them. However, donors need receipts by December 31st to claim deductions for that tax year. This timing requirement affects year-end donation processing and mailing schedules.

Types of Gifts and Issuing Appropriate Receipts

Different donation types require specific receipting approaches. Cash gifts are straightforward, while non-cash donations need valuation. Split receipting applies when donors receive benefits.

Cash Donations and Receipts

Charities issue receipts for exact amounts received through cash, cheque, credit card, or electronic transfer. Processing fees don’t reduce the receipt amount.

Monthly donations can use individual receipts or annual summaries. Failed payments require record adjustments to match actual funds received.

Non-Cash Gifts and Fair Market Value

Non-cash gifts require fair market value determination. The CRA requires professional appraisals for gifts over $1,000.

Valuation rules:

Securities: Closing price on donation date

Real estate: Professional appraisal required

Artwork: Qualified art appraiser assessment

Vehicles: Recognized valuation guides

Receipts must describe gifts specifically, not with generic terms like “household goods.”

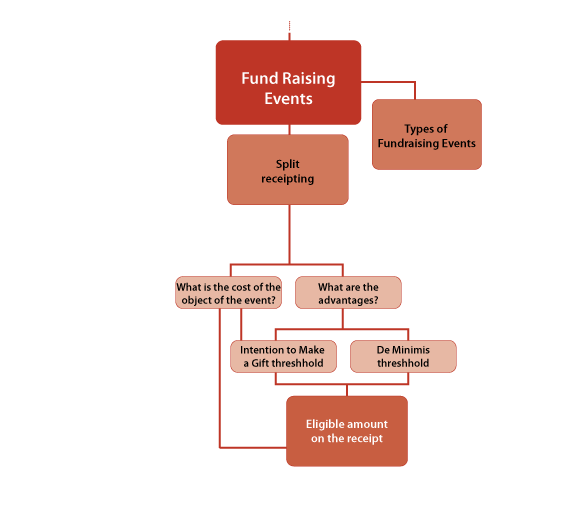

Split Receipting and Advantages

Split receipting applies when donors receive benefits. Receipts show eligible donation amounts after deducting advantage values.

Common examples:

Charity auction purchases

Fundraising dinner tickets

Golf tournament fees

Premium gifts

If advantage value exceeds 80% of payment, no receipt can be issued. For payments under $75, advantages under $75 don’t affect receipt amounts.

Charities should communicate advantage calculations before events to prevent donor disappointment.

Eligible and Ineligible Donations for Receipting

Not all payments qualify for donation receipts. Understanding eligibility rules helps charities issue proper receipts and avoid CRA penalties.

Gifts that Qualify for Receipts

True gifts made voluntarily without expectation of benefit qualify for receipts. Donors must transfer property ownership to the charity with no strings attached.

The CRA sets no minimum amount for donation receipts. Charities can choose their own thresholds based on administrative costs.

Common minimum amounts:

$10 for online donations

$20 for mail-in gifts

$25 for event donations

Charities must apply minimums consistently and communicate policies clearly to donors.

Business and Sponsorship Contributions

Business payments often mix charitable donations with sponsorship benefits. Only the charitable portion qualifies for receipts.

Corporate sponsorships typically include:

Logo placement and recognition

Promotional opportunities

Networking access

Marketing materials

Charities must calculate fair market value of benefits provided. The receipt shows payment minus benefit value. Pure donations from businesses without benefits qualify for full receipts.

Implications for Donors and Charities

Donation receipts create obligations and opportunities for both parties. Understanding tax implications and record-keeping requirements ensures compliance.

Tax Credits and Deductibility

Donors receive non-refundable tax credits, not deductions, for charitable donations. Credits reduce taxes owed dollar-for-dollar up to specified limits.

Federal tax credit rates:

15% on first $200 donated annually

29% on amounts over $200

Additional 4% for high-income earners

Provincial credits vary by jurisdiction. Combined federal-provincial credits can exceed 40% in some provinces.

Donors can carry forward unused credits for up to five years if annual limits prevent full use.

Income Tax Purposes and Reporting

Donors claim charitable donations on their tax returns using official receipts. The CRA matches receipt information with charity records during processing.

Annual donation limits:

75% of net income for most donations

100% of net income for certain gifts

No limit for donations to Crown, provinces, or municipalities

Married couples can combine donations on one return to maximize higher credit rates on amounts over $200.

Record Keeping and CRA Audits

Donors must keep original receipts for six years after filing their tax return. Digital copies are acceptable if they meet CRA standards.

The CRA audits both donors and charities. Auditors verify:

Receipt authenticity and format

Donation amounts and dates

Charity registration status

Proper advantage calculations

Charities must maintain donor records for a minimum of two years. Best practice involves keeping records longer to support donor relationships and audit requests.

Poor record keeping can result in denied tax credits for donors and penalties for charities. Electronic systems help maintain organized, accessible records.

Canadian charities are not legally required to issue donation receipts, but those who choose to must follow strict CRA guidelines. Only registered charities can issue official receipts that qualify for tax credits.

Understanding receipt requirements protects both charities and donors from costly mistakes. Proper compliance prevents penalties and maintains charitable status while building stronger donor relationships.

For expert guidance on charitable compliance and donation receipt requirements, connect with experienced charity law professionals.

Common questions about Canadian charity receipts and their requirements. These answers provide quick guidance for donors and charitable organizations.

What is required on a charity receipt in Canada?

Canadian charity receipts must include the organization’s legal name and address, CRA registration number, unique serial number, donation date, donor’s name and address, donation amount, and an authorized signature.

What legally needs to be on a receipt in Canada?

The CRA requires receipts to show the charity’s registration number, serial number, donation amount, donor information, and a statement that the receipt is for income tax purposes. Missing any element makes the receipt invalid.

How to generate a donation receipt?

Create receipts using the charity’s official template with all required information. Assign unique serial numbers, obtain authorized signatures, and maintain detailed records linking each receipt to donor and donation details.

How to acknowledge receipt of donation?

Send thank-you letters separate from official tax receipts. Acknowledgements can be informal but should confirm the donation amount and express gratitude. Tax receipts serve the legal purpose of enabling tax credits.

What should be included in a valid donation receipt for tax purposes?

Valid receipts include charity name, address, registration number, receipt serial number, donation date, donor details, amount, description of gift (if non-cash), advantage calculation (if applicable), and authorized signature.

By what deadline must Canadian charities issue tax receipts for donations?

The CRA requires no specific deadline for issuing receipts. However, donors need receipts by December 31st to claim tax credits for that year. Most charities issue receipts immediately or within 30 days of receiving donations.

In this evolving economic landscape, collaboration with our firm offers clients a strategic advantage. With Cambodia’s reform-driven investment environment and Canada’s expanding footprint in Southeast Asia, our team of experienced consultants and legal advisors provides tailored guidance to help businesses navigate cross-border opportunities. We focus in developing comprehensive legal strategies, structuring international partnerships, and ensuring compliance in emerging markets.

By leveraging our regional insight and international expertise, you benefit from a trusted partner dedicated to helping you capitalize on growth potential in Cambodia and beyond.

Book a Consultation with Northfield & Associates

Your Trusted Partner in International Bilateral Relations

At Northfield & Associates are focus in Foreign Direct Investment (FDI), international trade missions, and cross-border legal strategy. Our team of experienced consultants and legal advisors offers tailored guidance and strategic insight to help you navigate the complexities of international partnerships and development opportunities.

Whether you choose to meet in person at one of our offices or connect virtually, we provide flexible and accessible consultation options. During your session, we’ll assess your goals, review key documentation, and guide you through every stage of your FDI or trade mission engagement.

Let us help you take the next step with confidence supported by trusted legal and strategic counsel every step of the way.

Take the First Step Today

If you believe you may be eligible for legal relief or simply need sound legal advice, we’re here to help. Contact us today to book your consultation. Let us provide the clarity, strategy, and peace of mind you need to move forward.

We serve our clients in English, Cambodian, Vietnamese, Mandarin and Cantonese, especially in Asian clients.

If you or anybody that you know, think that you meet the requirements and wish to receive further information.

We can help you start the application process and confirm eligibility requirements to participate.

We Offer Consultations & Meetings by Phone & Virtually. Affordable Fees.

Disclaimer:

The information contained in this article is provided for general information purposes only and does not constitute legal or other professional advice. Readers should seek tailored legal advice in relation to their personal circumstances.

Northfield & Associates International Corporation is a global consulting firm serving private enterprises, public institutions, not-for-profit organizations, and institutional capital providers. Operating across Cambodia, Canada, and global markets, the firm supports capital deployment, regulatory navigation, and enterprise decision-making in complex economic and geopolitical environments. Northfield & Associates delivers customized, execution-focused advisory solutions that drive measurable transformation, strengthen competitiveness, and enhance long-term highest value opportunities. The firm incorporates consulting, legal, regulatory, financial, and risk expertise to enable disciplined capital allocation, strong governance, and operational resilience. Northfield & Associates upholds a culture of applied insight and innovation, supporting clients across digital transformation, growth strategy, and organizational capability building. The firm advises individual, leading global corporations, midsize enterprises, government agencies, and mission-driven organizations through long-term partnerships. Enterprise-wide risk management, professional ethics, and fiduciary standards are embedded across all operations. Northfield & Associates’ diverse, globally unified teams are committed to execution certainty and sustainable, risk-adjusted returns aligned with ESG and stakeholder objectives.

Forward-Looking Information

This news release contains forward-looking information. All statements, other than statements of historic fact, that address activities, events or developments that the Company believes, expects or anticipates will or may occur in the future constitute forward-looking information.

This forward-looking information reflects the current expectations or beliefs of the Company based on information currently available to the Company.

Forward-looking information is subject to a number of risks and uncertainties that may cause the actual results of the Company to differ materially from those discussed in the forward-looking information, and even if such actual results are realized or substantially realized, there can be no assurance that they will have the expected consequences to, or effects on the Company. Factors that could cause actual results or events to differ materially from current expectations include, among other things: the failure to finalize negotiations concerning the increase of the Loan or to close such transaction and the failure of the Company to complete the acquisition of the Company Facility; operating performance of facilities; environmental and safety risks; delays in obtaining or failure to obtain necessary permits and approvals from government authorities; unavailability of plant, equipment or labour; inability to retain key management and personnel; changes to regulations or policies affecting the Company’s activities; and the other risks disclosed under the heading “Risk Factors” and elsewhere in the Company’s amended annual information.

Forward-looking information speaks only as of the date on which it is made and, except as may be required by applicable securities laws, the Company disclaims any intent or obligation to update any forward-looking information, whether as a result of new information, future events or results or otherwise. Although the Company believes that the assumptions inherent in the forward-looking information are reasonable, forward-looking information is not a guarantee of future performance and accordingly undue reliance should not be put on such information due to the inherent uncertainty therein.

Questions?

info@northfied.biz

Within Corporate Newsroom

Media Contact:

media@northfied.biz

Press contact

PR consultants press@northfied.biz

NOT LEGAL ADVICE. Information made available on this website in any form is for information purposes only. It is not, and should not be taken as, legal advice. You should not rely on, or take or fail to take any action based upon this information. Never disregard professional legal advice or delay in seeking legal advice because of something you have read on this website. Northfield & Associates professionals will be pleased to discuss resolutions to specific legal concerns you may have.

When charities receive donations with specific instructions from donors, they must handle these restricted funds differently from regular donations.

Restricted funds require separate tracking, careful documentation, and precise reporting to ensure every dollar goes exactly where the donor intended. Mismanaging these funds can lead to serious problems, including fines, lawsuits, or loss of charitable status.

This guide walks through the essential steps for handling restricted fund accounting properly. We’ll cover the core principles you need to know, different types of restrictions you might encounter, and practical systems for tracking and reporting on these funds. You’ll also learn about internal controls that protect your organization and ensure compliance with accounting standards.

Core Principles of Restricted Fund Accounting

Restricted fund accounting operates on three key foundations.

First, we must clearly separate funds with and without donor limitations.

Second, we need systematic tracking methods that honor donor wishes.

Third, we must strictly follow how donors intend their gifts to be used.

Definition of Restricted and Unrestricted Funds

Restricted funds are donations that donors have designated for specific purposes.

We cannot use these funds for any other activities without the donor’s permission.

These funds come with clear instructions.

A donor might give money for building repairs, youth programs, or medical equipment.

Unrestricted funds have no donor-imposed limitations.

We can use these donations for any legitimate organizational purpose.

Unrestricted funds help cover general expenses like staff salaries, utilities, rent, office supplies, and emergency needs.

The key difference lies in flexibility.

Restricted funds must follow donor rules exactly, while unrestricted funds let us address our most pressing needs.

Both types are important.

Restricted funds often support specific programs, and unrestricted funds keep our operations running smoothly.

Purpose and Significance of Fund Accounting

Fund accounting helps us track different types of donations separately.

This system ensures we use each gift according to donor wishes.

We must report restricted and unrestricted funds in different categories.

This separation shows donors and regulators how we manage their contributions.

Financial statements require three main sections:

Without donor restrictions (unrestricted funds)

With donor restrictions (temporarily restricted)

With donor restrictions (permanently restricted)

This accounting method builds trust with donors.

They can see exactly how we used their specific gifts.

Fund accounting also protects our organization legally.

Mixing restricted funds with general funds can lead to fines, lawsuits, or loss of charitable status.

The system helps us plan better budgets.

We know which funds are available for general use and which have specific purposes.

Donor Intent and Donor Restrictions

Donor intent represents the specific purpose a donor had in mind when making their gift.

We must understand and document these intentions clearly.

Common types of donor restrictions include:

Time restrictions (use funds within certain dates)

Purpose restrictions (specific programs or projects)

We cannot change donor restrictions without written permission.

If a project costs less than expected, we cannot automatically use leftover funds elsewhere.

Documentation is crucial.

We must keep records of all donor communications and agreements, including emails, letters, and grant agreements.

When restrictions become impossible to follow, we must contact the donor.

Sometimes circumstances change and original plans no longer work.

Clear communication prevents problems.

We should discuss any concerns about restrictions before accepting large gifts.

Types of Restricted Funds in Charities

Charities receive donations with different types of restrictions that affect how and when funds can be used.

These restrictions fall into three main categories based on time limits, permanence, and specific purposes outlined by donors.

Temporarily Restricted Funds

Temporarily restricted funds have donor-imposed limitations that expire over time or when certain conditions are met.

These restrictions typically involve time restrictions or specific project completion requirements.

Common examples include donations for annual programs or multi-year initiatives.

A donor might give $25,000 for youth programs to be spent over three years.

Once we use the funds according to the donor’s wishes, the restrictions are released.

Time restrictions are the most frequent type of temporary restriction.

Donors specify when funds must be used, such as “for the 2026 summer camp program” or “to be spent within five years of receipt.”

We must track these funds carefully in our financial records.

When restrictions are satisfied, we transfer the funds from temporarily restricted to unrestricted net assets on our statement of activities.

Temporary restrictions will eventually be lifted.

This gives us more flexibility in long-term planning once conditions are met.

Permanently Restricted Funds

Permanently restricted funds maintain donor restrictions that never expire.

The principal amount must remain intact forever, though we can often use investment earnings according to donor specifications.

Endowments are the most common type of permanently restricted funds.

Donors create endowments to provide ongoing income for specific purposes while preserving the original gift amount.

For example, a $100,000 endowment for scholarships means we keep the $100,000 invested permanently.

We can use the annual investment earnings to fund scholarships, but the original amount stays untouched.

These funds require special investment management and accounting treatment.

We must maintain detailed records showing the original gift amount and any accumulated earnings or losses.

Legacy gifts often come with permanent restrictions.

Donors want their contributions to support our mission indefinitely, creating lasting impact beyond their lifetime.

Purpose-Restricted Funds

Purpose-restricted funds must be used for specific programs, activities, or expenses as designated by the donor.

These restrictions focus on how funds are spent rather than when they’re spent.

Purpose restrictions can be narrow or broad.

A donor might restrict funds for “veterinary supplies” (narrow) or “animal care programs” (broad).

We must honor the exact wording of the restriction.

Common categories include:

Program-specific donations for particular services

Capital campaigns for buildings or equipment

Operating expenses like rent or utilities

Staff salaries for specific positions

We need separate tracking systems for each purpose-restricted fund.

Our accounting records must clearly show which expenses are charged against which restricted funds.

Some donors combine purpose and time restrictions.

A gift might be restricted for “education programs in 2025 only,” creating both purpose and temporary restrictions we must manage at the same time.

Establishing and Tracking Restricted Income

Proper income identification and tracking systems ensure compliance with donor restrictions while maintaining accurate financial records.

Clear documentation and systematic tracking prevent misuse of restricted funds and support transparent reporting.

Identifying Restricted vs. Unrestricted Donations

We must clearly distinguish between restricted and unrestricted donations at the point of receipt.

Restricted income comes with specific donor-imposed limitations on how we can use the funds.

Unrestricted funds have no donor restrictions.

We can use these donations for any legitimate organizational purpose, including general operating expenses, administrative costs, or program activities.

Common types of restricted donations include:

Program-specific gifts for particular projects

Capital campaign contributions for buildings or equipment

Endowment funds with spending restrictions

Operating expense donations for specific costs like utilities

Time restrictions also matter.

Some donations must be used within specific timeframes, while others may be restricted until certain conditions are met.

We should document the restriction type immediately when receiving each donation.

This prevents confusion later and ensures proper accounting treatment.

Gift Instruments and Documentation

Every restricted donation requires proper documentation to capture donor intent accurately.

Gift instruments serve as legal proof of the donor’s wishes and restriction terms.

Key documentation includes:

Written donor correspondence stating restrictions

Grant agreements outlining fund usage requirements

Pledge cards with specific designation fields

Donation receipts noting any restrictions

We must review all gift documentation carefully before accepting restricted funds.

If restrictions conflict with our mission or capacity, we should discuss modifications with the donor or decline the gift.

Store original documentation in secure files linked to our accounting system.

Digital copies provide backup access while keeping organized records for audits.

Essential information to capture:

Exact restriction language from the donor

Start and end dates for time-restricted funds

Spending requirements or limitations

Reporting obligations to the donor

Clear documentation protects our organization and honors the donor’s wishes.

Implementing a Tracking Process

Our accounting system must separate restricted and unrestricted funds from the moment we receive them.

This requires specific procedures and internal controls.

Set up separate fund codes or accounts for each type of restriction.

Use distinct numbering systems that clearly identify the fund purpose and restriction type.

Tracking requirements include:

Fund Type

Account Setup

Reporting Needs

Unrestricted

General operating accounts

Statement of activities

Temporarily restricted

Separate fund codes

Restriction tracking reports

Permanently restricted

Endowment accounts

Investment performance reports

Record all restricted income in the appropriate fund account immediately upon receipt.

Never deposit restricted funds into general unrestricted accounts, even temporarily.

Monthly reconciliation ensures restricted fund balances match donor restrictions.

Compare actual spending against allowable uses for each restricted fund.

We should generate regular reports showing restricted fund activity.

These reports help management monitor compliance and provide transparency to donors about how we use their gifts.

Train all staff who handle donations on proper restriction identification and recording procedures.

Consistent processes prevent errors that could lead to compliance issues.

Proper accounting for restricted funds requires careful tracking and allocation methods that maintain donor restrictions and ensure accurate financial reporting.

We must record these funds separately from unrestricted donations and allocate expenses according to specific guidelines.

Recording Restricted Funds

We need to set up our accounting system to track restricted funds separately from unrestricted donations.

This starts with creating distinct accounting codes or fund accounts for each type of restriction.

Our chart of accounts should include separate categories for temporarily restricted and permanently restricted net assets.

We record restricted donations in these specific accounts when we receive them.

The balance sheet must show restricted funds as separate line items.

We cannot mix restricted and unrestricted net assets together on our financial statements.

We should establish separate bank accounts for major restricted funds when possible.

This makes tracking easier and reduces the risk of accidentally spending restricted money on the wrong purpose.

Our accounting system needs to track each restriction’s purpose, timeline, and remaining balance.

We must document exactly what each donor specified when they made their gift.

When we spend restricted funds, we move the money from restricted net assets to unrestricted net assets.

This shows that we have met the donor’s requirements.

Expense Allocation and Indirect Costs

We can only charge expenses to restricted funds if they directly relate to the restricted purpose.

Direct costs like program supplies or staff salaries for specific projects are usually acceptable.

Indirect costs require more careful handling.

We can allocate administrative expenses like rent or utilities to restricted funds only if our organization has an approved indirect cost rate.

Many donors limit how much we can spend on overhead costs.

We need to check each restriction to see what percentage can go toward administrative expenses versus program costs.

We should create allocation formulas based on reasonable methods like staff time, square footage, or program budgets.

These formulas must be consistent and well-documented.

Our financial statements must show how we allocated expenses between restricted and unrestricted activities.

This transparency helps donors see how we used their gifts.

Financial Reporting and Compliance

Charities must follow specific reporting standards when handling restricted funds. This helps maintain donor trust and meet legal requirements.

Proper financial statements separate restricted and unrestricted net assets. Regulatory bodies require detailed documentation of how we use these funds.

Reporting in Financial Statements

We must clearly separate restricted and unrestricted funds in our financial statements. The statement of financial position shows net assets with donor restrictions and net assets without donor restrictions as distinct categories.

Our balance sheet displays restricted funds as separate line items. This separation helps readers understand which assets we can use freely and which have limitations.

The statement of activities breaks down revenue and expenses by restriction type. We list temporarily restricted funds that will become available when conditions are met.

Permanently restricted funds appear separately since these restrictions never expire.

Key Financial Statement Elements:

Statement of financial position with separated net assets

Statement of activities showing restricted revenue

Cash flow statements track restricted fund movements

Notes explaining restriction details and purposes

We must document all restriction details in the notes to the financial statements. These notes explain the nature of restrictions and when temporarily restricted funds might become available.

Regulatory Requirements for Charities

Charities face strict rules about restricted fund management from multiple regulatory bodies. We must maintain accurate records that prove we’re using restricted funds according to donor wishes.

Revenue agencies require us to file annual returns that detail our restricted fund activities. These filings must show how we’ve used restricted donations and whether we’ve met all donor conditions.

Provincial charity regulators often have additional reporting requirements. We may need to submit detailed financial reports that break down restricted fund usage by program or purpose.

Annual information returns with restricted fund details

Quarterly reports for large restricted donations

Special reporting for government grants

Documentation of donor communications and agreements

Failure to meet these requirements can result in penalties, loss of charitable status, or legal action. We must keep detailed records of all restricted fund transactions and decisions.

Producing Donor Reports

Donor reports build trust by showing exactly how we’ve used restricted funds. We should create clear, specific reports that demonstrate the impact of restricted donations.

Our donor reports include financial summaries showing how much we’ve spent and what remains. We provide program updates that connect spending to actual outcomes and beneficiaries.

Effective Donor Report Elements:

Financial breakdown of fund usage

Program outcomes and beneficiary stories

Photos or evidence of funded activities

Timeline of fund expenditure and remaining balance

We send reports at agreed intervals, typically quarterly or annually. Some donors require approval before we spend restricted funds, so we include spending plans in our reports.

Large restricted donations often need special reporting arrangements. We work with major donors to create custom reports that meet their specific information needs while protecting beneficiary privacy.

Effective Management and Internal Controls

Strong internal controls and proper management systems help charities track restricted funds accurately. The right technology and clear procedures make compliance easier while reducing the risk of fund misuse.

Best Practices for Managing Restricted Funds

We need to separate restricted funds from unrestricted money right from the start. This means creating different accounts or fund codes in our accounting system for each type of restriction.

Documentation is critical. We should record every detail about donor restrictions when we receive the gift.

This includes the specific purpose, any time limits, and what happens if we can’t use all the money.

Our team needs clear roles for who can approve spending from restricted funds. We recommend having at least two people review each expense before we pay it.

Regular monitoring keeps us on track. We should check our restricted fund balances monthly to make sure we’re not overspending.

This also helps us spot problems early.

We need to train our staff on the rules for restricted funds. Everyone who handles money should understand why we can’t move funds between different restrictions.

Implementing Internal Controls

Strong internal controls start with separating duties. We should have different people who receive donations, record them, and approve spending from restricted accounts.

Our approval process needs multiple levels. Small expenses might need one signature, but larger amounts should require two or more approvals from senior staff or board members.

We need regular reconciliation of our accounts. Someone who doesn’t handle the daily bookkeeping should review our restricted fund records each month.

Written policies protect our organisation. We should document exactly how we handle restricted funds, who can make decisions, and what steps we follow for different situations.

Our board should review restricted fund reports at each meeting. This oversight helps catch mistakes and shows donors we take their restrictions seriously.

Technology Solutions for Charities

Nonprofit accounting software makes managing restricted funds much easier than basic bookkeeping programs. These systems let us tag each donation with its specific restrictions automatically.

Fund accounting features are essential. We need software that can track multiple funds separately while still giving us organisation-wide financial reports.

Cloud-based systems help our team access restricted fund information from anywhere. This is especially helpful when multiple staff members need to check fund balances before making spending decisions.

Integration saves time and reduces errors. Our donation platform should connect directly to our accounting system so restricted gifts get coded properly from the start.

We should look for software that generates compliance reports automatically. This makes it easier to show donors and auditors how we’ve used their restricted gifts properly.

Conclusion

Managing restricted funds requires careful attention to detail and strong systems. When we track these donations properly, we build trust with donors and stay compliant with regulations.

The key steps are simple but important: understand donor rules, track funds separately, and budget carefully. Transparency helps us show donors how their money makes a difference.

Good restricted fund management protects our charity’s reputation and mission. It also helps us use every dollar the way donors intended. Ready to improve your charity’s fund accounting?

Navigating director compensation rules can be complex.

Contact Northfield & Associates for expert guidance on compliance requirements. Our team understands Canadian charity law and can help ensure your organisation follows proper procedures.

Managing restricted funds raises many practical questions about proper accounting methods and compliance requirements. These common concerns focus on recording procedures, classification differences, and financial statement presentation.

What is a restricted account in accounting?

A restricted account holds donations that must be used for specific purposes set by the donor. We cannot use these funds for general operating expenses or other activities.

How do I record restricted funds?

Record restricted funds separately from unrestricted donations in your accounting system. Each restricted gift gets its own tracking code or fund designation, and your income statement must show restricted and unrestricted revenue in different categories.

What is the difference between restricted and unrestricted accounting?

Unrestricted funds have no donor limitations on how you use them. Restricted funds come with specific donor instructions that you must follow exactly. Your financial statements must separate these two types clearly.

Is restricted cash a liability or asset?

Restricted cash is an asset on your balance sheet. You own the money, but must use it according to donor instructions. Show restricted cash separately from unrestricted cash on your financial statements.

How do you show restricted funds on a balance sheet?

List restricted cash as a separate line item under assets. Your net assets section shows funds with donor restrictions separately from unrestricted net assets, as required by accounting standards.

What is an example of a restricted account?

A building fund where donors give money specifically for facility improvements. An endowment fund where you keep the original donation intact and only spend investment earnings. Program-specific donations like “for animal care only” must be tracked separately.

Ready for better nonprofit reporting?

At Northfield & Associates, we have a team of professional bookkeepers and accountants to help your organization manage the books so that you can breeze through tax season.

We’re often asked by prospective clients what our Bookkeeping Service covers? People want to know what specific tasks we do, and what their responsibility is. This brief explainer page will answer that question. This is by no means an exhaustive list, but covers the most frequently asked questions.

Getting Started

Review your existing books for needed corrections or back-work

Chart of accounts setup or amendment

Assistance with setting up bank feeds

Limited assistance* with setting up payroll (QBO or Gusto only)

Your books brought current and reconciled if needed

Ongoing Monthly Bookkeeping

After-the-fact transaction recording

Post to general ledger

Post to other ledgers (as needed)

Bank account reconciliation

Monthly financial statements

Other bookkeeping services, as required

Best-practice bookkeeping advice and counsel

Year End

Assistance with 1099-NEC preparation*

Assistance with 1099-MISC preparation*

Year-end financial statements and period-end closing

What We Don’t Do

Pay bills

We do not offer bill-pay services at this time, nor do we manage Accounts Payable (AP) or Accounts Receivable (AR).

Payroll tax responsibility

Our bookkeepers can assist you in setting up your initial payroll service in QBO or Gusto. We are not responsible for entering payroll hours/salary, accruing payroll taxes, nor the transmittal of payroll taxes to the IRS or the state. Your full-service payroll provider (QBO, Gusto, or whatever other service a client uses) will be the responsible party for payroll and payroll tax compliance.

*Payroll deductions and benefits

We provide assistance with setting up a payroll account in either Quickbooks Online or Gusto, including entry of employee data. We do not assist in state registrations, benefits, or advise on deductions. Those service areas are provided directly by either QBO or Gusto.

Preparation of W2s

Similar to the last item, your full-service payroll provider (QBO/Gusto) is responsible for preparation of Form W2 for employees.

Sales tax reporting

For those nonprofits that sell taxable goods and/or services, your bookkeeper will assist in accounting for sales taxes collected and transmitted, but we do not prepare state sales tax reports.

Donation recording

We do not provide individual donation data entry into your neither your donor CRM nor Quickbooks Online, nor do we prepare year-end donor acknowledgements.

Administrative tasks

We cannot provide administrative services unrelated to our bookkeeping function.

Attend board meetings

Due to the constraints of time and distance, we are unable to be present, physically nor virtually, at a meeting of a client’s board of directors.*May incur additional fee per 1099-NEC or 1099-MISC.

Let’s Collaborate & Make a Difference!

Partner with us to amplify your mission. Whether it’s Charity accounting, financial transparency, or strategic growth—we’re here to help you create meaningful impact. Let’s work together to build a better future!

In this evolving economic landscape, collaboration with our firm offers clients a strategic advantage. With Cambodia’s reform-driven investment environment and Canada’s expanding footprint in Southeast Asia, our team of experienced consultants and legal advisors provides tailored guidance to help businesses navigate cross-border opportunities. We focus in developing comprehensive legal strategies, structuring international partnerships, and ensuring compliance in emerging markets.

By leveraging our regional insight and international expertise, you benefit from a trusted partner dedicated to helping you capitalize on growth potential in Cambodia and beyond.

Your Trusted Partner in International Bilateral Relations

At Northfield & Associates are focus in Foreign Direct Investment (FDI), international trade missions, and cross-border legal strategy. Our team of experienced consultants and legal advisors offers tailored guidance and strategic insight to help you navigate the complexities of international partnerships and development opportunities.

Whether you choose to meet in person at one of our offices or connect virtually, we provide flexible and accessible consultation options. During your session, we’ll assess your goals, review key documentation, and guide you through every stage of your FDI or trade mission engagement.

Let us help you take the next step with confidence supported by trusted legal and strategic counsel every step of the way.

Northfield & Associates

Advancing Global Partnerships, Together.

Take the First Step Today

If you believe you may be eligible for legal relief or simply need sound legal advice, we’re here to help. Contact us today to book your consultation. Let us provide the clarity, strategy, and peace of mind you need to move forward.

Disclaimer: The information contained in this article is provided for general information purposes only and does not constitute legal or other professional advice. Readers should seek tailored legal advice in relation to their personal circumstances.

We serve our clients in English, Cambodian, Vietnamese, Mandarin and Cantonese, especially in Asian clients.

If you or anybody that you know, think that you meet the requirements and wish to receive further information.

We can help you start the application process and confirm eligibility requirements to participate.

We Offer Consultations & Meetings by Phone & Virtually. Affordable Fees.

Book a Consultation Today

Contact Northfield & Associates today to schedule a consultation with an experienced Consultant.

Northfield & Associates International Corporation is a global consulting firm serving private enterprises, public institutions, not-for-profit organizations, and institutional capital providers. Operating across Cambodia, Canada, and global markets, the firm supports capital deployment, regulatory navigation, and enterprise decision-making in complex economic and geopolitical environments. Northfield & Associates delivers customized, execution-focused advisory solutions that drive measurable transformation, strengthen competitiveness, and enhance long-term highest value opportunities. The firm incorporates consulting, legal, regulatory, financial, and risk expertise to enable disciplined capital allocation, strong governance, and operational resilience. Northfield & Associates upholds a culture of applied insight and innovation, supporting clients across digital transformation, growth strategy, and organizational capability building. The firm advises individual, leading global corporations, midsize enterprises, government agencies, and mission-driven organizations through long-term partnerships. Enterprise-wide risk management, professional ethics, and fiduciary standards are embedded across all operations. Northfield & Associates’ diverse, globally unified teams are committed to execution certainty and sustainable, risk-adjusted returns aligned with ESG and stakeholder objectives.

Forward-Looking Information

This news release contains forward-looking information. All statements, other than statements of historic fact, that address activities, events or developments that the Company believes, expects or anticipates will or may occur in the future constitute forward-looking information.

This forward-looking information reflects the current expectations or beliefs of the Company based on information currently available to the Company.

Forward-looking information is subject to a number of risks and uncertainties that may cause the actual results of the Company to differ materially from those discussed in the forward-looking information, and even if such actual results are realized or substantially realized, there can be no assurance that they will have the expected consequences to, or effects on the Company. Factors that could cause actual results or events to differ materially from current expectations include, among other things: the failure to finalize negotiations concerning the increase of the Loan or to close such transaction and the failure of the Company to complete the acquisition of the Company Facility; operating performance of facilities; environmental and safety risks; delays in obtaining or failure to obtain necessary permits and approvals from government authorities; unavailability of plant, equipment or labour; inability to retain key management and personnel; changes to regulations or policies affecting the Company’s activities; and the other risks disclosed under the heading “Risk Factors” and elsewhere in the Company’s amended annual information.

Forward-looking information speaks only as of the date on which it is made and, except as may be required by applicable securities laws, the Company disclaims any intent or obligation to update any forward-looking information, whether as a result of new information, future events or results or otherwise. Although the Company believes that the assumptions inherent in the forward-looking information are reasonable, forward-looking information is not a guarantee of future performance and accordingly undue reliance should not be put on such information due to the inherent uncertainty therein.

Questions?

info@northfied.biz

Within Corporate Newsroom

Media Contact:

media@northfied.biz

Press contact

PR consultants press@northfied.biz

NOT LEGAL ADVICE. Information made available on this website in any form is for information purposes only. It is not, and should not be taken as, legal advice. You should not rely on, or take or fail to take any action based upon this information. Never disregard professional legal advice or delay in seeking legal advice because of something you have read on this website. Northfield & Associates professionals will be pleased to discuss resolutions to specific legal concerns you may have.

Handling Conflicts of Interest on the Board of a Charity

Handling Conflicts of Interest

Are you involved in decision-making or representing a non-profit organization? This could mean holding the position of executive director or being a member of the board, among others. If that’s the case, it’s crucial to manage conflicts of interest effectively and prioritize the use of the non-profit’s resources towards achieving its mission. Upholding the organization’s best interests should always be your primary responsibility when carrying out tasks on behalf of the non-profit.

Effectively manage conflicts of interest

Identifying conflicts of interest can be a nuanced process, and avoidance may not always be possible. Here are the signs to look for and the actions to take if you come across one.

How to recognize conflicts of interest

A conflict of interest arises when an external observer could question whether your decisions on behalf of the non-profit were influenced by interests other than those of the organization. This encompasses situations where your personal interests or those of individuals you have a connection with, such as a spouse, employer, company you own shares in, or another organization you are involved with, could potentially sway your actions.

For instance, let’s consider a scenario where a non-profit’s board needs to purchase insurance for the organization. One of the directors on the board serves as an insurance advisor. If the non-profit chooses to buy insurance through this director, the director will receive a commission, thereby creating a conflict of interest.

While it’s advisable to avoid conflicts of interest, it may not always be feasible. In such cases, you must take the required actions to address the conflict of interest.

Steps directors must take when faced with a conflict of interest

Directors of Canadian non-profit organizations are required to promptly inform their fellow directors about any potential conflicts of interest they may have.

During the first board meeting, directors must disclose any interests they hold in another business or organization that could potentially conflict with the non-profit’s interests. If a new conflict of interest arises subsequently, it must be disclosed at the next board meeting.

If a director intends to enter into an agreement with the non-profit, specific rules must be followed. For instance, if a director wishes to purchase a property that the non-profit is selling, a conflict of interest arises. In such cases, the other directors must evaluate the offer’s alignment with the organization’s interests, and the conflicted director cannot take part in the discussion or vote on the matter.