Marriage is the process by which two people make their relationship public, official and permanent. It is the joining of two people in a bond that putatively lasts until death, but in practice is often cut short by separation or divorce.

If prior to getting married or living with someone, you did not have a Prenuptial Agreement, then it would be wise that when the relationship has broken down and you both go your separate ways, that you draft a Separation Agreement. This blog will explain what a Separation Agreement is, why is it important, what can be included in the Agreement and why you need it.

A Separation Agreement essentially is a contract where you identify the terms that you and your partner want to agree on.

The most important items that would be included in a Separation Agreement would be property and custody of children. If you own a home, then as per the Family Law rules, the home is to be split 50/50. If children are involved in the marriage or cohabitation it is very important to lay out the parenting schedule, who’s going to have primary custody or is it going to be a shared custody between both parents.

Other items to consider would be common assets and spousal support. Some assets have a lot of value and sometimes couples want to make sure that they share the value or one may want to buy the other person out. With regards to spousal support, both spouses and common law partners’ income are looked at in order to determine if there are any other Financial Entitlements.

Prior to drafting a Separation Agreement and starting negotiations, all finances need to be disclosed including bank accounts, loans, debts, lines of credit and notice of assessment for 3 years. It is also important that both partners disclose the same type of documentation so that your lawyer understands what they’re getting into prior to negotiations.

Depending on the facts of the case or circumstances of each client there are other things that need to be discussed and included in the Separation Agreement. What is very important to remember that most people often overlook, is that even though you and your partner separate amicably and you don’t want to get the courts and lawyers involved, it’s always a good idea to have a Separation Agreement which includes everything, so that you are covered for the future. As time goes on, people change, the amicable breakup may change as well, so it is very important that you have an agreement that you are both happy with and you can always go back to reference should a dispute ever arise.

When it comes to drafting a Separation Agreement it may take a while if things are not very straightforward. This depends on many factors including: the years of the relationship, if it has been a long marriage or if it has been a long cohabitation, assets, are children involved, is there some friction between both partners in terms of who has the children, who gets what and how much will be given in child or spousal support.

With this, comes a lot of correspondence between lawyers. When you hire a lawyer to prepare a Separation Agreement you will be advised as to everything you are entitled to. Be prepared to tell your relationship story in full detail so that you will receive the proper advice that you deserve. Keep in mind that your partner is most likely doing the same in return so there will be a lot of back and forth until a common understanding and a common Separation Agreement is reached. During this process you might get a little bit frustrated, but you have to understand that everything you agree to will be put in writing so it’s very important that you agree with all of the clauses before signing the Separation Agreement.

There will be occasions that one partner may choose to go it alone and not have a lawyer involved. It is required by the other partners’ lawyer to advise them that prior to signing the Separation Agreement, the partner that does not have a lawyer must have at least received independent legal advice just so that they know exactly what it is they are signing.

Filing for Divorce or Separation, Custody & Access, Child Support, Division of Assets?

We Can Help.

Sponsoring a spouse is both a deeply personal commitment and a complex legal process. Understanding eligibility requirements, preparing the correct documentation, and avoiding common pitfalls are essential to a successful application.

At Northfield & Associates, our experienced immigration consultants and lawyers specialize in spousal sponsorship. We provide strategic advice and tailored support to help you navigate the process with clarity and confidence.

Whether you prefer to meet in person at one of our offices or connect remotely, we make consultations convenient and accessible. During your session, we’ll assess your situation, review your documents, and guide you through each step of the sponsorship process.

In this evolving economic landscape, collaboration with our firm offers clients a strategic advantage. With Cambodia’s reform-driven investment environment and Canada’s expanding footprint in Southeast Asia, our team of experienced consultants and legal advisors provides tailored guidance to help businesses navigate cross-border opportunities. We specialize in developing comprehensive legal strategies, structuring international partnerships, and ensuring compliance in emerging markets.

By leveraging our regional insight and international expertise, you benefit from a trusted partner dedicated to helping you capitalize on growth potential in Cambodia and beyond.

Your Trusted Partner in International Bilateral Relations

At Northfield & Associates, we specialize in Foreign Direct Investment (FDI), international trade missions, and cross-border legal strategy. Our team of experienced consultants and legal advisors offers tailored guidance and strategic insight to help you navigate the complexities of international partnerships and development opportunities.

Whether you choose to meet in person at one of our offices or connect virtually, we provide flexible and accessible consultation options. During your session, we’ll assess your goals, review key documentation, and guide you through every stage of your FDI or trade mission engagement.

Let us help you take the next step with confidence supported by trusted legal and strategic counsel every step of the way.

Northfield & Associates

Advancing Global Partnerships, Together.

Take the First Step Today

If you believe you may be eligible for legal relief or simply need sound legal advice, we’re here to help. Contact us today to book your consultation. Let us provide the clarity, strategy, and peace of mind you need to move forward.

Disclaimer: The information contained in this article is provided for general information purposes only and does not constitute legal or other professional advice. Readers should seek tailored legal advice in relation to their personal circumstances.

We serve our clients in English, Cambodian, Vietnamese, Mandarin and Cantonese, especially in Asian clients.

If you or anybody that you know, think that you meet the requirements and wish to receive further information.

We can help you start the application process and confirm eligibility requirements to participate.

We Offer Consultations & Meetings by Phone & Virtually. Affordable Fees.

Book a Consultation Today

Contact Northfield & Associates today to schedule a consultation with an experienced Consultant.

Northfield & Associates International Corporation is a global strategic advisory and consulting firm partnering with private equity, sovereign, and institutional investors to deploy capital, manage regulatory, supporting senior leadership, boards, and capital providers across Cambodia, Canada, and international markets operating in complex regulatory, economic, and geopolitical environments, and drive enterprise value creation across complex global markets.

We advise boards, executives, entrepreneurs, and public-sector decision-makers on business strategy, institutional transformation, and high-stakes market challenges requiring disciplined judgment, capital efficiency, and execution certainty. Our work is concentrated across priority global sectors, including agribusiness, aviation and automotive, energy and natural resources, financial services, healthcare, infrastructure, real estate, immigration, education, and information technology.

Our platform integrates sector-specific intelligence with multidisciplinary advisory capabilities. Clients benefit from coordinated access to consulting, legal and regulatory counsel, financial management, risk assessment, real estate advisory, immigration, education, and technology expertise. This integrated model supports informed capital allocation, regulatory-compliant investment structuring, and execution-ready strategies designed to optimise returns, preserve downside protection, and enhance risk-adjusted performance.

Northfield combines consulting rigor with legal and regulatory judgment to support capital markets-aligned decision-making in complex, regulated, and rapidly evolving environments. We partner with private enterprises, institutional investors, family offices, and public-sector entities to structure, deploy, and manage capital effectively; strengthen governance; mitigate regulatory and geopolitical risk; and drive sustainable enterprise value creation.

Our engagements span strategy formulation, operational optimisation, organisational design, and change execution. We deliver measurable outcomes that improve financial performance, support disciplined growth, enhance valuation, and generate durable returns on investment for investors, shareholders, and institutional stakeholders. We operate with independence, precision, and accountability, aligned with long-term value creation and fiduciary standards.

Forward-Looking Information

This news release contains forward-looking information. All statements, other than statements of historic fact, that address activities, events or developments that the Company believes, expects or anticipates will or may occur in the future constitute forward-looking information.

This forward-looking information reflects the current expectations or beliefs of the Company based on information currently available to the Company.

Forward-looking information is subject to a number of risks and uncertainties that may cause the actual results of the Company to differ materially from those discussed in the forward-looking information, and even if such actual results are realized or substantially realized, there can be no assurance that they will have the expected consequences to, or effects on the Company. Factors that could cause actual results or events to differ materially from current expectations include, among other things: the failure to finalize negotiations concerning the increase of the Loan or to close such transaction and the failure of the Company to complete the acquisition of the Company Facility; operating performance of facilities; environmental and safety risks; delays in obtaining or failure to obtain necessary permits and approvals from government authorities; unavailability of plant, equipment or labour; inability to retain key management and personnel; changes to regulations or policies affecting the Company’s activities; and the other risks disclosed under the heading “Risk Factors” and elsewhere in the Company’s amended annual information.

Forward-looking information speaks only as of the date on which it is made and, except as may be required by applicable securities laws, the Company disclaims any intent or obligation to update any forward-looking information, whether as a result of new information, future events or results or otherwise. Although the Company believes that the assumptions inherent in the forward-looking information are reasonable, forward-looking information is not a guarantee of future performance and accordingly undue reliance should not be put on such information due to the inherent uncertainty therein.

Questions?

info@northfied.biz

Within Corporate Newsroom

Media Contact:

media@northfied.biz

Press contact

PR consultants press@northfied.biz

NOT LEGAL ADVICE. Information made available on this website in any form is for information purposes only. It is not, and should not be taken as, legal advice. You should not rely on, or take or fail to take any action based upon this information. Never disregard professional legal advice or delay in seeking legal advice because of something you have read on this website. Northfield & Associates professionals will be pleased to discuss resolutions to specific legal concerns you may have.

Membership dues are a crucial aspect of not-for-profit corporations. According to Ontario’s Not-for-Profit Corporations Act (ONCA), Section 86 allows directors to establish and manage annual contributions or dues, subject to the company’s articles and by-laws. It means that directors have the flexibility to determine the amount of contributions and how they are collected.

In addition, aligning membership dues with an organization’s articles and by-laws is essential as it guides directors in establishing fair and reasonable dues. ONCA allows directors to decide the annual contribution amount and how it will be paid. This will enable organizations to tailor dues structures to their unique needs and members’ preferences. Clear communication about the rationale behind the dues, the benefits members receive, and the impact on the organization’s objectives fosters trust and understanding among members.

To stay in line with ONCA regulations, organizations should meticulously create and routinely assess their articles and by-laws, taking a proactive stance to avoid conflicts and guaranteeing that the legal structure oversees membership dues as outlined in ONCA’s Section 86; these dues serve as a means for financial sustainability for not-for-profit corporations.

At Northfield & Associates our expert teams guidance on compliance requirements. Our team understands Canadian charity law and can help ensure your organisation follows proper procedures.

At Northfield & Associates, we have a team of professional bookkeepers and accountants to help your organization manage the books so that you can breeze through tax season.

We’re often asked by prospective clients what our Bookkeeping Service covers? People want to know what specific tasks we do, and what their responsibility is. This brief explainer page will answer that question. This is by no means an exhaustive list, but covers the most frequently asked questions.

Getting Started

Review your existing books for needed corrections or back-work

Chart of accounts setup or amendment

Assistance with setting up bank feeds

Limited assistance* with setting up payroll (QBO or Gusto only)

Your books brought current and reconciled if needed

Ongoing Monthly Bookkeeping

After-the-fact transaction recording

Post to general ledger

Post to other ledgers (as needed)

Bank account reconciliation

Monthly financial statements

Other bookkeeping services, as required

Best-practice bookkeeping advice and counsel

Year End

Assistance with 1099-NEC preparation*

Assistance with 1099-MISC preparation*

Year-end financial statements and period-end closing

What We Don’t Do

Pay bills

We do not offer bill-pay services at this time, nor do we manage Accounts Payable (AP) or Accounts Receivable (AR).

Payroll tax responsibility

Our bookkeepers can assist you in setting up your initial payroll service in QBO or Gusto. We are not responsible for entering payroll hours/salary, accruing payroll taxes, nor the transmittal of payroll taxes to the IRS or the state. Your full-service payroll provider (QBO, Gusto, or whatever other service a client uses) will be the responsible party for payroll and payroll tax compliance.

*Payroll deductions and benefits

We provide assistance with setting up a payroll account in either Quickbooks Online or Gusto, including entry of employee data. We do not assist in state registrations, benefits, or advise on deductions. Those service areas are provided directly by either QBO or Gusto.

Preparation of W2s

Similar to the last item, your full-service payroll provider (QBO/Gusto) is responsible for preparation of Form W2 for employees.

Sales tax reporting

For those nonprofits that sell taxable goods and/or services, your bookkeeper will assist in accounting for sales taxes collected and transmitted, but we do not prepare state sales tax reports.

Donation recording

We do not provide individual donation data entry into your neither your donor CRM nor Quickbooks Online, nor do we prepare year-end donor acknowledgements.

Administrative tasks

We cannot provide administrative services unrelated to our bookkeeping function.

Attend board meetings

Due to the constraints of time and distance, we are unable to be present, physically nor virtually, at a meeting of a client’s board of directors.*May incur additional fee per 1099-NEC or 1099-MISC.

Let’s Collaborate & Make a Difference!

Partner with us to amplify your mission. Whether it’s Charity accounting, financial transparency, or strategic growth—we’re here to help you create meaningful impact. Let’s work together to build a better future!

In this evolving economic landscape, collaboration with our firm offers clients a strategic advantage. With Cambodia’s reform-driven investment environment and Canada’s expanding footprint in Southeast Asia, our team of experienced consultants and legal advisors provides tailored guidance to help businesses navigate cross-border opportunities. We focus in developing comprehensive legal strategies, structuring international partnerships, and ensuring compliance in emerging markets.

By leveraging our regional insight and international expertise, you benefit from a trusted partner dedicated to helping you capitalize on growth potential in Cambodia and beyond.

Your Trusted Partner in International Bilateral Relations

At Northfield & Associates are focus in Foreign Direct Investment (FDI), international trade missions, and cross-border legal strategy. Our team of experienced consultants and legal advisors offers tailored guidance and strategic insight to help you navigate the complexities of international partnerships and development opportunities.

Whether you choose to meet in person at one of our offices or connect virtually, we provide flexible and accessible consultation options. During your session, we’ll assess your goals, review key documentation, and guide you through every stage of your FDI or trade mission engagement.

Let us help you take the next step with confidence supported by trusted legal and strategic counsel every step of the way.

Northfield & Associates

Advancing Global Partnerships, Together.

Take the First Step Today

If you believe you may be eligible for legal relief or simply need sound legal advice, we’re here to help. Contact us today to book your consultation. Let us provide the clarity, strategy, and peace of mind you need to move forward.

Disclaimer: The information contained in this article is provided for general information purposes only and does not constitute legal or other professional advice. Readers should seek tailored legal advice in relation to their personal circumstances.

We serve our clients in English, Cambodian, Vietnamese, Mandarin and Cantonese, especially in Asian clients.

If you or anybody that you know, think that you meet the requirements and wish to receive further information.

We can help you start the application process and confirm eligibility requirements to participate.

We Offer Consultations & Meetings by Phone & Virtually. Affordable Fees.

Book a Consultation Today

Contact Northfield & Associates today to schedule a consultation with an experienced Consultant.

Northfield & Associates International Corporation is a global consulting firm serving private enterprises, public institutions, not-for-profit organizations, and institutional capital providers. Operating across Cambodia, Canada, and global markets, the firm supports capital deployment, regulatory navigation, and enterprise decision-making in complex economic and geopolitical environments. Northfield & Associates delivers customized, execution-focused advisory solutions that drive measurable transformation, strengthen competitiveness, and enhance long-term highest value opportunities. The firm incorporates consulting, legal, regulatory, financial, and risk expertise to enable disciplined capital allocation, strong governance, and operational resilience. Northfield & Associates upholds a culture of applied insight and innovation, supporting clients across digital transformation, growth strategy, and organizational capability building. The firm advises individual, leading global corporations, midsize enterprises, government agencies, and mission-driven organizations through long-term partnerships. Enterprise-wide risk management, professional ethics, and fiduciary standards are embedded across all operations. Northfield & Associates’ diverse, globally unified teams are committed to execution certainty and sustainable, risk-adjusted returns aligned with ESG and stakeholder objectives.

Forward-Looking Information

This news release contains forward-looking information. All statements, other than statements of historic fact, that address activities, events or developments that the Company believes, expects or anticipates will or may occur in the future constitute forward-looking information.

This forward-looking information reflects the current expectations or beliefs of the Company based on information currently available to the Company.

Forward-looking information is subject to a number of risks and uncertainties that may cause the actual results of the Company to differ materially from those discussed in the forward-looking information, and even if such actual results are realized or substantially realized, there can be no assurance that they will have the expected consequences to, or effects on the Company. Factors that could cause actual results or events to differ materially from current expectations include, among other things: the failure to finalize negotiations concerning the increase of the Loan or to close such transaction and the failure of the Company to complete the acquisition of the Company Facility; operating performance of facilities; environmental and safety risks; delays in obtaining or failure to obtain necessary permits and approvals from government authorities; unavailability of plant, equipment or labour; inability to retain key management and personnel; changes to regulations or policies affecting the Company’s activities; and the other risks disclosed under the heading “Risk Factors” and elsewhere in the Company’s amended annual information.

Forward-looking information speaks only as of the date on which it is made and, except as may be required by applicable securities laws, the Company disclaims any intent or obligation to update any forward-looking information, whether as a result of new information, future events or results or otherwise. Although the Company believes that the assumptions inherent in the forward-looking information are reasonable, forward-looking information is not a guarantee of future performance and accordingly undue reliance should not be put on such information due to the inherent uncertainty therein.

Questions?

info@northfied.biz

Within Corporate Newsroom

Media Contact:

media@northfied.biz

Press contact

PR consultants press@northfied.biz

NOT LEGAL ADVICE. Information made available on this website in any form is for information purposes only. It is not, and should not be taken as, legal advice. You should not rely on, or take or fail to take any action based upon this information. Never disregard professional legal advice or delay in seeking legal advice because of something you have read on this website. Northfield & Associates professionals will be pleased to discuss resolutions to specific legal concerns you may have.

How Can Canadian Charities Manage Their CRA Business Account?

For any registered charity in Canada, managing your business account with the Canada Revenue Agency (CRA) is key to staying compliant and ensuring smooth operations. The CRA business account is where you handle important tasks like filing annual returns, updating key information, and fulfilling legal obligations. But how do members, directors, officers, and volunteers get access to this account, and what responsibilities come with it? Let’s walk through the process in clear terms.

What is a CRA Business Account?

Every registered charity in Canada needs to manage its activities with the CRA through what’s known as a CRA business account. This account isn’t just for businesses—registered charities use it to file annual returns, make changes to organizational details, and ensure compliance with the CRA’s rules and regulations.

Why Does Your Charity Need a CRA Business Account?

A CRA business account serves multiple purposes, and it’s important for several reasons:

Filing Returns: Registered charities must submit their T3010 form annually. This lets the CRA review the charity’s operations and financial status, ensuring it continues to meet its obligations.

Updating Key Information: Charities need to notify the CRA when significant changes occur, such as appointing new directors or officers, changing addresses, or revising charitable activities.

Maintaining Compliance: Staying on top of updates and filings through the CRA business account helps charities avoid penalties or the risk of losing their charitable registration.

Steps to Access Your Charity’s CRA Business Account

Let’s look at how members, directors, officers, and even volunteers can access a charity’s CRA business account.

Step 1: Set Up a Personal My Business Account

Before accessing your charity’s business account, you’ll need to set up your own My Business Account with the CRA:

Go to the CRA website: On the CRA’s homepage, find the option to sign in to “My Business Account.”

Sign in: You can either log in using a CRA user ID and password or use a partner login, such as through your bank.

Set up security: After logging in, you’ll need to answer some security questions to verify your identity. This ensures your account is secure and protected.

Request access to the charity’s business account: Once you’ve set up your My Business Account, you’ll need to link it to the charity’s business number to gain access.

Step 2: Authorization Process

For members, directors, officers, or volunteers to access the charity’s account, they must be authorized by the charity itself. Here’s how that works:

Authorization by the Charity: A person with the proper authority, usually a director, must formally authorize others by using the CRA’s online services. This gives the authorized individual access to the charity’s business account.

Access as an Authorized Representative: After being authorized, the individual can log in to the charity’s CRA business account and manage its financial and tax matters.

Step 3: What You Can Do as an Authorized Representative

Once you’re authorized to manage the charity’s CRA business account, here are some of the key tasks you’ll be responsible for:

View Financial Information: Check the charity’s records and financial data.

File Returns and Forms: Complete and submit required filings, such as the annual T3010 form.

Update Charity Information: Make changes to the charity’s directors, address, or other details as needed.

Responsibilities of Members, Directors, Officers, and Volunteers with access comes responsibility. Members, directors, officers, and volunteers need to ensure they handle the CRA business account with care:

Legal Responsibility: Directors and officers have a legal duty to ensure the charity complies with CRA regulations. If the charity is found to be non-compliant, they could be held personally liable.

Accurate Record Keeping: It’s important to keep thorough records of all submissions and updates to ensure the charity remains transparent and accountable.

Regular Monitoring: Access the CRA business account regularly to stay on top of deadlines and ensure the charity’s information is always up to date.

What Happens If You Don’t Keep Up with CRA Requirements?

Failing to manage the CRA business account can lead to serious consequences:

Loss of Charitable Status: If the charity doesn’t file its annual returns or keep its information updated, the CRA can revoke its charitable registration. This would mean losing the ability to issue donation receipts, which is a major blow for fundraising.

Financial Penalties: Non-compliance can result in fines or penalties, putting additional financial strain on the charity.

Damage to Reputation: A charity that fails to meet CRA requirements could lose the trust of donors, sponsors, and the community, which can be difficult to rebuild.

Conclusion

Managing your charity’s CRA business account is a key part of staying compliant with Canadian laws. Members, directors, officers, and volunteers must understand their responsibilities and take the necessary steps to keep the charity in good standing. From filing returns to updating information, regular monitoring of the account will ensure the charity avoids penalties and continues its important work.

By taking these steps, your charity can continue to operate smoothly and fulfill its mission without unnecessary obstacles.

Get Expert Help with Your CRA Business Account

At Northfield & Associates, we help Canadian charities navigate CRA compliance complexities with confidence. Our experienced team provides guidance on account management procedures, regulatory requirements, and issue resolution to protect your organization’s mission and charitable status.

Don’t let CRA compliance challenges threaten your charity’s future.

to discuss your specific circumstances and receive expert assistance throughout the reinstatement process with our experienced legal team.

Frequently Asked Questions

Managing your charity’s CRA business account involves understanding complex regulations, filing requirements, and compliance obligations. These frequently asked questions address the most common concerns Canadian charities face when dealing with the Canada Revenue Agency, from registration numbers and reporting requirements to record-keeping and potential sanctions.

What is a CRA registration number?

A CRA registration number is a unique identifier assigned to registered charities by the Canada Revenue Agency. It typically starts with the digits 10001 and is followed by four additional digits. Charities must include this number on all official donation receipts and use it when filing returns or communicating with the CRA.

What are the sanctions of charities in CRA?

The CRA can impose various sanctions on non-compliant charities including monetary penalties, suspension of receipting privileges, compliance agreements, and complete revocation of charitable status. Minor violations may result in education letters or penalties, while serious issues like misuse of funds can lead to immediate revocation and loss of tax-exempt status.

What are the charity tax rules in Canada?

Canadian charities are exempt from income tax but must follow strict rules. They must spend at least 3.5% of assets annually on charitable activities, cannot engage in prohibited political activities, must issue proper donation receipts, and cannot provide undue private benefits. Charities must also maintain proper books and records and file annual returns.

Can a charity own a for-profit business in Canada?

Yes, but with restrictions. Charities can own for-profit businesses if the business furthers the charity’s purposes or if profits support charitable activities. However, operating unrelated businesses can jeopardize charitable status. The CRA evaluates each situation based on factors like the business’s connection to charitable purposes and the time spent on commercial activities.

What are the requirements for charity reporting in Canada?

Registered charities must file annual T3010 returns within six months of their fiscal year-end. The return includes detailed financial information, program descriptions, governance details, and compensation data. Larger charities may need audited financial statements, while smaller ones need review engagements or compiled statements depending on their revenue.

How long do charities need to keep financial records in Canada?

Canadian charities must keep books and records for at least six years after the end of the fiscal year they relate to. This includes receipts, invoices, bank statements, donation records, board minutes, and all supporting documentation. The CRA can request these records during audits or compliance reviews.

Do Canadian charities file tax returns?

Yes, registered charities must file annual T3010 Registered Charity Information Returns even though they’re tax-exempt. This return provides the CRA with detailed information about the charity’s finances, activities, and governance. Failure to file can result in penalties and eventual loss of charitable status.

At Northfield & Associates our expert teams guidance on compliance requirements. Our team understands Canadian charity law and can help ensure your organisation follows proper procedures.

In this evolving economic landscape, collaboration with our firm offers clients a strategic advantage. With Cambodia’s reform-driven investment environment and Canada’s expanding footprint in Southeast Asia, our team of experienced consultants and legal advisors provides tailored guidance to help businesses navigate cross-border opportunities. We focus in developing comprehensive legal strategies, structuring international partnerships, and ensuring compliance in emerging markets.

By leveraging our regional insight and international expertise, you benefit from a trusted partner dedicated to helping you capitalize on growth potential in Cambodia and beyond.

Book a Consultation with Northfield & Associates

Your Trusted Partner in International Bilateral Relations

At Northfield & Associates are focus in Foreign Direct Investment (FDI), international trade missions, and cross-border legal strategy. Our team of experienced consultants and legal advisors offers tailored guidance and strategic insight to help you navigate the complexities of international partnerships and development opportunities.

Whether you choose to meet in person at one of our offices or connect virtually, we provide flexible and accessible consultation options. During your session, we’ll assess your goals, review key documentation, and guide you through every stage of your FDI or trade mission engagement.

Let us help you take the next step with confidence supported by trusted legal and strategic counsel every step of the way.

Take the First Step Today

If you believe you may be eligible for legal relief or simply need sound legal advice, we’re here to help. Contact us today to book your consultation. Let us provide the clarity, strategy, and peace of mind you need to move forward.

We serve our clients in English, Cambodian, Vietnamese, Mandarin and Cantonese, especially in Asian clients.

If you or anybody that you know, think that you meet the requirements and wish to receive further information.

We can help you start the application process and confirm eligibility requirements to participate.

We Offer Consultations & Meetings by Phone & Virtually. Affordable Fees.

Disclaimer:

The information contained in this article is provided for general information purposes only and does not constitute legal or other professional advice. Readers should seek tailored legal advice in relation to their personal circumstances.

Northfield & Associates International Corporation is a global consulting firm serving private enterprises, public institutions, not-for-profit organizations, and institutional capital providers. Operating across Cambodia, Canada, and global markets, the firm supports capital deployment, regulatory navigation, and enterprise decision-making in complex economic and geopolitical environments. Northfield & Associates delivers customized, execution-focused advisory solutions that drive measurable transformation, strengthen competitiveness, and enhance long-term highest value opportunities. The firm incorporates consulting, legal, regulatory, financial, and risk expertise to enable disciplined capital allocation, strong governance, and operational resilience. Northfield & Associates upholds a culture of applied insight and innovation, supporting clients across digital transformation, growth strategy, and organizational capability building. The firm advises individual, leading global corporations, midsize enterprises, government agencies, and mission-driven organizations through long-term partnerships. Enterprise-wide risk management, professional ethics, and fiduciary standards are embedded across all operations. Northfield & Associates’ diverse, globally unified teams are committed to execution certainty and sustainable, risk-adjusted returns aligned with ESG and stakeholder objectives.

Forward-Looking Information

This news release contains forward-looking information. All statements, other than statements of historic fact, that address activities, events or developments that the Company believes, expects or anticipates will or may occur in the future constitute forward-looking information.

This forward-looking information reflects the current expectations or beliefs of the Company based on information currently available to the Company.

Forward-looking information is subject to a number of risks and uncertainties that may cause the actual results of the Company to differ materially from those discussed in the forward-looking information, and even if such actual results are realized or substantially realized, there can be no assurance that they will have the expected consequences to, or effects on the Company. Factors that could cause actual results or events to differ materially from current expectations include, among other things: the failure to finalize negotiations concerning the increase of the Loan or to close such transaction and the failure of the Company to complete the acquisition of the Company Facility; operating performance of facilities; environmental and safety risks; delays in obtaining or failure to obtain necessary permits and approvals from government authorities; unavailability of plant, equipment or labour; inability to retain key management and personnel; changes to regulations or policies affecting the Company’s activities; and the other risks disclosed under the heading “Risk Factors” and elsewhere in the Company’s amended annual information.

Forward-looking information speaks only as of the date on which it is made and, except as may be required by applicable securities laws, the Company disclaims any intent or obligation to update any forward-looking information, whether as a result of new information, future events or results or otherwise. Although the Company believes that the assumptions inherent in the forward-looking information are reasonable, forward-looking information is not a guarantee of future performance and accordingly undue reliance should not be put on such information due to the inherent uncertainty therein.

Questions?

info@northfied.biz

Within Corporate Newsroom

Media Contact:

media@northfied.biz

Press contact

PR consultants press@northfied.biz

NOT LEGAL ADVICE. Information made available on this website in any form is for information purposes only. It is not, and should not be taken as, legal advice. You should not rely on, or take or fail to take any action based upon this information. Never disregard professional legal advice or delay in seeking legal advice because of something you have read on this website. Northfield & Associates professionals will be pleased to discuss resolutions to specific legal concerns you may have.

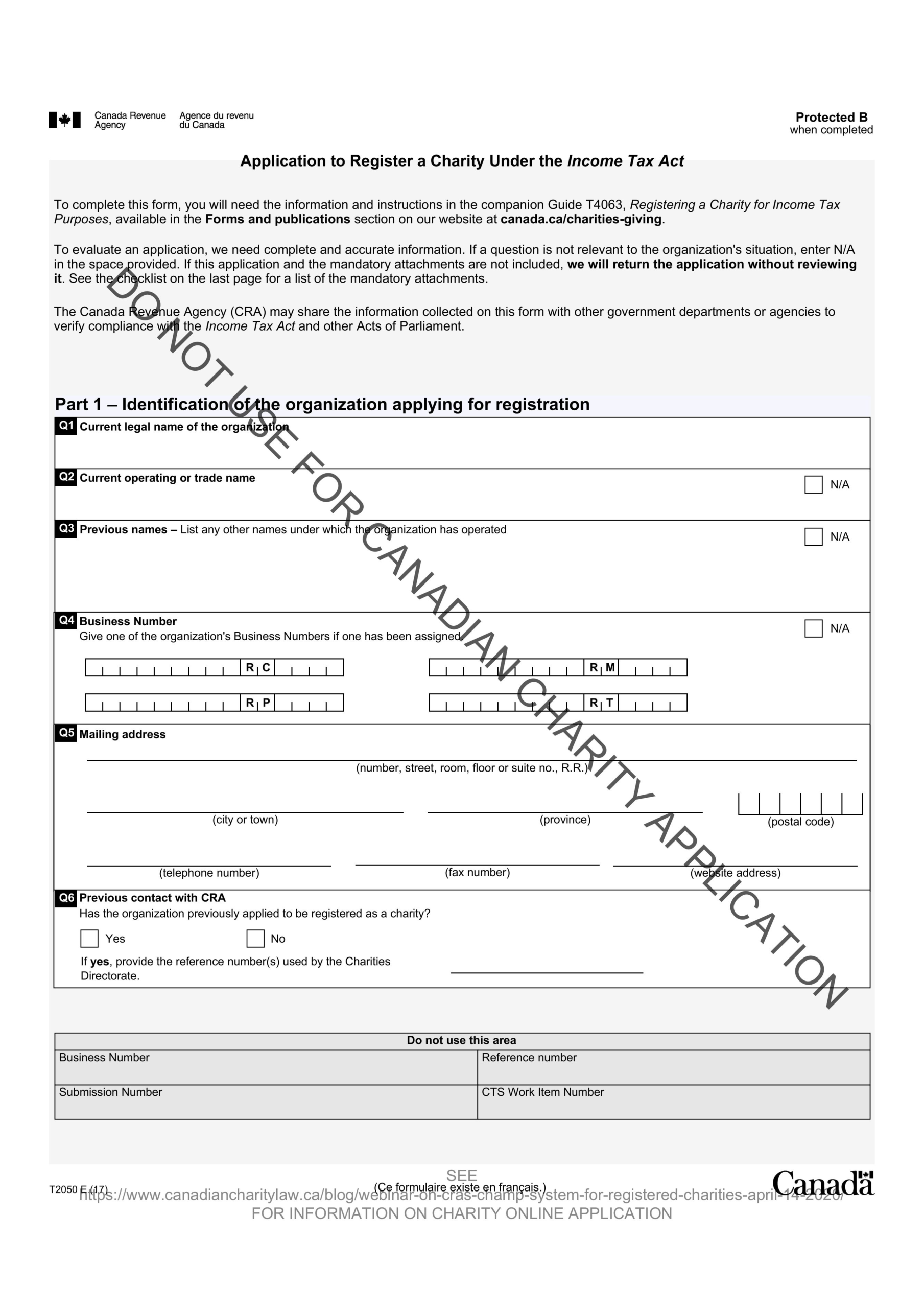

Don’t Use the Form T2050 To Register a Charity In Canada: It is No Longer Accepted by the CRA

Understanding the process to register a charity in Canada is crucial for any organization aiming to make a significant social impact.

It’s important to note that the Canada Revenue Agency (CRA) has transitioned to a primarily online application system. The previously used T2050 form is no longer accepted by the CRA.

We’ve heard anecdotally from CRA examiners that four years after the form has been discontinued, it continues to receive tens of applications to register a Canadian charity using form T2050 every year, including from accountants and law firms!

While a paper application is still available upon request for those with extenuating circumstances, be aware that these applications face significantly longer processing times. The CRA actively encourages all applicants to utilize the online system.

It’s vital to recognize that applying to register a charity in Canada is a far more intricate process than obtaining a standard business number or license. The CRA requires extensive documentation and information to assess an organization’s eligibility.

Furthermore, becoming a registered charity entails substantial ongoing compliance obligations. Organizations must be prepared to adhere to stringent regulations and reporting requirements.

Professional Assistance:

Many organizations seek professional legal assistance to navigate the complexities of the CRA Charity Registration application process. Experienced Charity Lawyers can provide valuable guidance and support, ensuring a smoother and more efficient application experience. With about 50% of all charity applications being rejected annually by the CRA – Charities Directorate, the ROI of using an experienced Charity Consulting Firm, such as Northfield & Associates, is invaluable.

By understanding the updated online application process and the associated compliance requirements, organizations can better prepare to register a charity or Foundation in Canada and maximize their positive impact.

If you are looking to register your charity using the CRA’s mandated online portal and need assistance, contact our charity registration legal team.

At Northfield & Associates our expert teams guidance on compliance requirements. Our team understands Canadian charity law and can help ensure your organisation follows proper procedures.

In this evolving economic landscape, collaboration with our firm offers clients a strategic advantage. With Cambodia’s reform-driven investment environment and Canada’s expanding footprint in Southeast Asia, our team of experienced consultants and legal advisors provides tailored guidance to help businesses navigate cross-border opportunities. We focus in developing comprehensive legal strategies, structuring international partnerships, and ensuring compliance in emerging markets.

By leveraging our regional insight and international expertise, you benefit from a trusted partner dedicated to helping you capitalize on growth potential in Cambodia and beyond.

Book a Consultation with Northfield & Associates

Your Trusted Partner in International Bilateral Relations

At Northfield & Associates are focus in Foreign Direct Investment (FDI), international trade missions, and cross-border legal strategy. Our team of experienced consultants and legal advisors offers tailored guidance and strategic insight to help you navigate the complexities of international partnerships and development opportunities.

Whether you choose to meet in person at one of our offices or connect virtually, we provide flexible and accessible consultation options. During your session, we’ll assess your goals, review key documentation, and guide you through every stage of your FDI or trade mission engagement.

Let us help you take the next step with confidence supported by trusted legal and strategic counsel every step of the way.

Take the First Step Today

If you believe you may be eligible for legal relief or simply need sound legal advice, we’re here to help. Contact us today to book your consultation. Let us provide the clarity, strategy, and peace of mind you need to move forward.

We serve our clients in English, Cambodian, Vietnamese, Mandarin and Cantonese, especially in Asian clients.

If you or anybody that you know, think that you meet the requirements and wish to receive further information.

We can help you start the application process and confirm eligibility requirements to participate.

We Offer Consultations & Meetings by Phone & Virtually. Affordable Fees.

Disclaimer:

The information contained in this article is provided for general information purposes only and does not constitute legal or other professional advice. Readers should seek tailored legal advice in relation to their personal circumstances.

Northfield & Associates International Corporation is a global consulting firm serving private enterprises, public institutions, not-for-profit organizations, and institutional capital providers. Operating across Cambodia, Canada, and global markets, the firm supports capital deployment, regulatory navigation, and enterprise decision-making in complex economic and geopolitical environments. Northfield & Associates delivers customized, execution-focused advisory solutions that drive measurable transformation, strengthen competitiveness, and enhance long-term highest value opportunities. The firm incorporates consulting, legal, regulatory, financial, and risk expertise to enable disciplined capital allocation, strong governance, and operational resilience. Northfield & Associates upholds a culture of applied insight and innovation, supporting clients across digital transformation, growth strategy, and organizational capability building. The firm advises individual, leading global corporations, midsize enterprises, government agencies, and mission-driven organizations through long-term partnerships. Enterprise-wide risk management, professional ethics, and fiduciary standards are embedded across all operations. Northfield & Associates’ diverse, globally unified teams are committed to execution certainty and sustainable, risk-adjusted returns aligned with ESG and stakeholder objectives.

Forward-Looking Information

This news release contains forward-looking information. All statements, other than statements of historic fact, that address activities, events or developments that the Company believes, expects or anticipates will or may occur in the future constitute forward-looking information.

This forward-looking information reflects the current expectations or beliefs of the Company based on information currently available to the Company.

Forward-looking information is subject to a number of risks and uncertainties that may cause the actual results of the Company to differ materially from those discussed in the forward-looking information, and even if such actual results are realized or substantially realized, there can be no assurance that they will have the expected consequences to, or effects on the Company. Factors that could cause actual results or events to differ materially from current expectations include, among other things: the failure to finalize negotiations concerning the increase of the Loan or to close such transaction and the failure of the Company to complete the acquisition of the Company Facility; operating performance of facilities; environmental and safety risks; delays in obtaining or failure to obtain necessary permits and approvals from government authorities; unavailability of plant, equipment or labour; inability to retain key management and personnel; changes to regulations or policies affecting the Company’s activities; and the other risks disclosed under the heading “Risk Factors” and elsewhere in the Company’s amended annual information.

Forward-looking information speaks only as of the date on which it is made and, except as may be required by applicable securities laws, the Company disclaims any intent or obligation to update any forward-looking information, whether as a result of new information, future events or results or otherwise. Although the Company believes that the assumptions inherent in the forward-looking information are reasonable, forward-looking information is not a guarantee of future performance and accordingly undue reliance should not be put on such information due to the inherent uncertainty therein.

Questions?

info@northfied.biz

Within Corporate Newsroom

Media Contact:

media@northfied.biz

Press contact

PR consultants press@northfied.biz

NOT LEGAL ADVICE. Information made available on this website in any form is for information purposes only. It is not, and should not be taken as, legal advice. You should not rely on, or take or fail to take any action based upon this information. Never disregard professional legal advice or delay in seeking legal advice because of something you have read on this website. Northfield & Associates professionals will be pleased to discuss resolutions to specific legal concerns you may have.

Why the CRA Ghosted Your Private Foundation Application (And How to Win Them Back)

So, you’ve done well for yourself. Maybe you sold your business, your investments paid off handsomely, or you finally convinced your wealthy aunt that you were her favorite nephew. Whatever the reason, you’ve decided to join the ranks of philanthropic elite by starting your own private foundation in Canada. You’ve imagined the press releases, the galas, maybe even a building with your name on it.

Then you got the letter.

The Canada Revenue Agency—those delightful folks who live to audit your receipts and question your home office claims—has rejected your application. Welcome to the club nobody wants to join. Let’s talk about why this happened and, more importantly, how to avoid becoming a cautionary tale at your lawyer’s office.

You Thought This Was Going to Be Easy (Spoiler: It’s Not)

Embed this infographic on your site:

Here’s the thing about starting a private foundation: it’s not like opening a lemonade stand. You can’t just slap together some paperwork, declare yourself a philanthropist, and start issuing tax receipts to your golf buddies.

The CRA application process can take anywhere from two months for “simple” applications to six months or more for “regular” ones. And trust me, if you’re reading this article because your application was rejected, yours definitely fell into the “regular” category—or worse, the “what were they thinking?” category.

Reason #1: You Confused “Private Foundation” with “Private Piggy Bank”

Let’s start with the most common misconception. Remember that businessman from our sources who, standing at his dying brother’s bedside, realized you can’t take your wealth with you? Well, he also learned you can’t use a private foundation as a personal ATM.

Once you donate property to a private foundation, it’s gone. Forever. You cannot retrieve it. Not for emergencies. Not for “just this once.” Not because you promised your kid you’d help with their down payment and forgot about it.

The CRA has seen it all: people trying to move money in and out of foundations for non-charitable purposes, treating the foundation like a flexible savings account with better tax benefits. This is explicitly prohibited, and attempting it is a fast track to rejection—or worse, revocation of charitable status if you somehow sneak through.

Real-life example: Imagine Uncle Bob sets up his foundation, donates $500,000, and then six months later decides he actually needs that money for his vacation property in Muskoka. Too bad, Uncle Bob. That money now belongs to charity. The CRA doesn’t care that your real estate agent assured you the cottage was a “can’t-miss opportunity.”

Reason #2: Your “Charitable Purpose” Was More “Vague Purpose”

To get CRA approval, you need defined charitable objectives. “Doing good things” doesn’t cut it. Neither does “helping people” or “making the world better” or any other fortune cookie philosophy you pulled from your vision board.

The CRA recognizes four charitable purposes: relief of poverty, advancement of education, advancement of religion, and other purposes beneficial to the community. Your application needs to clearly articulate which category you’re targeting and how you plan to achieve your goals.

What went wrong: You probably wrote something like “We want to support great causes in our community and help those in need.” The CRA read that and thought, “Cool story. Which causes? Which needs? How will you determine who to help? What’s your criteria?”

What you should have done: Be specific. Instead of “supporting education,” try “providing scholarships to low-income students pursuing STEM degrees at accredited Canadian universities.” See the difference? One sounds like a beauty pageant answer; the other sounds like a plan.

Reason #3: You Tried to Sneak in Private Company Shares (and Got Caught)

Oh boy. This is where things get spicy.

Remember that 2007 federal budget that made everyone excited because you could now donate listed securities without capital gains? Well, the government giveth, and the government also created the Excess Corporate Holdings Regime for Private Foundations.

Here’s the deal: if your foundation owns more than 2% of any share class of a private company, you enter what’s called the “Monitoring” range. Own more than 20%? Welcome to the “Divestment” range, where you have specific time frames to reduce your holdings or face penalties that would make a tax accountant weep.

The horror story: You donated 30% of your private company shares to your new foundation, thinking you were being generous. The CRA looked at this and saw a potential tax avoidance scheme. First-offense penalty? Five percent of the fair market value of those shares multiplied by your divestment obligation. Second offense within five years? That jumps to 10%. Fail to file properly? Another 10% penalty.

As one source wisely noted: “Unless there is a specific and immediate plan to redeem the shares caught by this legislation, I strongly suggest that donors not use this type of property in private foundations.” Translation: Don’t even think about it unless you have a rock-solid exit strategy and a lawyer who specializes in making miracles happen.

Reason #4: Your Family Involvement Plan Looked Like a Dynasty

Private foundations can absolutely be family affairs. In fact, the majority of them are. Family members can sit on the board, make decisions together, and create a lasting legacy. It’s actually one of the beautiful things about private foundations—three generations working together to do good.

But here’s where people trip up: they don’t think through the governance structure, conflict-of-interest policies, or succession planning. They create a board that’s 100% blood relatives with no thought to what happens when Uncle Jerry and Aunt Martha stop speaking to each other over that incident at Christmas 2023.

What the CRA saw: A governance structure that looked less like a professional charitable organization and more like a family reunion where someone’s going to end up crying in the bathroom.

What you needed: Clear bylaws. Defined roles. Conflict-of-interest guidelines. Decision-making processes that don’t involve shouting matches. As one third-generation foundation chairman wisely noted: “Set conflict of interest guidelines. Have some policies or a healthy discussion that is recorded for posterity for successive meetings on how personal interests should be dealt with.”

Reason #5: You Underestimated the Money (and Overestimated Your Commitment)

Let’s talk about everyone’s favorite topic: money.

The setup costs: Legal fees for incorporation and CRA registration typically run between $5,000-$15,000, though more complex foundations can cost up to $25,000.

The minimum investment: While there’s technically no minimum amount required to start a foundation, most experts recommend at least $1 million. Why? Because of the disbursement quota.

The disbursement quota: This is the kicker that trips up many applicants. Your foundation must spend 3.5% of its invested assets annually on charitable activities (for those with revenue under $1,000,000). If you start with $100,000, that’s $3,500 per year. After administrative costs (typically 0.75%-1.5% of assets), investment management fees, and other expenses, you’re left with very little for actual grantmaking.

The time commitment: One founder admitted, “I didn’t know entirely what I was getting into when I started. If I hadn’t become so personally involved, I’m not sure I’d be doing today what I’m doing.” Starting a foundation isn’t passive philanthropy. It’s a part-time job at minimum, possibly a full-time one if you’re serious.

Where applications fail: You probably proposed starting a foundation with $250,000, no clear plan for adding capital, vague administrative support, and the assumption that you could run this in your spare time between your day job, coaching Little League, and your standing golf game.

Reason #6: You Got Creative with What Qualifies as “Charitable Activities”

The CRA is very specific about where foundation money can go: registered charities, registered amateur athletic associations, public bodies, and other qualified donees. That’s it. That’s the list.

You cannot:

Fund your buddy’s “totally going to change the world” startup

Support international organizations that aren’t on the CRA’s approved list

Give money directly to individuals in need (even if they really, really need it)

Engage in business activities (private foundations are explicitly prohibited from this, unlike other charities)

The mistake: Your application probably included some well-intentioned but technically ineligible activities. Maybe you wanted to help entrepreneurs in developing countries, fund a community organization that isn’t actually registered as a charity, or support a cause that’s more political than philanthropic.

What you should have done: Before writing your application, you should have verified that every single organization and activity you planned to support meets CRA’s qualified donee requirements. This isn’t the time for creative interpretation.

Reason #7: Your Legal Structure Was Half-Baked

You have two options for structuring your foundation: as a trust or as a corporation. Most people choose incorporation because it provides limited liability and is generally easier to manage. But here’s where things went sideways:

You probably:

Didn’t consult with a lawyer who specializes in charitable law

Used generic incorporation documents that weren’t properly tailored for a charitable organization

Forgot that after incorporation, you still need to register with the CRA as a charity

Didn’t properly establish whether you wanted an inter-vivos trust (operating during your lifetime) or a testamentary trust (established by your will)

The two-step tango: Setting up a private foundation requires two distinct steps. First, create the legal entity (trust or corporation). Second, apply for charitable status with the CRA. You can’t do them simultaneously, and messing up either step means starting over.

Reason #8: Your Application Looked Like You Wrote It During Halftime

The CRA application requires responses to 21 questions. Twenty-one questions that determine whether your foundation receives charitable status and all the tax benefits that come with it.

Looking at rejected applications, it’s clear that some people treated this like a job application for a position they don’t really want. Rushed answers. Vague descriptions. Copy-pasted text from other foundations’ websites. Missing information. Inconsistencies that suggest different people filled out different sections without talking to each other.

Governance structure that would make a corporate lawyer nervous

Activities that might technically violate CRA regulations

How to Actually Get It Right

Alright, enough doom and gloom. Let’s talk about how to avoid rejection and join the successful 5,334 private foundations currently operating in Canada.

1. Start with Soul-Searching, Not Spreadsheets

Before you fill out a single form, ask yourself:

Why do I really want to do this?

What specific problem am I trying to solve?

Am I willing to permanently part with this money?

Do I have the time to be genuinely involved?

How do I want my family involved (if at all)?

What’s my 10-year vision for this foundation?

One co-founder put it perfectly: “I think philanthropy can give meaning to your life. I don’t want to have a lot of regrets when I’m 85, 95. I want to be able to say, you gave back, you made a difference.”

2. Hire Professionals (and Actually Listen to Them)

This is not a DIY project. You need:

A lawyer specializing in charitable law

An accountant familiar with foundation taxation

A financial advisor who understands philanthropic planning

Possibly a consultant on philanthropic strategy

Yes, this will cost money. But it costs far less than having your application rejected and starting over, or worse, having your foundation’s charitable status revoked later because you didn’t understand the rules.

3. Be Boringly Specific

Your mission statement should be so specific that someone could read it and immediately understand exactly what you’re doing. Compare:

Bad: “Supporting children’s education in Canada”

Good: “Providing academic scholarships and mentorship programs to students from low-income families in Atlantic Canada pursuing post-secondary education in STEM fields, with emphasis on first-generation university students”

Yes, the second one is wordier. It’s also approvable. (See: CRA Guidance CG-019 for more on drafting purposes).

4. Plan for the Long Haul

Most foundations are created to promote sustained giving over time. Your application should demonstrate that you’ve thought about:

How the foundation will be funded initially and ongoing

Investment strategy to meet the disbursement quota while maintaining capital

Governance structure that can outlive the founders

Succession planning for board members

How the foundation will evolve over decades

5. Get Your Governance House in Order

Before you submit your application, you should have draft documents for:

Bylaws or trust deed

Conflict of interest policy

Investment policy

Grantmaking guidelines

Board member roles and responsibilities

Compensation policy (most board members serve as volunteers, and in some provinces like Ontario, it’s prohibited to compensate them)

6. Understand the Money Math

Run the numbers before you commit:

Annual disbursement quota (3.5% of assets)

Administrative expenses (0.75%-1.5% of assets)

Investment management fees

Audit and legal fees

Other operational costs

If you’re starting with $500,000, your annual disbursement quota is $17,500. After expenses, you might have $10,000-$12,000 for actual grants. Is that enough to achieve your mission? If not, you need more initial capital or a plan to grow the endowment.

Private company shares (proceed with extreme caution)

Art and collectibles

One financial advisor recommends to commit at least $1 million, though this can be funded over several years. Start with what you can comfortably contribute now, and plan for future additions.

8. Study Successful Foundations

Before you apply, research foundations with similar missions. Look at their public filings (available through the CRA website). See how they articulate their purposes, structure their governance, and report their activities.

You don’t need to reinvent the wheel. Learn from those who’ve successfully navigated the process.

The Silver Lining

If your application was rejected, you’re not alone. Many successful foundations had to revise and resubmit their applications. The difference between them and the permanently rejected is that they listened to the feedback, addressed the concerns, and tried again with better preparation.

As one executive director of a second-generation foundation noted: “It’s money for the common good. I think there are a lot of philanthropists who are taking that responsibility seriously.”

The CRA isn’t trying to prevent you from doing good—they’re ensuring that entities claiming charitable status are legitimate, well-governed, and actually serving charitable purposes. Their job is to protect the integrity of the charitable sector and ensure that tax advantages aren’t abused.

Your Next Steps

So your application was rejected. Here’s what to do:

Read the rejection letter carefully. The CRA usually explains why they said no. Don’t dismiss their concerns as bureaucratic nonsense—address each one specifically.

Consult with professionals who specialize in charitable law and CRA applications. Share the rejection letter with them. Get their honest assessment.

Consider alternatives. Maybe a private foundation isn’t the right vehicle for your philanthropic goals right now. Donor-advised funds offer many similar benefits with less administrative burden and lower startup costs.

If you’re committed to the foundation route, revise your application thoroughly. Don’t just tweak a few sentences—fundamentally address the CRA’s concerns.

Take your time. The application can take 6+ months even when everything goes smoothly. Rushing the resubmission will likely result in another rejection.

The Bottom Line

Starting a private foundation in Canada is one of the most rewarding ways to give back to your community and create a lasting legacy. But it requires genuine commitment, substantial resources, proper planning, and professional guidance.

The CRA rejected your application not because they’re heartless bureaucrats who hate philanthropy (though I’m sure you called them worse things when you got that letter), but because your application didn’t meet the legal requirements for charitable status.

Learn from it. Fix it. Try again.

And next time, maybe start with that soul-searching before you fill out the paperwork. As one third-generation foundation trustee wisely noted: “If you’re going to have a lot of related family members involved, set conflict of interest guidelines. Have some policies or a healthy discussion that is recorded for posterity.”

In other words: do the hard thinking before you do the paperwork. Your future board meetings—and your relationship with the CRA—will thank you for it.

In this evolving economic landscape, collaboration with our firm offers clients a strategic advantage. With Cambodia’s reform-driven investment environment and Canada’s expanding footprint in Southeast Asia, our team of experienced consultants and legal advisors provides tailored guidance to help businesses navigate cross-border opportunities. We focus in developing comprehensive legal strategies, structuring international partnerships, and ensuring compliance in emerging markets.

By leveraging our regional insight and international expertise, you benefit from a trusted partner dedicated to helping you capitalize on growth potential in Cambodia and beyond.

Book a Consultation with Northfield & Associates

Your Trusted Partner in International Bilateral Relations

At Northfield & Associates are focus in Foreign Direct Investment (FDI), international trade missions, and cross-border legal strategy. Our team of experienced consultants and legal advisors offers tailored guidance and strategic insight to help you navigate the complexities of international partnerships and development opportunities.

Whether you choose to meet in person at one of our offices or connect virtually, we provide flexible and accessible consultation options. During your session, we’ll assess your goals, review key documentation, and guide you through every stage of your FDI or trade mission engagement.

Let us help you take the next step with confidence supported by trusted legal and strategic counsel every step of the way.

Take the First Step Today

If you believe you may be eligible for legal relief or simply need sound legal advice, we’re here to help. Contact us today to book your consultation. Let us provide the clarity, strategy, and peace of mind you need to move forward.

We serve our clients in English, Cambodian, Vietnamese, Mandarin and Cantonese, especially in Asian clients.

If you or anybody that you know, think that you meet the requirements and wish to receive further information.

We can help you start the application process and confirm eligibility requirements to participate.

We Offer Consultations & Meetings by Phone & Virtually. Affordable Fees.

Disclaimer:

The information contained in this article is provided for general information purposes only and does not constitute legal or other professional advice. Readers should seek tailored legal advice in relation to their personal circumstances.

Northfield & Associates International Corporation is a global consulting firm serving private enterprises, public institutions, not-for-profit organizations, and institutional capital providers. Operating across Cambodia, Canada, and global markets, the firm supports capital deployment, regulatory navigation, and enterprise decision-making in complex economic and geopolitical environments. Northfield & Associates delivers customized, execution-focused advisory solutions that drive measurable transformation, strengthen competitiveness, and enhance long-term highest value opportunities. The firm incorporates consulting, legal, regulatory, financial, and risk expertise to enable disciplined capital allocation, strong governance, and operational resilience. Northfield & Associates upholds a culture of applied insight and innovation, supporting clients across digital transformation, growth strategy, and organizational capability building. The firm advises individual, leading global corporations, midsize enterprises, government agencies, and mission-driven organizations through long-term partnerships. Enterprise-wide risk management, professional ethics, and fiduciary standards are embedded across all operations. Northfield & Associates’ diverse, globally unified teams are committed to execution certainty and sustainable, risk-adjusted returns aligned with ESG and stakeholder objectives.

Forward-Looking Information

This news release contains forward-looking information. All statements, other than statements of historic fact, that address activities, events or developments that the Company believes, expects or anticipates will or may occur in the future constitute forward-looking information.

This forward-looking information reflects the current expectations or beliefs of the Company based on information currently available to the Company.

Forward-looking information is subject to a number of risks and uncertainties that may cause the actual results of the Company to differ materially from those discussed in the forward-looking information, and even if such actual results are realized or substantially realized, there can be no assurance that they will have the expected consequences to, or effects on the Company. Factors that could cause actual results or events to differ materially from current expectations include, among other things: the failure to finalize negotiations concerning the increase of the Loan or to close such transaction and the failure of the Company to complete the acquisition of the Company Facility; operating performance of facilities; environmental and safety risks; delays in obtaining or failure to obtain necessary permits and approvals from government authorities; unavailability of plant, equipment or labour; inability to retain key management and personnel; changes to regulations or policies affecting the Company’s activities; and the other risks disclosed under the heading “Risk Factors” and elsewhere in the Company’s amended annual information.

Forward-looking information speaks only as of the date on which it is made and, except as may be required by applicable securities laws, the Company disclaims any intent or obligation to update any forward-looking information, whether as a result of new information, future events or results or otherwise. Although the Company believes that the assumptions inherent in the forward-looking information are reasonable, forward-looking information is not a guarantee of future performance and accordingly undue reliance should not be put on such information due to the inherent uncertainty therein.

Questions?

info@northfied.biz

Within Corporate Newsroom

Media Contact:

media@northfied.biz

Press contact

PR consultants press@northfied.biz

NOT LEGAL ADVICE. Information made available on this website in any form is for information purposes only. It is not, and should not be taken as, legal advice. You should not rely on, or take or fail to take any action based upon this information. Never disregard professional legal advice or delay in seeking legal advice because of something you have read on this website. Northfield & Associates professionals will be pleased to discuss resolutions to specific legal concerns you may have.

How Can Churches, Temples and Mosques Improve Volunteer Engagement?

Volunteers play a vital role in driving the mission of a church, temple and mosques forward. They support outreach, evangelism, and various faith programs, ensuring that the church, temple and mosques or mosque can continue its good work in the community. However, to maximize their impact, church, temple and mosques volunteers need proper training. Here are five training tips to empower your church, temple and mosques volunteers and help them serve more effectively.

1. Connect Volunteers with Your Church’s Mission

To start, it’s essential for volunteers to understand and connect with your church’s, temple’s and mosque’s mission. This connection will deepen their commitment and help them see how their efforts contribute to the church’s, temple’s and mosque’s goals.

How to Connect Volunteers with Your Mission:

Group Bible Studies: Choose a Bible or other religions scripts study that reflects your church’s, temple’s and mosque’s mission. Discuss how volunteer roles help achieve this mission.

Testimonies: Invite church, temple and mosques leaders or members to share stories about how the church, temple and mosques has impacted their lives, highlighting the role of volunteers.

Church History Overview: Share the story of your church’s, temple’s and mosque’s beginnings, its initial purpose, and how it has evolved. This gives volunteers a sense of belonging and purpose.

Personal Stories: Encourage volunteers to share their own stories and motivations. This mutual sharing fosters a supportive community and a deeper connection to the church’s, temple’s and mosque’s mission.

2. Create Comprehensive Training Materials

Once volunteers understand the mission, provide detailed training on their specific roles. A well-structured training program will prepare them to handle their responsibilities kconfidently.

Key Components of Training Materials:

Role-Playing Activities: Simulate common scenarios volunteers might face. This helps them practice and improve their responses in a supportive environment.

Interactive Quizzes: Use quizzes to test volunteers’ knowledge about their roles and church, temple and mosques procedures. Reviewing answers as a group ensures everyone is on the same page.

Q&A Sessions: Allow volunteers to ask questions and receive answers from leaders. This clarifies doubts and promotes a culture of open communication.

Detailed Guides: Provide written guides covering essential information, like the church, temple and mosques status and other logistical details. Volunteers can refer to these guides even after training ends.

3. Offer Ongoing Learning Opportunities

Learning shouldn’t stop after the initial training. Continuous learning keeps volunteers engaged and helps them grow in their roles.

Ways to Provide Ongoing Learning:

Books and Studies: Offer resources that emphasize the importance of volunteer service and its spiritual rewards.

Mentorship: Pair new volunteers with experienced ones for one-on-one guidance. This fosters a strong, supportive volunteer community.

Workshops and Training Sessions: Host regular workshops to help volunteers develop specific skills. Frequent sessions ensure that training is accessible when needed.

Easy Access to Support: Invest in volunteer management software or appoint a group leader to facilitate communication and address questions promptly.

4. Encourage Volunteer Growth

As your church, temple and mosques grows, so should the opportunities for your volunteers. Supporting their growth ensures they stay motivated and can take on new challenges.

Strategies to Encourage Growth:

Shadowing Opportunities: Let volunteers shadow church, temple and mosques leaders to learn about different roles firsthand.

Rotational Assignments: Rotate volunteers through different areas of ministry to broaden their experience.

Increased Responsibility: Allow volunteers to take on leadership roles within the volunteer program. This prepares them for larger responsibilities in the future.

Clear Growth Pathways: Clearly outline the steps for volunteers to advance to leadership positions. This transparency helps them understand how they can grow within the church.

5. Show Volunteer Appreciation